The stock market is coming off another sugar high, but REITs (real estate investment trusts) are still cheap. That’s great news to us income investors, who look past the piddly paying blue chips on the S&P 500. We prefer REITs because they pay, and we appreciate a deal when we see one:

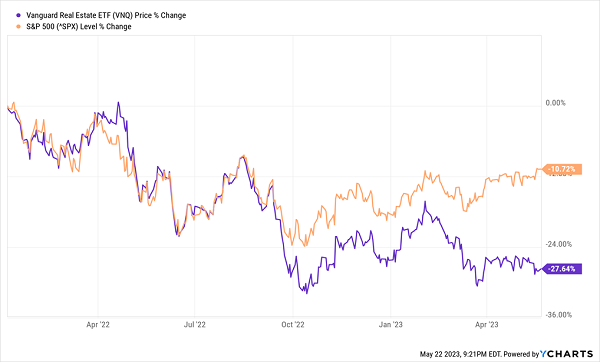

REITs Remain Near Their Bear-Market Lows

REITs are on the mat because the Federal Reserve has relentlessly hiked rates. Good. Those of us who want to retire on dividends alone love how wide REITs’ yield spread over basic stocks has become.

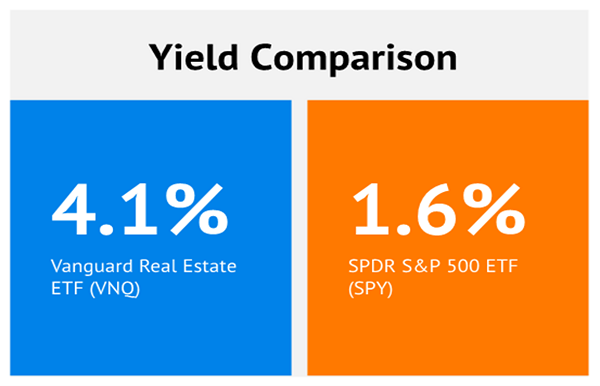

Even a vanilla fund like Vanguard Real Estate ETF (VNQ) is a better income source than “America’s ticker”—VNQ yields 4.1% while SPDR S&P 500 ETF only pays 1.6%.

These dividend deals are available because the main source of downward pressure on REITs has continued apace in 2023. The Federal Reserve recently hiking its benchmark rate another 25 basis points to 5%-5.25%.

Why Are REITs Sinking? Higher Rates

Higher interest rates mean not only higher costs of capital for REITs (and all other companies, for that matter), but also more competition for income as bond yields become increasingly competitive.

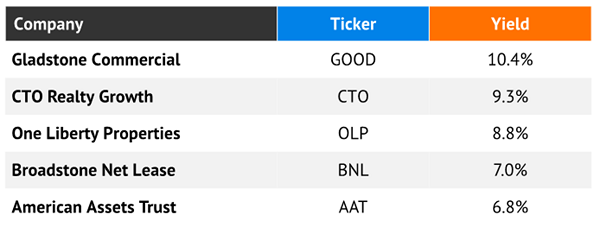

These elevated rates won’t last forever, though. We are, after all, careening towards the most anticipated recession of all time. When the slowdown officially hits, the Fed is going to cut—and REITs like the following five are going to get a close look from income investors. Let’s look at this 8.5%-paying potential portfolio ahead of the herd:

CTO Realty Growth (CTO, 9.3%) is a diversified REIT that owns 15 retail properties, three office properties, and five mixed-use properties totaling more than 3.7 million square feet. It also owns a nearly 15% stake in Alpine Income Property Trust (PINE), a net-lease REIT.

CTO has dipped by more than 20% over the past year, hurt in part by being forced to lower the rents on two large leases.

Still, CTO bears watching. It converted to the REIT structure just two years ago, but it has already raised its payout thrice since then. While dividend coverage is stretched—at about 90% of estimated 2023 core adjusted funds from operations (AFFO)—property demand is improving.

American Assets Trust (AAT, 6.8% yield) is another diversified REIT, this one boasting 23 properties spanning office, retail and residential. AAT has been battered, losing nearly half of its value over the past year or so—nice from a valuation perspective, but it might be too dangerous to touch. Occupancy across office, retail and multifamily was down year-over-year during the first quarter, with only mixed-use on the rise. Still, there was reason for hope in its Q1 report: FFO improved 16% year-over-year, while same-store NOI improved 6.5%.

One Liberty Properties (OLP, 8.8% yield) is a net-lease REIT that has been transforming itself over the past few years. Its 121 properties include restaurants, fitness centers, grocery-anchored real estate and office space, but it’s increasingly shifting toward industrial holdings. The good news? Industrial now makes up roughly 60% of its rental revenue. The bad news? Bed Bath & Beyond’s bankruptcy, as well as a possible restructuring of leases with Regal Cinemas, is hanging over OLP’s head. And while OLP has an excellent yield near 9%, the payout hasn’t grown in years.

Broadstone Net Lease (BNL, 7.0% yield) is another net-lease REIT, this one focusing on single-tenant commercial properties. Its portfolio includes 801 properties, the vast majority (794) spread across 44 states, with the rest in four Canadian provinces. Despite its nearly 30% losses over the past year, things don’t look dire for this REIT, which boasts 99.4% occupancy. BNL also has a long debt leash, with less than 2% of its debt coming due through the end of 2025.

Gladstone Commercial (GOOD, 10.4%) is part of the Gladstone family of REITs, this one focused on single-tenant and anchored multi-tenant net-leased industrial and office properties. As I wrote in March, Gladstone is being hampered by its 40% allocation to office properties—to the point where GOOD was forced to cut its dividend by 20% this year, to 10 cents per share.

“Capital preservation” is a smart move for the troubled REIT, and it brought its FFO payout ratio down from 96% before to 77% now. Still, roughly $100 million worth of interest-rate caps will expire in the middle of this year, which will raise interest expenses, and it faces the longer-term problem of what WFH means for its properties.

Your Guide to Retirement Riches: 8%-Yielding Blue Chips That Pay EVERY MONTH

Gladstone belongs in the “Dividend B Squad.” High yield? Yes. Recovery potential? Absolutely. But it’s just not the kind of durable, reliable income holding we need if we’re going to retire without losing sleep every night.

For that, we need the “A” squad: diversified, reliable payers of mouthwatering yet dependable income—preferably, those that don’t knuckle under every time the economy throws a fit.

And you can find these rare monthly dividend blue chips in my “8% Monthly Payer Portfolio.”

Many of the recommendations in my “8% Monthly Payer Portfolio” leverage the power of steady-Eddie holdings to generate massive yields, while also fostering the potential to generate aggressive price performance.

These dividends aren’t good. They’re not even great. They’re retirement-sustaining, all on their own.

A mere $500,000 nest egg—less than half of what most financial gurus insist you need to retire—put to work in this powerful portfolio could generate a $40,000 annual income stream.

That’s more than $3,300 every month in regular income checks!

Even better? The current bear market has provided us with a rare gift, pulling many of these monthly income plays back into our “buy zone,” where we can grab them at bargain prices. Click here to for more on my top monthly dividend payers for 8%+ dividends right now!

Recent Comments