Stocks or bonds? Why choose when:

- Stocks pay just 1.5%

- Bonds pay just 1.3%, yet

- There are little-known hybrid instruments yielding up to 7.9%!

These vehicles aren’t risky. They just happen to be favorites of Wall Street insiders who don’t want income investors like us crowding their favorite trades.

Unfortunately for them, we are not going to apologize for this article in advance. It’s time for us to discuss how to take the 1.5% yield from the S&P 500, the 1.3% yield from 10-year Treasuries—throw each in the trash—and instead type in the “convertible bond” tickers we’re not supposed to know about.

The Safety of a Bond, the Upside of a Stock (and 5X the Dividends of Both!)

Convertible bonds, like the preferred shares we discussed recently, pay regular interest, just like any other bond—and when bought the right way, their income streams are five times greater than anything you’d get from garden-variety stocks or bonds!

And convertibles have a trick up their sleeve: like stock options, they can be “converted” from a bond to a share of stock by the holder.

In other words, you’re getting the best of both bonds and stocks because you get steady dividend income, a downside hedge (because your principal is returned at maturity) and a shot at price upside, too.

No wonder the yacht-club set loves these investments so much!

Convertibles Still Off the Radar (For Now)

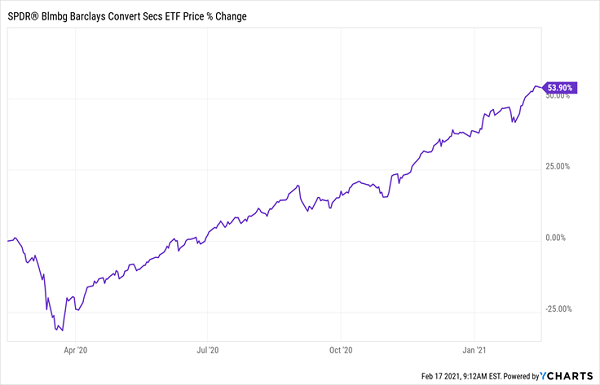

If you’re one of the very few folks who follow the convertible-bond market, you might wonder why I’m bullish on these investments right now. After all, convertibles have been on a tear, with the benchmark SPDR Bloomberg Barclays Convertible Securities ETF (CWB) up more than 50% in the past year:

Convertibles Have Soared—But We Can “Rewind the Clock”

Even so, the convertible-bond market is tiny, at around $300 billion in all. Compare that to the roughly $5 trillion tied up in ETFs and $36 trillion in S&P 500 stocks. So it’s got lots of room to grow, especially given that convertibles, with their downside protection, are nicely suited to the overbought market we’re facing today.

Now let’s address the other elephant in the room: the fact that convertibles only yield about 2% on average when you buy them “direct.” Heck, some issuers are even issuing 0%-yielding convertibles, like Peloton (PTON), whose newest issue lets you convert the bond to a stock at $239.25 a share—or $100 above the current price.

Converting a 2% (or 0%!) Yield Into an 8% Monthly Cash Stream

You and I don’t need to worry about either low- or (no-) yielding convertibles because we’ve got a “backdoor” way to squeeze them for much larger payouts—and buy them for less than folks who buy convertibles individually or through an ETF.

The secret is to buy through a closed-end fund (CEF). When we do, we give ourselves three critical advantages:

- Big discounts: Many CEFs—including the vast majority of convertible-bond CEFs—trade at discounts to net asset value (NAV, or the value of the convertibles they own). This is basically free money! And it lets us buy into the hot convertible-bond market at a nice discount—or to rewind the clock on some of their big, recent gains, in other words.

- Big monthly dividends: Yields of 7% and up are common among convertible-bond CEFs, including two we’ll look at below. And almost all pay dividends monthly.

- No legwork: We’ll save ourselves the worry about trying to figure out which issues to buy (and when to convert) by hiring a professional to do it for us. Better still, these convertible cowboys (and girls) will work for us for free (more on how their fees are “comped” for us in a moment).

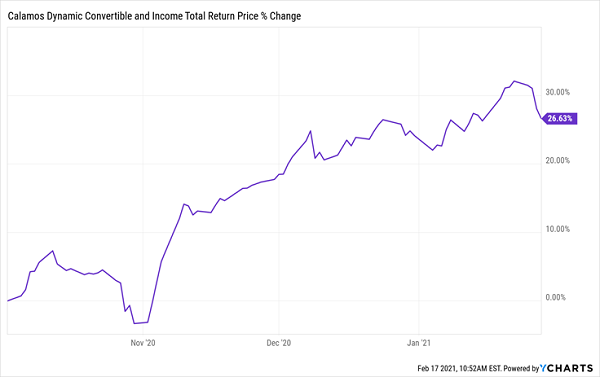

To see the kind of return that’s possible here, consider a CEF called the Calamos Dynamic Convertible and Income Fund (CCD). I recommended CCD in my Dividend Swing Trader service in October 2020, when it yielded a gaudy 8% and traded at a 9% discount to NAV.

Just over three months later, we checked out for a fast 27% total return, with a lot less volatility than you’d get buying regular stocks:

Convertible-Bond CEF Gives Us a Quick, Low-Drama Gain

And remember when I said we could get CEF managers to work for us for free? That’s another hidden bonus of buying at a discount: CCD’s fees (including interest on the fund’s leverage) are 2.5% of assets.

But since that was much less than the fund’s 9% discount when we bought, we were essentially getting those fees “comped.” No other fund, not even a so-called “low-fee” ETF, can offer up a deal like that!

CCD trades around par right now, so it’s not yet time to jump back into this one; let’s keep it on our watch list until we get another crack at a 7% (or more) discount, which has been around its average level over the last 12 months.

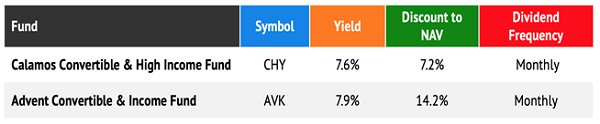

However, there are two other convertible-bond CEFs trading at decent discounts today, while boasting steady monthly payouts:

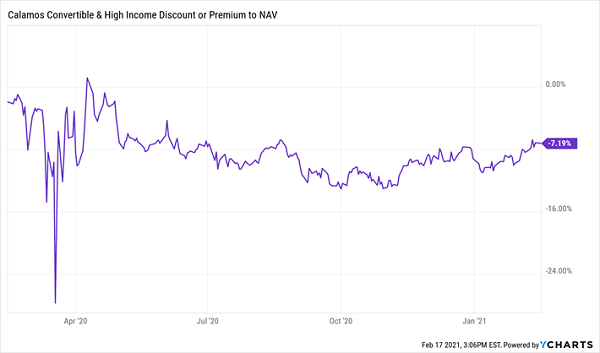

The Calamos Convertible and High Income Fund (CHY) trades at a 7.2% discount, and while that’s not as cheap as it was last summer, it’s still well below the 1.9% discount at which the fund traded pre-pandemic:

CHY: Still a Good Deal for a 7.6% Dividend

CHY holds 80% of its portfolio in convertibles, with the rest spread across corporate bonds, stocks, cash and bank loans. It’s also nicely spread across industries, with its biggest allotment (24.7%) in tech.

Calamos founder John P. Calamos Sr. has been in the convertible game for more than 40 years, having founded the company specifically to dive into the convertible market back in 1977. You’re getting his services for a reasonable 1.26% of assets—and remember that you’re not even paying that, thanks to CHY’s 7% discount!

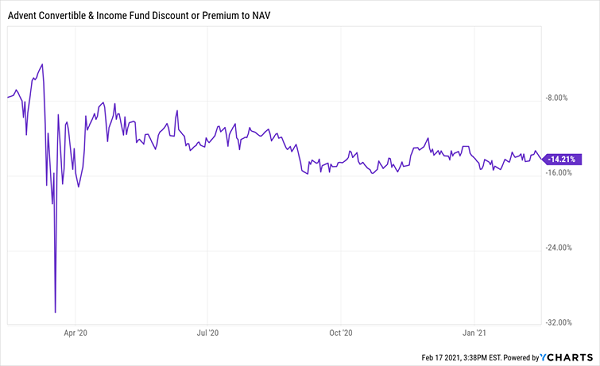

Finally, you can grab the Advent Convertible & Income Fund (AVK) at an even higher dividend and a bigger discount, to boot. With shares trading at 14.2% below NAV, this fund is far cheaper than it was pre-pandemic:

AVK: Now Selling for 86 Cents on the Dollar

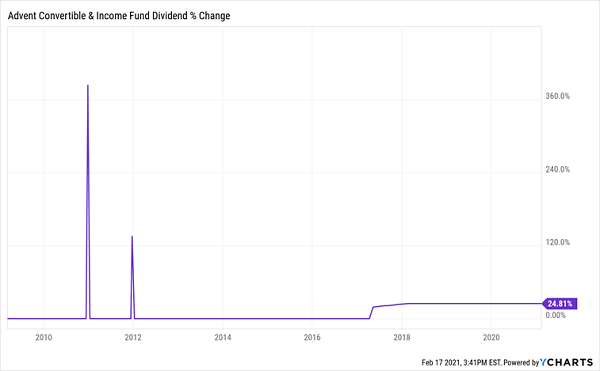

AVK also boasts a rock-solid payout, with the dividend holding steady coming out of the last financial crisis, then rising in 2017 and holding the line right through the current mess. There have even been a couple big one-time payouts thrown in for good measure!

High Yields and Payout Growth in 1 Fund

Thanks to AVK’s wide discount, we’re nicely positioned for some downside protection (and even some nice price upside) while we enjoy the fund’s rich 8% dividend.

You Can Retire on $500K. Here’s the Secret.

Don’t buy the conventional “wisdom” that you need a million bucks to retire well. You can do it on a lot less—like $500,000 less!

The 2 convertible-bond funds I just showed you give you a hint of how this works. With AVK’s 7.9% yield, you’d generate a nice $39,500 a year in dividends on a $500K investment today. That’s enough for many folks to retire on dividends alone, without selling a single stock from their portfolios.

But it’s just the start. Truth is, there are dozens of safe 8%+ yielders out there—and many of these cash machines even pay dividends monthly!

You’ll find my favorites among these “country club” buys in my new “8% Monthly Dividend Portfolio.” As the name says, it features a portfolio of stocks, CEFs, REITs and bonds that, taken together, will pay you a steady $40,000 a year on a $500K nest egg—year in and year out. And you’ll get your payouts every single month like clockwork.

I’m ready to take you on a full tour of this breakthrough portfolio now. Go here and discover it for yourself—including the names, tickers, buy-under prices and everything else you need to know about every stock and fund inside.

Recent Comments