Don’t get me wrong—I love my kids. It’s just that I’ve loved “hidden yields” longer.

What are these long-term affectionate affairs of mine? These under-the-radar dividends require looking at the bigger-picture view of all the cash a company is spending on you and me. Sometimes it means looking past a low current yield and instead focusing on rampant dividend growth that will mean big income down the road.

But sometimes, that simply means looking where everyone isn’t—like five little-known stocks yielding a cool 7% on average that we’ll discuss today.

The Virtue of Hidden Stocks

To understand the power of investing in the relatively unknown, consider this quick story from a good friend of mine:

Used-car prices have skyrocketed over the past few months. That’s because COVID-19 has disrupted a number of automotive supply chains, making new supply scarce. As a result, just about anyone looking to sell their used cars have been able to do so at prices they wouldn’t have dreamed of even a year ago.

However, my friend was trying to sell something unusual: A special-edition car, from a niche automaker, that was less than a year old.

A car like that is a challenge for used-car dealers. There’s oodles of data from the thousands of 2011 Honda Civics and 2014 Corollas that have been repurchased and resold over the past few years. But dealerships had seen few if any of this particular vehicle, so they had little to no data to go on.

And my friend, like a seasoned fund manager, exploited an inefficiency in the market to sell the car back for well more than he had bought it for.

You and I can do something similar in the stock market.

Certain industries fly well under Wall Street’s radar. You won’t see portfolio managers talking about them on CNBC. A handful of analysts might cover these investments, if any. Few institutional investors hold positions in these picks. And that’s the perfect recipe for finding underappreciated stocks and funds that we can leverage for high “hidden” yields.

And better yet? Many of these underloved, lightly covered stocks just so happen to pay regular monthly dividends.

You can read all about the benefits of monthly dividend stocks here, but in short: Monthly payers’ distribution schedules match up perfectly with your everyday bills; the payouts actually compound faster, providing better returns over time; and they often yield more than their quarterly paying counterparts.

In fact, these five obscure monthly dividend picks currently provide a full 7% in annual income—currently more than five times the broader market!

Phillips Edison (PECO)

Dividend Yield: 3.6%

Let’s start out with a stock that hasn’t even been around for a month.

Phillips Edison (PECO) is a real estate investment trust (REIT) owns and operates omni-channel grocery-anchored neighborhood shopping centers, and it has existed as a company for three decades. It was founded in 1991, and the next year, it acquired its first property: Nordan Shopping Center in Danville, Virginia. Fast-forward to today, and it sports a portfolio of 278 wholly-owned properties as well as 22 shopping center properties it owns through a pair of joint ventures.

However, the company has only traded on the public markets for a couple of weeks. It announced the closing of its initial public offering (IPO) on July 19, offering 17 million shares at $28 each. And a couple weeks later, PECO’s underwriters exercised their option to buy an additional 2.55 million shares of common stock.

The current dividend isn’t much older. Phillips Edison announced in November 2020 that it would resume its monthly distribution in January 2021. PECO currently pays 8.5 cents monthly (following a 3-for-1 split executed in early July, before its IPO), translating into a 3.6% yield. That’s well covered by operations; its first-quarter distributions were just 42.5% of core funds from operations (FFO, a vital REIT profitability metric).

Put Phillips Edison on your radar. It’s far too young of a public issue to gauge just yet, and most stocks go through a choppy first few months after their IPO. But solid dividend coverage suggests higher payouts over time. And while physical retail isn’t exactly an explosive industry to be in, grocery-anchored retail seems at far less risk than shopping malls and outlet centers.

Source Capital (SOR)

Dividend Yield: 6.4%

If you’re familiar with closed-end funds (CEFs), you’re probably familiar with names such as Nuveen, Western Asset and Aberdeen. But there are several interesting smaller shops out there, and FPA’s Source Capital (SOR) is among their ranks.

Source Capital has just one goal: maximum total returns. CEF management says it’s free to invest “across capital structure, geographies, sectors, and market caps,” and if the market isn’t offering up any compelling equity opportunities, it will happily plow its money into bonds.

As of the end of June, SOR was as diversely invested as you could want. Roughly 40% of the portfolio was U.S. equity, with another 13% in American fixed income. Another 6% of assets were allocated toward international debt. And the rest was plunked into international stocks from roughly a dozen countries including Switzerland, China and South Africa.

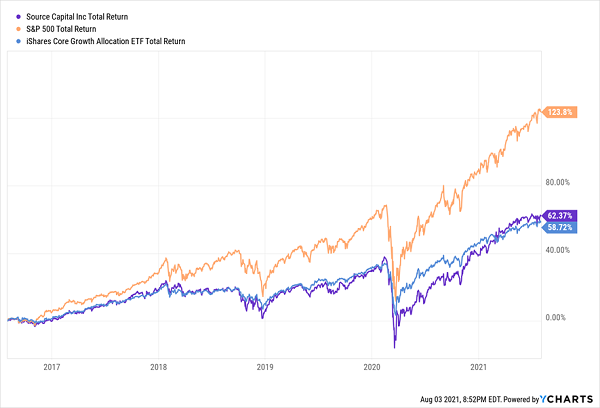

Unlike many other CEFs, Source Capital doesn’t use any leverage—it’s a traditionally operated fund. That makes the 6.4% yield look a little suspect, and indeed, much of that often comes in the form of long-term capital gains, which aren’t as tax-friendly.

Because Source Capital dips into debt, we shouldn’t expect it to mirror the S&P 500 … and it certainly doesn’t. What’s more worrisome is that its performance is virtually on par with the iShares Core Growth Allocation ETF (AOR)—a 60% stocks-40% bonds allocation fund that has twice the fixed-income exposure as SOR currently.

Source Is a Tepid Total Return Producer

Further putting SOR’s already lackluster returns in jeopardy is a big shift in the managers’ office. Thomas Atteberry, co-portfolio manager, is stepping down in July 2022.

Ellington Financial (EFC)

Dividend Yield: 9.9%

Ellington Financial (EFC) is a mortgage REIT (mREIT) that invests in a wide range of assets, including mortgage-backed securities (MBSs), mortgage loans, consumer loans, asset-backed securities, even equity investments in loan origination companies.

In general, mortgage REITs are far more opaque, and thus far more time-consuming and difficult for your average investor to really get to know. So typically, an investment in this space will come down to just a few points, including valuation and the manager’s track record.

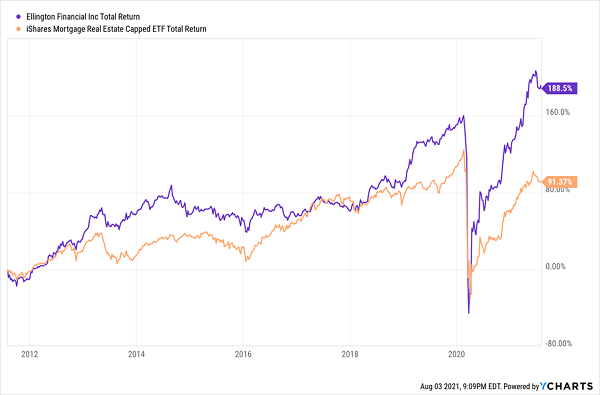

On the latter point, EFC is a long-term outperformer. And while its share price throughout the COVID-19 bear market might not indicate it, external manager Ellington Financial Management LLC has proven adept at navigating EFC in times of crisis.

Ellington: Twice as Nice as Its Peers

From a valuation perspective, EFC is ever so slightly overpriced, trading at $18.20 per share versus a book value of $18.23 as of the end of May. That also takes into account a recent dip in shares sparked by the company’s 6 million-share offering, which it executed while it traded at a premium to book value. It last pulled off such an offering in January 2020.

It’s a good situation, but it could be better. While the 10% yield is fantastic, growth estimates for next year are minimal, and at best, shares appear fairly valued.

Gladstone Commercial (GOOD)

Dividend Yield: 6.6%

Next up, let’s meet one of the members of the Gladstone family!

Gladstone Commercial (GOOD) is one of a group of public investment vehicles that also include Gladstone Investment Corporation (GAIN), Gladstone Capital Corporation (GLAD) and Gladstone Land Corporation (LAND). As a group, they invest in (and buy) lower middle market companies, and deal in commercial and farmland real estate.

Gladstone Commercial’s place in this world is investing in single-tenant and anchored multi-tenant net leased industrial and office properties. Its portfolio currently consists of 120 properties in 27 states, leased out to 107 different tenants spanning 19 industries. Telecommunications and conglomerate/diversified tenants each make up 15% of the portfolio, followed by healthcare at 10%. Automobile, building and banking earn single-digit exposure, and the rest of the portfolio is spread across 13 other industries.

This diversified tenant roster includes the likes of Morgan Stanley (MS), Automatic Data Processing (ADP) and Willis Towers Watson (WLTW). And no single tenant accounts for more than 3% of annualized straight-line rent.

But what I like about Gladstone is that it’s not a passive rent collector. Its management team will work with its tenants to make value-add capital improvements. That means repaving parking lots, undergoing building expansions, and even helping tenants reduce operating expenses.

This is a good company that has made savvy moves this year, including converting office space (an increasingly troubled asset post-COVID) into an industrial building. This adaptability has served GOOD well over the long haul, outperforming the broad-based Vanguard Real Estate ETF (VNQ).

Gladstone Gets It Done

But you’ll pay for excellence at present. GOOD shares currently trade at a rich premium.

Saba Capital Income & Opportunities Fund (BRW)

Dividend Yield: 8.6%

Like Phillips Edison, Saba Capital Income & Opportunities Fund (BRW) is new.

Well, sort of.

Saba Capital Income & Opportunities Fund has only been known by that name for a bit more than a month. Prior to June 22, it was the Voya Prime Rate Trust (PPR). So what happened?

A proxy battle.

Saba Capital Management LP is a hedge fund manager and activist investor that got Saba-nominated board members elected at Voya Prime Rate Trust last year. Those board members then picked Saba to replace Voya Investment Management Co. as the fund’s investment advisor effective June of this year.

The new BRW will primarily invest in high-yield credit, but it also says it “will also opportunistically target other investments, such as registered closed-end funds and special purpose acquisition companies.” Nothing so rash in the current portfolio, however. It currently is 100% invested in secured senior loans from 260 issuers including Nexstar Broadcasting, Caesars Resort Collection and Bausch Health (BHC). It has a little international exposure (less than 10%), but a wide range of industries, with none commanding more than 7.5% of assets.

New management also rolled out a shiny, brand-new monthly dividend starting in June, currently set for 3.3 cents per share, good for a massive 8.6% yield at current prices.

The “A” Squad: Monthly Payers Doling Out 7%-Plus Yields

Just like with PECO, put BRW on your watch list. It’s difficult to tell what to expect with a brand-new manager after just one month, but you love to see a fund get aggressive with a generous new dividend to be paid every 30 days.

But if you’re looking for juicy monthly dividends that are ready for primetime right here, right now, it’s time for you to discover the market’s best 7%-plus yielders.

My “7% Monthly Payer Portfolio” is an elite set of high-income, high-frequency dividend payers that, at current prices, are smack-dab in the middle of our ideal “buy zone.” And as the name suggests, these 7% dividends are paid out to investors each and every month.

Many of the picks in my “7% Monthly Payer Portfolio” leverage the power of steady-Eddie holdings to generate not just massive yields, but shockingly aggressive price performance. That allows us to do the unthinkable from an income strategy: double our money much more quickly than traditional blue-chips-and-mutual-funds portfolios.

These dividends aren’t just good.

They’re not just great, either.

They’re downright life-changing.

If you drop $500K—less than half what most financial gurus suggest you need to retire—into this powerful portfolio now, you’d kick-start a $35,000 annual income stream. That’s nearly $3,000 a month in regular income checks!

The time to get in is now, while you can still buy these names at bargain prices. Click here to get everything you need—names, tickers, complete dividend histories and more—instantly!

Recent Comments