“Daddy. Can you come play with me in the playroom?” my four-year-old asked.

“Sure. I’ll be right in,” I said. “Once I get done unloading the dishwasher. Would you like to help me unload?”

“No thanks,” my daughter replied. No surprise, but one day I hope to catch her off-guard.

She walked to the playroom. Barely. And reappeared.

“Daddy. You’re taking for ages.”

For ages is the equivalent of forever in our house. I think. Then again, given her level of exasperation, she could be telling me I’m taking longer than forever.

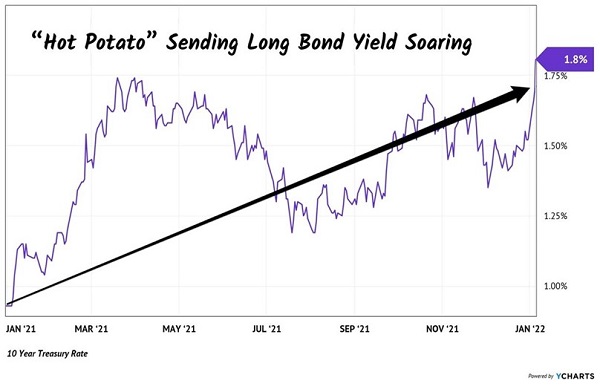

She’d make a good bond trader. With long rates rising every day, few income investors want to hold any bonds for any amount of time.

The 10-Year Rate is Spiking

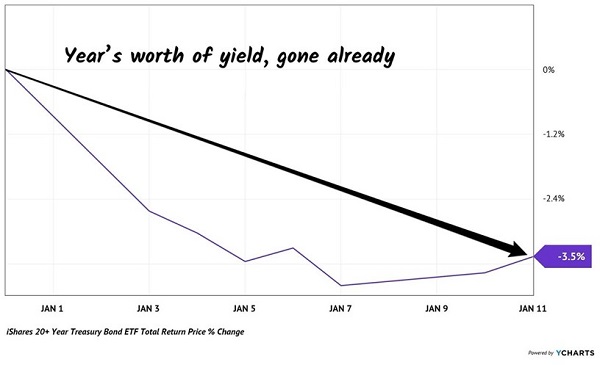

This is bruising long-dated bond funds like the iShares 20+ Year Treasury Bond ETF (TLT). TLT is the knee-jerk investment that many “first-level” investors buy when they are looking for bond exposure. Unfortunately, there are two big problems with TLT:

- It only yields 1.9%.

- And, worse yet, its 19-year duration is drubbing its total returns.

Any kid knows that 19 years is “way too long” to hold a bond when inflation is running a hot 7%. Please, somebody get these TLT investors a Contrarian Income Report subscription! They’re buying this fund for its (lame) yield and are losing that, plus more, in price declines:

By the Time 2022 Trading Opened, TLT Had Lost Its 2022 Dividend

Is there any hope for TLT? Not really. It’s a doomed strategy, picking up modest yield pennies on the inflation train tracks.

And we shouldn’t expect a pivot, because TLT is a “dumb” ETF that is run by machines. I’d rather have my four-year-old at the helm. She knows enough to not sign up for 19 years. (Or 19 minutes, for that matter. An inflation investing savant.)

Some grown-ups are good at managing fixed income. Rather than rely on computers, I prefer firms that have the inside track on the best bond deals. My favorite company, DoubleLine, has some excellent closed-end funds (CEFs) that are led by “bond god” Jeffrey Gundlach.

Among the many reasons to invest with Gundlach is that he and his all-star team of fixed-income analysts buy bonds that you and I can’t, such as those paying up to 8.9%. issued by government-backed agencies like Freddie Mac. It’s worth paying a management fee for “insider” access to these deals.

If these ideas sound esoteric, well, they are, and that’s where the value is in Bondland. Without venturing around the globe, we’re stuck with TLT paying a mere 1.9% (and losing that in price on the first trading day of the year).

This is why we take the elevator to floor two and pay Gundlach and Co. the “big bucks” management fee. “Big bucks” is tongue-in-cheek because when we buy one of DoubleLine’s closed-end funds (CEFs) at a discount, we essentially get our fees “comped.”

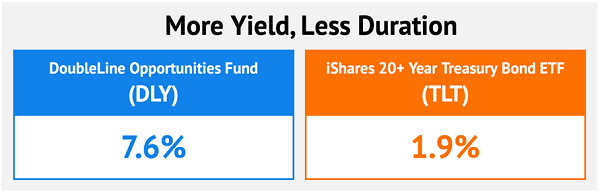

Fees come from NAV (net asset value, or the bonds the CEF holds minus any debt used to buy them), and we’re paying 4% less than NAV today for first-class CEF DoubleLine Opportunities Fund (DLY). In other words, we’re buying a dollar for 96 cents, giving us Gundlach’s fee for free. The discount is 4% and his fee is 2.2%. Our fee is taken care of.

DLY was created to take advantage of income opportunities in mortgage-backed securities (MBSs), commercial MBSs and collateralized loan obligations (CLOs). I realize these acronyms can frighten anyone who lived through the financial crisis (or watched The Big Short), which is why we look to DoubleLine to navigate these waters. They are proven masters of this universe.

The fund’s stormy start during the early days of the virus helped the team lock in higher credit quality than would otherwise be available with 7.6% yields. The “bond god” himself is our guy who got the call from Freddie Mac. We’ll gladly buy his connections—and income streams. It’s no wonder the DoubleLine CEFs pay so much more than Uncle Sam.

DLY is more prepared for higher rates, too. The fund’s bond holdings have an average duration (time until they mature) of just over two years. This is impressively low and provides the fund with flexibility if interest rates were to rise more than we are currently expecting. (It won’t get caught holding unfavorable bonds for years and lose both yield and price; it can move its money around to take advantage of rate changes.)

When buying bonds in 2022, don’t tie up your money for ages. Stay nimble on duration, and only invest with the best.

Another benefit of buying the best bond funds is that they tend to pay monthly dividends. If we’re smart about our selection, we can put together a portfolio of secure funds that pay monthly, adding up to 7% or more in yield per year.

But given our level of sky-high inflation, and the rate at which rates are rising, we can’t just close our eyes and buy just any bond fund. There are more dividend dogs like TLT that have too long a duration and simply don’t pay enough.

Instead, we want to focus on Monthly Dividend Superstars. These are secure funds with yields up to 8.1% that have double-digit price upside, too. In other words, we get paid every month while our nest egg grows. Talk about the perfect retirement investment!

My favorite funds are cheap thanks to recent market volatility. But I don’t expect them to remain in the bargain bin for long. Please click here so that I can send you my Monthly Dividend Superstars research, including the names and tickers of my favorite fixed-income investments.

Recent Comments