On Sunday night, our old friend exclaimed to my wife and me: “How have you all been??”

It’d been, well, almost a year since we’d been to her bar. We had plenty to catch up on with our drink-slinging pal as we sipped and snacked. Back on the home front, our babysitter had recently resurfaced and appeared to have bedtime under control. It was nice to have a throwback evening, the type we all took for granted just 12 months ago.

In the interim, many income investors have, likewise, taken low long-term rates for granted. Not we contrarians, of course. We’ve been discussing the prospect of Fed-Fueled Dividends and rising interest rates since October.

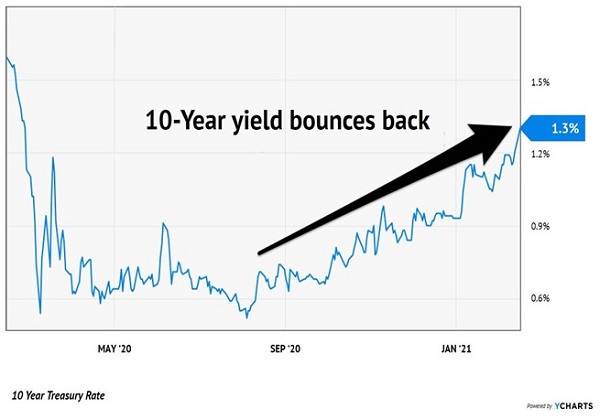

Suddenly, the mainstream media is on to our story because the 10-year Treasury rate has quickly rallied above 1.3%. One year ago, we’d have yawned at a yield like this. These days, however, it’s a shock to the system akin to leaving the house for the first time in forever:

10-Year Yield on a Comeback Tour

In the near-term, a pullback towards 1.1% or so is possible. Markets never move in straight lines, yet suddenly everyone seems to believe that rising rates are a sure thing. Their confidence may mark a minor turning point.

But there’s no denying that the trend in the 10-year yield is now up. Let’s look beyond the weeks ahead to picture the 10-year bond paying somewhere between 1.5% and 2%. (This might be what it yielded the last time you dined out at your favorite establishment!)

While a modest move by historical measures, it will be enough to generate a few winners and losers in Dividend-land.

Loser: US Treasuries

As yields rise, the demand for already-issued US Treasuries declines. These bond prices fall with rates. When rates are rising, we don’t want to own US bonds. (Which is not a big adjustment for us, we don’t buy them anyway.)

Neutral: Fixed-rate bonds (that pay a lot)

As rates rise, we’ll see lazy blanket statements that lump all bonds together. We should ignore “advice” that states that all bonds will fall as rates rise.

The bond funds in our Contrarian Income Report portfolio, for example, dish tax-advantaged dividends of 6%, 7% and more. A 2%-paying Treasury is not a viable competitor to yields like these.

If we were to see action that indicated much higher long-term yields were likely, we would consider moving more of our bond money into floating-rate bonds. It’s too early to make this call right now.

Loser: Utilities

Generally speaking, utility stocks remain under pressure when rates rise. The Utilities Select Sector SPDR ETF (XLU), for example, pays just 3.3%—not enough to differentiate it from rising bond yields. XLU is already down 10% from its November highs.

Exceptions? Of course! Utilities that are growing their dividends at a meaningful clip are always more interesting than the lot. Which reminds me…

Winner: Dividend growers

If there’s anything better than a secure dividend, it’s a rising payout.

Stocks with strong dividend growth tend to win in most environments. A higher-rate backdrop is no different. Rates are rallying because there is light at the end of the lockdown tunnel. A hot economy will be a boon to dividend growers, many of which have already raised payouts through the worst year in memory.

Winner: Bank stocks

Fed Chair Jay Powell has flat out said he wants inflation at 2% per year. As he works towards this “goal,” he should have company in the form of higher bond yields. After all, who would buy a 10-year bond that pays 1.3% when inflation is running at 2%?

Powell can set the short-term rate, which he has basically anchored to zero. On the other end of the curve, Powell does not control long-term rates. He may say he can influence them by buying Treasury bonds, and to an extent he can, but the bond market is bigger than even his printing press. Over time, Uncle Sam issues more debt than he is able to buy.

With the “spread” between the long and short end of the interest rate curve ballooning from nothing to something, bank profits will benefit. In relative terms, it will be a huge windfall because their borrowing costs will stay low while their lending profits pop.

I look past Wall Street’s big banks while searching for bargains. The small banks that service Main Street are the best pure plays on an improving economy and higher “long” rates.

Plus, they actually know their customers, which lowers their loan risk. Our CIR subscribers have been treated to 140% and 20% total returns (including dividends) from Synovus (SNV) and Comerica (CMA) respectively. Meanwhile you Hidden Yielders have enjoyed a 24% pop from Popular Bank (BPOP).

If the 10-year takes the break I’m anticipating, these shares should follow suit. So, there’s no pressure to chase them right now. However, we should look at any consolidation as a buying opportunity for bank dividend bargains.

Winner: Select business development companies (BDCs)

Business development companies (BDCs) also tend to thrive as rates rise. BDCs extend loans to small businesses and often their loans have a “floating rate” component included. So, the BDC tends to make more money as long-term rates rise.

For example, Hercules Capital (HTGC) has previously funded social media darlings like Facebook and Pinterest. Management regularly exceeds profit expectations and regularly raises the firm’s dividend.

Hercules’ Herculean (sorry, couldn’t resist) payout took a breather in 2020 but is back on the upswing. Shares yield a sweet 8.3% today and the stock has some upside, too, thanks to its rising payout:

Hercules! Hercules!

New Mountain Finance Corporation (NMFC) meanwhile yields a generous 9.8%. The company tends to lend $10 million to $50 million per pop, and most of its loans are floating rate.

Its portfolio companies (the firms NMFC lends to) are required to have barriers to competitive entry, recurring revenues and strong free cash flow. These businesses provide strong profits to help fund NFMC’s big payout.

The stock trades for a fraction below the value of its portfolio today, at 99.7% of book price. Which means NMFC is a potential BDC “free lunch” waiting for us here on the sidelines.

While I’m intrigued by HTGC and NMFC, my #1 income play for 2021 looks even better at the moment. This “All-Weather” dividend star should thrive in the months ahead. Click here and I’ll explain more about this unusual investment.

Recent Comments