Most dividend investors understandably love the idea of an 8% No Withdrawal Portfolio. It’s a simple yet “game changing” idea that you don’t hear much from mainstream pundits and advisors.

Find stocks that pay 7%, 8% or more and you can retire comfortably, living off dividend checks while your initial capital stays intact (or even appreciates).

Now this strategy is a bit more complicated than simply finding 8% yields and buying them. Granted the recent stock market pullback has benefited investors like us because we can snag more dividends for our dollar. Yields are higher overall, and that’s a good thing.

Next we must smartly select the stocks that are going to pay our dividends securely – without tapping their own shares prices to pay us.

Real estate investment trusts (REITs) are naturally suited for this purpose. They must, as per their status pay most of their profits to us as dividends. This tax requirement let’s us play landlord from the convenience of our brokerage accounts!

Plus we can cherry pick our real estate buys to focus on those that increase their dividends consistently over time. These stocks have wonderful “built in” capital appreciation potential because their stock prices rise as their dividends climb.

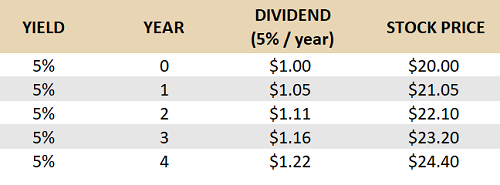

Let’s map out the case of a REIT dividend grower with some round numbers to make the math easy. We’ll say the stock is a 5% payer growing its dividend by 5% per year. Its current yield (left column) stays constant amidst the dividend growth because its stock price (right column) rises along with its dividend:

We won’t get this price growth from a mere ETF, however. While many REITs do raise their payouts year after year, there are other REITs that find themselves overleveraged and forced to slash their dividends. Which means we must select our REITs smartly and carefully.

I’ll share my favorite REIT buys (which are pullback-proof to boot!) in a moment. First, let me highlight three to avoid right now:

Washington Prime (WPG)

Dividend Yield: 18.1%

In fairness, retail REIT Washington Prime (WPG) started with a weak hand. Simon Property (SPG) packed many of its second- and third-tier mall assets into the company and spun it off in 2014. (At the time, Fitch Ratings even warned against the bargaining power of second-tier malls associated to spinoffs like Washington Prime’s.) WPG then bought up Glimcher Realty Trust for $4.3 billion in early 2015 to make up the current entity.

To its credit, Washington Prime has been repositioning itself in Tier 1 and Open Air malls, but the company still is dogged by the woes of dying “anchor” and other large retailers such as JCPenney (JCP), Sears and Toys R Us that spawn press-release headlines such as:

- “Washington Prime Group Provides Leasing Update and Progress on Toys R Us Repositioning Efforts”

- “Grand Central Mall to Begin Demolition of Former Sears Space”

- “Washington Prime Group Expects No JCPenney Closures” (This is what qualifies as good news nowadays!)

While the company has rebounded with the rest of the REIT market in 2019, it’s not because it’s doing much right operationally.

Full-year adjusted funds from operations (FFO, an important REIT profitability measure) dipped 7.4% in 2018. That’s bad. What’s worse is how Washington Prime closed out the year–with a 13.6% dip in AFFO, to 38 cents per share. One of the “sunnier” parts of the report was that comparable net operating income for its Tier 1 and Open Air assets were “practically flat, down only 0.3%” … after they backed out $7 million in impact from Toys R Us’ bankruptcy and some capex.

Considering these issues, as well as the warning signal flashing from its barely-not-junk debt rating, Washington Prime is not a reclamation story investors can feel good about yet–18% yield or not.

WPG: Growing Yield, Shrinking … Everything Else

Annaly Capital Management (NLY)

Dividend Yield: 11.7%

Mortgage REIT Annaly Capital Management (NLY) has had significant issues in the past because of its heavy concentration in fixed-rate securities. The problem? When rates rise, the rates on those securities look increasingly stale, and their prices decline as investors jump into higher-rate securities. Back in 2004-06, this hacked away at profits, causing Annaly to hack away at its dividend.

NLY remains heavily invested in fixed-rates, at 93% of the portfolio (that’s growing; it was 90% just a year ago). It’s not as much of a problem now that the Federal Reserve has pushed the “pause” button on interest rates, though it has hampered the company over the past few years.

But Annaly investors still have plenty to grumble about.

Fourth-quarter earnings were a doozy. The report was peppered with issues such as an uptick in leverage from 6.6-to-1 at the end of 2017 to 7.0-to-1 at the end of last year, thinner net interest margins (1.34%), a decline in book value per share (From $11.34 to $9.39). But the biggest problem was the most important number: core earnings per share, which declined 13.3% to 26 cents per share.

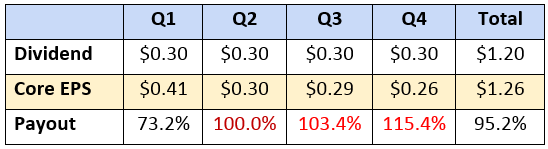

The direction (down) is problematic, obviously. But dividend coverage remains an issue, too. Namely, Annaly has paid out all if not more of its profits out as dividends in each of the past three quarters:

The yield is nice, but the cash flows behind it aren’t.

iShares Mortgage Real Estate ETF (REM)

Dividend Yield: 9.2%

Expenses: 0.48%

I love the instant diversification investors can reap from buying into funds. But I prefer actively managed closed-end funds (CEFs) over index funds in part because in some market industries, fund managers act like bouncers, keeping out the riff-raff and letting the few attractive players in.

A good example of how index funds get it wrong? The iShares Mortgage Real Estate ETF (REM)–a portfolio of about 35 mREITs that are weighted by market cap. In other words, the bigger they are, the more they affect the fund’s performance.

The problem? The two 800-pound gorillas of the mortgage REIT space – Annaly Capital and AGNC Investment (AGNC) – make up almost 30% of the portfolio and have dragged it down with their underperformance.

The mREIT industry is a difficult one with more losers than winners, making quality stock selection vital, moreso than with other areas of the market. You see the same thing in international real estate, where ETFs such as the SPDR Dow Jones Global Real Estate ETF (RWO, 3.5% yield) and SPDR Dow Jones International Real Estate ETF (RWX, 4.9%), where you would be far better cherry-picking the best REITs to buy at any given moment.

How to Buy REITs for 109% Returns

It’s actually easier to “time” REIT stocks than most investors think. Thanks to their generous yields we can simply buy the safest payouts when we are able to secure the most dividends for our dollar.

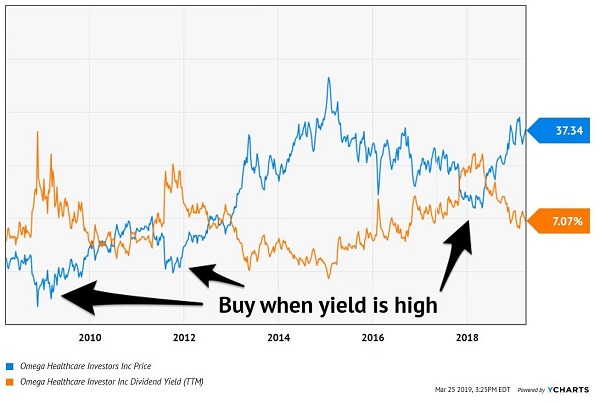

Let’s take healthcare landlord Omega Healthcare Industries (OHI). The firm’s payout is usually generous, and always reliable—yet, for whatever reason, its sometimes-manic price action gives investors heartburn.

But it shouldn’t. It’s actually quite predictable. Check out the chart below, and you’ll notice:

- When the stock’s yield is high (orange line), its price is low. Investors should buy here.

- When the stock’s price is high (blue line), its yield is low. Investors should hold here, and enjoy their dividend payments.

Investing is Easy: Buy When Yield (Orange Line) is High

Today OHI’s yield is neither opportunistically high nor offensively low. It’s a respectable “hold” in a high yield portfolio. If yield curve or tariff or recession fears drive the price lower, I would recommend buying more shares at their higher yield without hesitation.

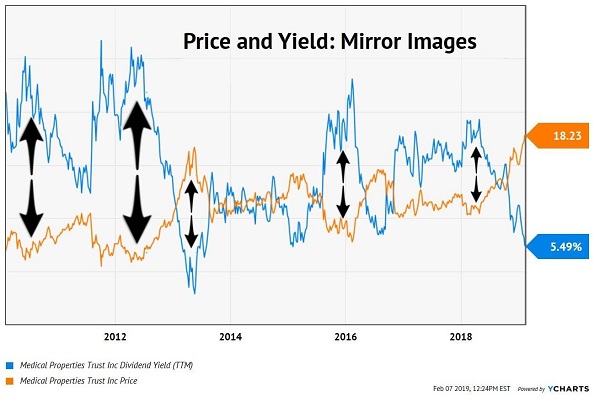

On the other hand, the recent “market froth” prompted me to sell one of our favorites. Fellow landlord Medical Properties Trust (MPW) is about as recession-proof and pullback-proof as it gets. The firm provides financing to hospitals and pays most of its profits to investors.

As with OHI, MPW’s stock price and yield are usually mirror images of each other:

With its yield near its all-time lows, it made sense to sell (and book our 109% total returns). Even the sleepy high yield space can experience mild bouts of irrational exuberance! Fortunately there are investments with more price upside that will actually give us a raise to boot (up to 7.5% dividends).

Introducing the “Pullback-Proof” Income Portfolio Paying 7.5%

The “cash or bear market” no-win quandary inspired me to put together my 5-stock “Pullback-Proof” portfolio, which I’m going to GIVE you today.

These 5 income wonders deliver 2 things “blue-chip pretenders” like General Mills and Target never could, such as:

- Rock-solid (and growing) 7.5% average cash dividends (more than my portfolio’s average).

- A share price that doesn’t crumble beneath your feet while you’re collecting these massive payouts. In fact, you can bank on 7% to 15% yearly price upside from these five “steady Eddie” picks.

With the Dow regularly lurching a stomach-churning 1,000 points (or more) in a single day during pullbacks, I’m sure safe—and growing—7.5% every single year would have a lot of appeal.

And remember, 7.5% is just the average! One of these titans pays a SAFE 8.5%.

Think about that for a second: buy this incredible stock now and every single year, nearly 9% of your original buy boomerangs straight back to you in CASH.

If that’s not the very definition of safety, I don’t know what is.

These five stout stocks have sailed through meltdown after meltdown with their share prices intact, doling out huge cash dividends the entire time. Owners of these amazing “pullback-proof” plays might have wondered what all the fuss was about!

These five “pullback-proof” wonders give you the best of both worlds: a 7.5% CASH dividend that jumps year in and year out (forever), with your feet firmly planted on a share price that holds steady in a market inferno and floats higher when stocks go Zen.

Recent Comments