We talk a lot about discounts and dividends in our CEF Insider service. And they’re critical, of course. The need for a high dividend is obvious, especially if you’re in or near retirement. And buying a CEF at a big discount to net asset value (NAV) can slingshot us to serious price gains.

But being too focused on one number, be it the discount, the dividend or an individual stock’s P/E ratio, is what renowned contrarian Howard Marks calls “first-level thinking.” To get to the real truth of whether an investment is worth buying, we need to go deeper.

Of course, we contrarians know this. But even the savviest investors fall victim to first-level thinking from time to time, so we need to be vigilant.

And we need to be especially vigilant now, because making this mistake could lead you to hold off on buying stocks (and stock-focused CEFs). After all, the common wisdom tells us that stocks are too expensive now, so it’s safer to stay on the sidelines.

We’re going to debunk this simplistic (and deeply flawed) argument today. We’ll also talk CEFs—and our dividends—as we do.

Stocks Often Get Pricey—and Then Get Pricier Still

The focus of today’s first-level fears is the S&P 500’s P/E ratio of 30, which to many folks says stocks are ripe for a crash.

But this fear is unlikely to become reality. Bloomberg columnist and portfolio manager Nir Kaissar has a simple explanation of why this is so. In a recent column, Kaissar points to the following chart:

Stocks Have Been “Pricey” Since 1990!

Here, Kaissar is using Nobel-laureate Robert Shiller’s cyclically adjusted price-to-earnings (CAPE) ratio, but the same applies to the P/E ratio: while stock valuations are way above their historical average (going back to 1881), they’ve tended to stay above that average for long periods, including for most of the last 30 years!

Then there’s the Federal Reserve, which has said it will keep interest rates low for a long time; right now, many economists believe rates won’t rise until the start of 2023. That means over a year of strong stock performance is very likely.

Tech’s “Takeover” of the S&P 500 Also Escapes First-Level Thinkers

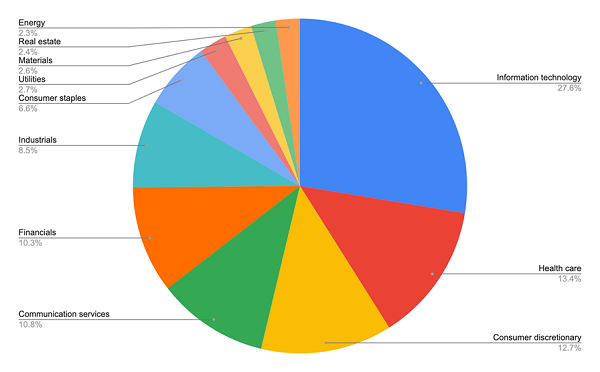

There’s a more long-term reason to think a higher market valuation is here to stay: technology. Currently, tech is over a quarter of the S&P 500, but it’s actually much more.

Tech’s a Bigger Slice of the Market Than Most People Think

Source: CEF Insider, S&P Indices

Look at the 11% of the market in communication services: that sector includes Alphabet (GOOG, GOOGL), Facebook (FB), Verizon Communications (VZ), EA Games (EA) and Activision (ATVI)—dyed-in-the-wool tech firms every one! Including communication services, more than a third of the S&P 500 is devoted to technology.

Plus, consumer discretionary’s biggest constituents are Amazon.com (AMZN) and Tesla (TSLA), with many other tech-heavy companies also part of that sector. And we’re not even talking about the health care, industrial and utility stocks with close ties to tech.

This matters because technology historically has had higher valuations, since it has a much higher growth rate than other corners of the market and thus attracts more investor cash. Thus, as tech becomes a bigger part of the S&P 500, the index will naturally have a higher average P/E ratio.

A “Goldilocks” Play That Fits Today’s Market

Still, I understand if you want to take a more defensive approach these days. And the good news is that CEFs give us a way to stay in the market while also hedging our downside.

That would be through a covered-call fund like the Nuveen S&P 500 BuyWrite Income Fund (BXMX).

BXMX is like an ETF in that, as the name suggests, it holds the stocks in the S&P 500: heavyweights like Apple (AAPL), Berkshire Hathaway (BRK.A) and JPMorgan Chase (JPM).

But that’s where the similarities end, because a key feature of BXMX is that it sells call options, or contracts that let an option buyer purchase the fund’s holdings in the future at a set price. These buyers pay the fund a cash premium for this right, and these payments naturally cut BXMX’s volatility (because it gets more of its portfolio returns in cash) and enhance our dividends: BXMX yields 5.9% now, quite a bit more than the market’s 1.3% average.

5 CEFs That Pay You 7.3% (With 20% Upside Ahead)

I’ve assembled a 5-CEF portfolio that pays you much more than BXMX—an outsized 7.3% average payout. And all 5 of these funds trade at much bigger discounts, too!

My prediction: 20% price gains from this 5-CEF “mini-portfolio” in the next 12 months as these ridiculous discounts swing back to normal.

And you still get a nice layer of protection here, both courtesy of these funds’ big discounts (which will hedge their downside in a correction) and the huge diversification this portfolio offers: these funds hold large-cap and midcap stocks, corporate bonds, real estate investment trusts and more.

Don’t miss this opportunity for income and gains. Click here and I’ll reveal full details on all 5 of these CEFs: names, tickers, best-buy prices and my full analysis of each one.

Recent Comments