“Hey Brett… you joined two partnerships last year?”

What? I didn’t. Or I thought I didn’t. In reality, I did–by buying shares in not one but two master limited partnerships (MLPs).

One of them was Enterprise Products Partners (EPD) and while I can’t recall the other, I can vividly the annoyed look on my accountant’s face like it was yesterday.

Master limited partnerships (MLPs) are required to issue you a K-1 package at the end of the tax year. These are generally headaches for the person who does your taxes (whether it’s you, or a professional).

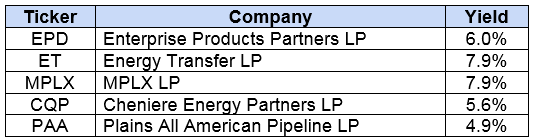

That year my accountant calmly but sternly asked me to stop buying MLPs in my personal portfolio. I agreed. But oh the dividends we passed up! Check out these current yields on the five largest “energy partnership” stocks:

It’s the “LP” after the name that’ll earn us the K-1 come tax time. But this isn’t a dead end. There is a way to buy a basket of these stocks for more yield and minus the K-1 hassle. We’ll discuss the details and the tickers in a minute. First, let’s look at the cash flows that power these payouts.

Pipelines, Profits and Payouts

MLPs themselves are, like many things in American culture, a successful product of the 1980s. Congress gave them the hall pass on federal taxes provided they pass along most of their profits to their “partners” (or shareholders) in the form of dividends. In this respect MLPs are quite similar to real estate investment trusts (REITs), which likewise must dish 90% of their income to shareholders as dividends.

While we think of REITs as landlords, MLPs operate like toll bridges. REITs collect rent checks while MLPs charge their customers for moving oil and natural gas from here to there.

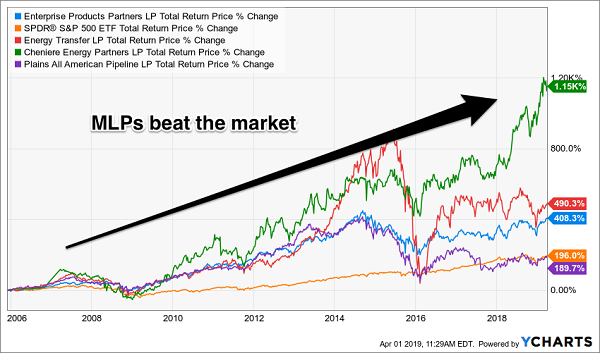

Also like REITs, MLPs do tend to outperform the broader stock market over time. Four of the five big MLPs above have been with us since the last energy boom and bust of the mid 00’s, and three of the four have handily beat the market:

Over Time, MLPs Outperform…

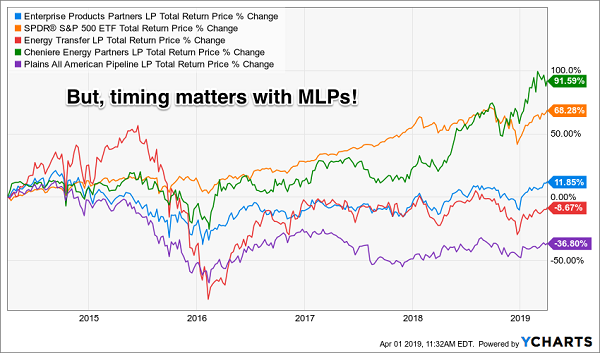

In theory MLPs can make money whether energy prices are high or low, being industry middlemen. In practice, they’ve broken hearts and bank accounts when energy slides. Over the last five years the four outperformers above have underachieved. In fact, two of them were money losers (even after dividends paid!)

… But Timing Matters!

What’d 2014 investors in these issues do wrong (other than securing five tax seasons of hassle)? They bought the line about MLPs being insulated from energy prices. In practice it’s much better to buy MLPs when energy prices are in the tank with nowhere to go but up.

And it’s an even better idea to buy funds of MLPs that will provide you with:

- Extra yield,

- A discount to the value of the stocks they own, and

- A way around the tax hassle.

9% MLP Yields for 92 Cents on the Dollar

Savvy contrarian income seekers are familiar with closed-end funds, or CEFs. They are similar in flavor to mutual funds and ETFs but better because their prices are simply inefficient.

They trade just like stocks. Their prices swing more wildly than their underlying value. They are subject to greedy legs up and fearful drops. Which makes them perfect for those of us who prefer to buy low–we get regular opportunities to do so!

Another benefit of buying your MLPs through CEFs is that they’ll replace your K-1 collection with one neat 1099 form. The latter is much easier for a tax professional, or you, to handle every April.

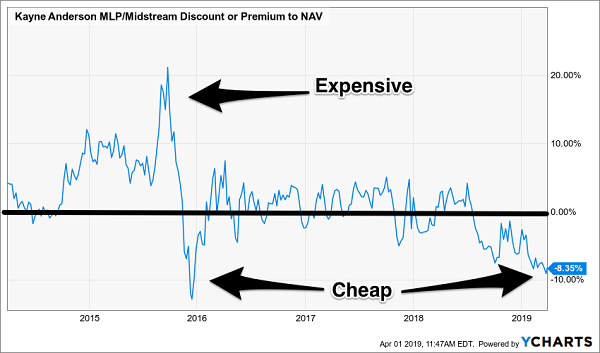

It’s better to buy these funds when energy prices are in the tank. For example, with oil down earlier this year I asked readers to consider the Kayne Anderson MLP Investment Fund (KYN), which was paying an amazing 11% and trading for just 94 cents on the dollar. KYN proceeded to rocket 17% higher in three months!

If you missed that run, well, you can blame me for not officially adding the fund to our Contrarian Income Report portfolio! Interestingly though the fund is actually cheaper today with respect to its net asset value (NAV, or the shares of the MLPs it holds). In fact the fund hasn’t been this discounted since the late-2015 MLP collapse:

KYN is Cheap (Per Its NAV)

Should we buy now? I would prefer to see a pullback in the price of oil first. According to my favorite contrarian indicators for the black goo, hedge fund managers are a bit too bullish on energy for my liking. And I’ve found that their sentiment is the driver of short-term oil prices. When they are greedy, the goo is more likely to drop in the coming weeks and months.

What about an ETF like the InfraCap MLP ETF (AMZA)? This is a rookie play on the sector because, as an ETF, the fund will never trade at a discount to the value of the shares it holds. As I write AMZA trades for a 0.1% premium while KYN fetches an 8.4% discount. Why would you pay $1.01 for a dollar in assets when 91.6 cents will do?

Plus KYN has outperformed AMZA since inception (even when accounting for fees). The lesson here, as always, is to buy a smart CEF and leave the basic ETF to the basic investors.

While I don’t quite like the current setup for MLPs, I do love the short and long-term prospects for five “pullback-proof” dividend payers yielding an average of 7.5%. If you’re worried about a pricey stock market that seems to defy gravity every day, here are five solid payouts you can purchase today without worrying about an overdue pullback.

Introducing the “Pullback-Proof” Income Portfolio Paying 7.5%

The “cash or bear market” no-win quandary inspired me to put together my 5-stock “Pullback-Proof” portfolio, which I’m going to GIVE you today.

These 5 income wonders deliver 2 things “blue-chip pretenders “like General Mills and Target never could, such as:

- Rock-solid (and growing) 7.5% average cash dividends (more than my portfolio’s average).

- A share price that doesn’t crumble beneath your feet while you’re collecting these massive payouts. In fact, you can bank on 7% to 15% yearly price upside from these five “steady Eddie” picks.

With the Dow regularly lurching a stomach-churning 1,000 points (or more) in a single day during pullbacks, I’m sure safe—and growing—7.5% every single year would have a lot of appeal.

And remember, 7.5% is just the average! One of these titans pays a SAFE 8.5%.

Think about that for a second: buy this incredible stock now and every single year, nearly 9% of your original buy boomerangs straight back to you in CASH.

If that’s not the very definition of safety, I don’t know what is.

These five stout stocks have sailed through meltdown after meltdown with their share prices intact, doling out huge cash dividends the entire time. Owners of these amazing “pullback-proof” plays might have wondered what all the fuss was about!

These five “pullback-proof” wonders give you the best of both worlds: a 7.5% CASH dividend that jumps year in and year out (forever), with your feet firmly planted on a share price that holds steady in a market inferno and floats higher when stocks go Zen.

Recent Comments