Most investors with $500,000 in their portfolios think they don’t have enough money to retire on.

They do – they just need to do two things with their “buy and hope” portfolios to turn them into $3,279 monthly income streams (or much more):

- Sell everything – including the 2%, 3% and even 4% payers that simply don’t yield enough to matter. And,

- Buy my 8 favorite monthly dividend payers.

The result? $3,279.69 in monthly income every month (from an average 7.6% annual yield, paid every 30 days). With upside on your initial $500,000 to boot!

And this strategy isn’t capped at $500,000. If you’ve saved a million (or even two), you can just buy more of my elite eight monthly payers and boost your passive income to $6,349 or even $12,698 per month.

Though if you’re a billionaire, sorry, you are out of luck. These Goldilocks payers won’t be able to absorb all of your cash. With total market caps around $1 billion or $2 billion, these vehicles are too small for institutional money.

Which is perfect for humble contrarians like you and me. This ceiling has created inefficiencies that we can take advantage of. After all, in a completely efficient market, we’d have to make a choice between dividends and upside. Here, though, we get both.

Heck, This Grandma Makes $387,000 Last Forever

Recently I was chatting with a reader of mine who manages money for a select group of clients. He’s using my No Withdrawal Portfolio to make a client’s modest savings – a nice grandmother with $387,000 – last longer than she ever dreamed:

“She brought me $387,000,” he said. “And wants to take out $3,000 per month for ten years.”

“Well she’s already withdrawn money for eight months (at $3,000 per month) and her balance has actually grown to $397,000. If the portfolio continues yielding 7% per year plus 2% per year in capital gains, and she withdraws $3,000 per month, it will pay my fees and still last her 27 years!”

Now many retirement experts pitch real estate as the best way to bank monthly income. But this grandma isn’t hustling to collect rent checks, or fix broken light bulbs. She’s simply collecting her “dividend pension” every month, which is 100% funded by her stocks and funds.

Actually her monthly salary is more than 100% financed – which is why her portfolio has grown by $10,000 as she’s withdrawn $3,000 per month.

How is This Possible? With “B-List” Monthly Payers Like These

Apple Hospitality REIT (APLE)

Dividend Yield: 6.2%

I wonder how many investors researching Apple (AAPL) have accidentally come across this lesser-known real estate investment trust, only to quickly punch in the correct ticker and get back to reading about iPhones.

Anyone who had missed out on a gem.

Apple Hospitality REIT (APLE) owns 236 hotels across 33 states for a capacity of roughly 30,000 guestrooms. The REIT’s properties are spread between two upscale hotel families – Hilton (HLT) and Marriott (MAR) – which includes their namesake brands, as well as the likes of Fairfield Inn, Embassy Suites and SpringHill Suites.

APLE has delivered an impressive growth story over the years, ballooning its top line from less than $400 million in 2013 to more than $1 billion last year. However, while the company has been rapidly expanding, management is fiscally responsible and has given the dividend a wide safety net.

Through the first six months of 2017, the company posted 90 cents per share in modified funds from operations (MFFO) – a tweaked version of FFO, which itself is an important gauge of a REIT’s operational performance and dividend health – against six dividends of 10 cents each. That equates to a payout ratio of just 67%, meaning it would take a catastrophe to keep Apple Hospitality from ponying up what it owes shareholders.

You Won’t Have to Worry About Apple Hospitality’s (APLE) Payout

Global Net Lease (GNL)

Dividend Yield: 9.6%

Global Net Lease (GNL) would seem to be a prime monthly dividend payer for several reasons.

For one, GNL is a “triple-net lease” REIT. Unlike many REITs that take responsibility for things such as taxes, insurance and maintenance, triple-net leasers instead push all those expenses onto the tenants. The tradeoff here is that they don’t charge lessees as much, but what they do bring in should be much more predictable.

GNL also has a couple other plusses, such as international diversity – it owns commercial properties not just in the U.S., but also the U.K., Germany and a few other European countries. Moreover, it doles out nearly 10% in dividends at the moment. And better still, it’s growing; Q2’s revenues, for instance, soared by more than 14% year-over-year.

However, Global Net Lease is externally managed, which requires it to pay a great many fees for property management and other services – fees that cramp the company’s funds from operations to a dangerous extent. GNL paid out 97% of its adjusted funds from operations (AFFO) as dividends last year, and through six months of 2017, this REIT has actually paid out a little more than its total AFFO.

Worse, GNL investors have watched shares decline 5% year-to-date amid a broad up-market, eating up much of their gains from income.

Global Net Lease’s (GNL) Dividend Is Merely Subsidizing Your Losses

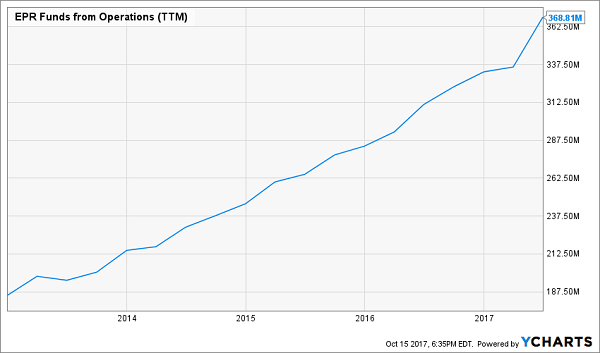

EPR Properties (EPR)

Dividend Yield: 5.8%

EPR Properties (EPR) is a play on one of my favorite themes of the past few years: the “experience economy.”

In short, people have started to put less value in merely amassing things, stuff and junk, and instead are increasingly spending their money doing things. That – along with the rise of Amazon.com (AMZN) and other e-commerce operators – have torn a hole through a number of retail REITs – but has benefitted a handful of properly positioned companies, including EPR.

Do you go to the movies? Ski? Have you ever spent a few hour in one of those state-of-the-art TopGolf driving ranges, complete with high-tech games and swanky bars? If so, chances are you’ve helped pad the pockets of EPR, which boasts 378 properties across the U.S.

That said, EPR is much more than entertainment – it also holds properties used for things such as public charter schools and early childhood education centers.

This extremely diversified REIT delivers a monthly payout that just got more than 6% sweeter earlier this year. Better still, the dividend is just 82% of AFFO, so EPR has plenty of ability to meet its obligation.

EPR Properties (EPR) IS Part of a New Generation of High-Performance REITs

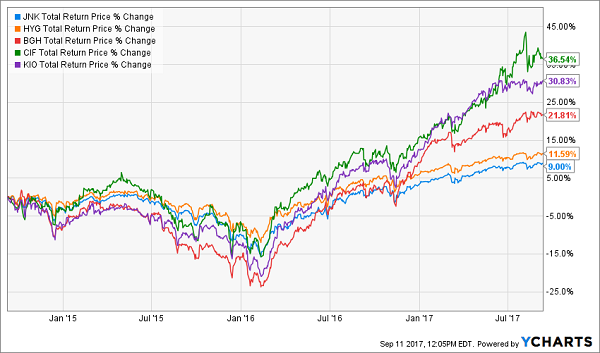

SPDR Barclays High Yield Bond ETF (JNK)

SEC Yield: 5.7%

It’s not widely practiced, but a few exchange-traded funds (ETFs) do dole out income monthly instead of quarterly. Better still, some of these monthly ETF payers even pay a fairly consistent amount of income every month.

The SPDR Barclays High Yield Bond ETF (JNK) does just enough to qualify, and in fact is a generally popular ETF. But I say stay away.

The JNK is a portfolio of nearly a thousand different junk issues – corporate bonds that are below investment grade, which means they have a higher risk of default, but also means that they have to yield more to compensate for that risk. Because SPDR’s junk ETF is so diversified (and so cheap), though, it has become a very common way for investors to gain exposure to this high-income bond class.

However, the JNK doesn’t hold a candle to a number of junk-focused closed-end funds (CEFs).

SPDR’s JNK Isn’t Junk, But It’s No Treasure, Either

These funds tend to charge more in expenses because of their active management, and they’re not nearly as talked about, but on average they offer much higher yields and have delivered much better performance than this merely “OK” exchange-traded fund.

Don’t buy into JNK’s junky payouts. Here are 8 better monthly dividend payers.

My Top Elite 8 Monthly Payers for 7.9% Dividends, Plus Upside

My all-star retirement portfolio contains 8 of the absolute best preferred stocks, REITs (real estate investment trusts) and CEFs (closed-end funds) out there. It’s well diversified across all types of investments and sectors, and the cash flows funding these dividends will do well no matter what happens in the broader economy or stock market.

Plus, relentless dividend growth means your 7.9% yield will be more like 10% in short order.

I’m ready to take you inside this “no-worry” retirement portfolio now. Click here and I’ll show you the 8 bargain investments inside it and give you their names, tickers, buy-under prices and much more.

Recent Comments