I’m about to show you 3 dividend powerhouses set to soar thanks to one of the most powerful (and misunderstood) profit indicators there is.

It involves the midterm elections—but only because the vote will remove some uncertainty and likely propel the market higher. But that’s only part of the story.

Because I fully expect this market to hold onto its midterm pop, then surge double-digits in 2019, thanks to the 1 proven indicator I’ll show you today.

90-Year-Old Indicator Signals Big Gains in 2019

I’m talking about a proven way to play the political calendar for 13%+ gains (plus dividends) in a single year.

Funny thing is, most people, blinded by their own politics, walk right past it. But whether you’re a Republican or a Democrat, for your portfolio’s sake, you need to keep an eye on the 4-year presidential cycle, no matter who’s in office.

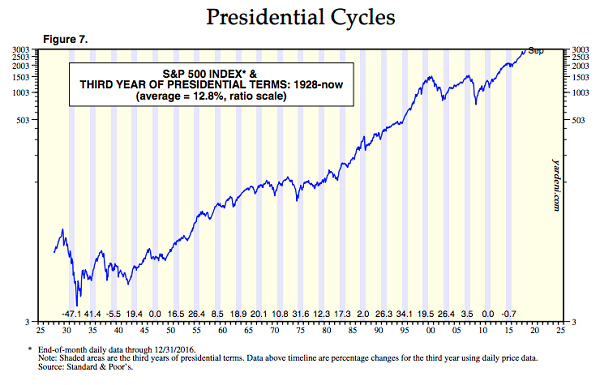

And you need to be all set to buy at the start of year 3, now just 2 months off, because it’s by far the most profitable. Check out the year 3’s average return, according to just-released figures from Yardeni Research:

Source: Yardeni Research

To put that 12.8% surge in context, it’s more than double the average rise for year 1 (5.2%), year 2 (4.8%) and year 4 (5.7%)!

Trump Joins the Establishment

One thing we can all agree on is that President Trump is different from any other president. So it’s fitting that his first-year pattern, juiced by a surging economy and tax reform, smashed the mold, with the S&P 500 popping 19.4%.

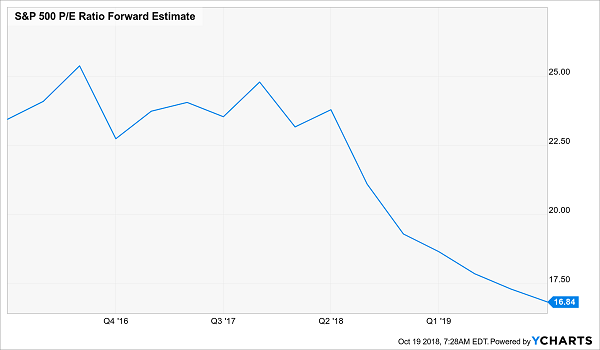

But his second year has fallen back to the trend so far, rising around 4%, right around the average. And with profits soaring and stocks trading at just 16.8-times forward earnings, down from 19.3 a year ago, we’re nicely teed up for double-digit gains in 2019.

Stocks Pick a Perfect Time to Go on Sale

And since a rising dividend is a crucial share-price driver, our top 3 buys are all growing their payouts at a fast clip.

Pick No. 1: A Dirt-Cheap Dividend Growing Double Digits

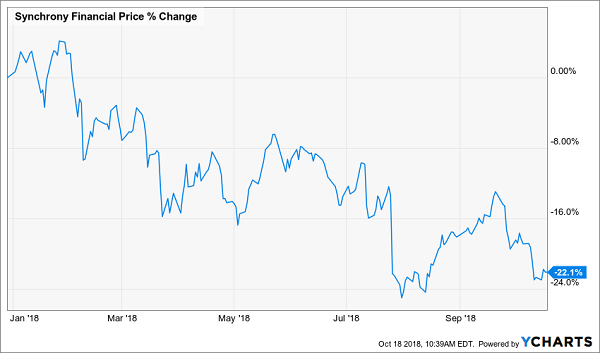

Synchrony Financial (SYF): A “year 3” boom could be just what the stock needs to break out of the rut it’s fallen into this year:

Punishment Doesn’t Fit the Crime

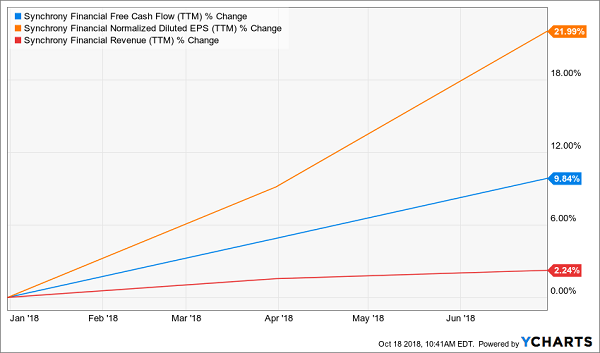

Now contrast that drop with the credit-card company’s revenue, earnings per share and free cash flow (FCF)—the lifeblood of any business:

Up, Up and Up

So what’s going on?

Simple: an overdone selloff because Synchrony lost its deal as the main credit-card supplier for Walmart (WMT). But there’s more here than meets the eye.

Because the loss still leaves Synchrony with two solid options when the deal expires in July 2019: sell the $10-billion portfolio or try to convert these customers to regular credit cards (and stop sharing the spoils with Walmart).

Meantime, the sales team has upped its game, inking deals with other big names, like its agreement with PayPal (PYPL), which closed in July, giving Synchrony $7.6 billion in loans and making it the exclusive credit issuer for PayPal in the US.

Synchrony is also quietly benefiting from rising rates, with interest and fee income jumping 10% in the third quarter. Other vital numbers also popped higher, like purchase volumes (up 11%), loan receivables (up 14%) and active accounts (up 9%, thanks in part to the PayPal deal).

The beauty of Synchrony is that its dividend, which yields 2.8%, jumped 40% in July and is a virtually guaranteed to keep growing because the company boasts an extremely low payout ratio—just 20% of earnings.

In a nutshell, that means management could more than double its dividend tomorrow and still not crack my 50% “safe zone” for a dividend-paying stock.

Finally, this stock trades at just 8.6 times forward earnings projections, well below its five-year average of 11.4. That gives us a lot of upside potential, and downside protection, too.

Pick No. 2: A Window Seat on an American Boom

With 70% of its passenger revenue coming from domestic flights, Delta Air Lines (DAL) is a terrific gauge of the US economy, and its third-quarter results tell us one thing: buckle up for more growth. Domestic passenger revenue jumped 9.2%, while cargo sales spiked 18.5%.

And Wall Street’s earnings forecasts are stratospheric, with a whopping 15% gain expected in 2019, to $6.37 a share. Delta trades at a very low 8.6-times that figure.

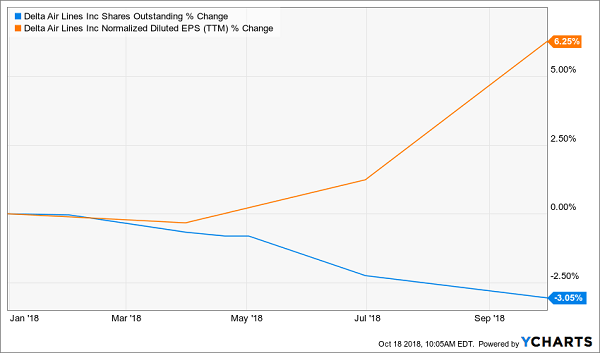

Fuel is Delta’s second-biggest cost, and its bill jumped 40% in Q3. But management is used to dealing with wild oil prices and deftly held the line on other costs, driving adjusted earnings per share (EPS) up 16%, to $1.80, crushing forecasts of $1.74.

Something else management does well? Pounce when the stock is cheap: in the past year, Delta bought back 3.1% of its shares, further juicing EPS (and the share price).

A Buyback Afterburner

All these moves are translating into a dividend that’s soared an annualized 43% since Delta started the payout in 2014, so you can look forward to yielding far more than the stock’s current 2.9% yield on your initial buy in no time.

Your next move? Buy now and grab some nice gains before the next big payout hike drops in mid-2019, putting even more lift under Delta stock.

Pick No. 3: Ride Rising Rates to 117%+ Dividend Growth

When it comes to real estate, for many folks, renting is a no-brainer.

To see why, look no further than the US 30-year mortgage rate, which has jumped 24% from a year ago, dusting many a homeownership dream:

Borrowed Cash Gets Pricier

Throw in the surging economy, which is pulling talent to hubs like San Francisco, LA and San Diego, and you get the perfect time to jump on our third pick, Essex Property Trust (ESS), which has been renting units in those locales since 1971.

Funny thing is, most folks have no clue! They think rising rates hurt REITs like Essex. That’s been proven wrong over and over, but it’s fine by us. We’ll use this overhyped fear to grab the stock cheap.

Cash Flow Soars, Investors Shrug

To see how asleep the herd is here, consider that Essex shares have barely budged all year, even though management has boosted full-year cash-flow estimate twice.

Result: you can now grab shares for 19.4-times FFO (funds from operations, REIT-speak for cash flow), the same level as you could on January 2!

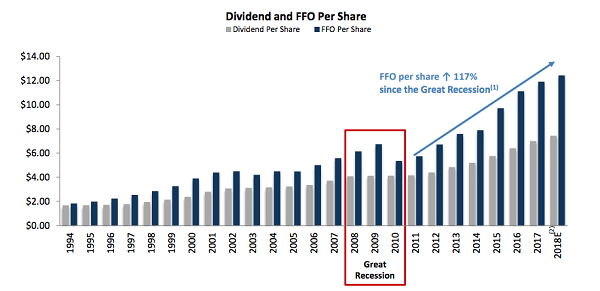

That’s an insult to management, which is doing everything right—growing FFO like a weed (up 5.7% in Q2), boosting the trust’s already high occupancy rate (96.7% vs. 96.4% a year ago) and passing cash from tenants to shareholders. Essex boasts a market-beating 3.1% yield now, and check out this dividend-growth record:

Source: Essex Property Trust 2018 corporate presentation

Let me leave you with one more reason to buy: Essex pays just 59% of its forecast 2018 FFO as dividends—in a REIT world where 85%+ ratios are common.

That puts big payout (and share price) growth firmly in play for 2019. Further upside from the election cycle is a bonus.

Revealed: Apple’s “Secret” 10.2% Dividend

What if I told you I’d found a way to take a big-name stock like Apple, with a paper-thin 1.7% current dividend, and turn it into a massive 10.2% cash stream?

Oh, and you can do it in just 1 click.

An Instant 6X Dividend Hike

Payouts like that mean up to $10,200 a year in dividends on a $100k investment. That’s 6 TIMES what you’d get from Apple’s “normal” payout!

Think about that for a second: incredible double-digit cash dividends right now—straight from the stocks you know well.

It’s that simple: no risky options, dangerous derivatives or short selling.

Just buy the stocks you love, straight from your online brokerage account. But instead of their paltry sub-2% dividends, you’ll get their “secret” payouts of 7.5%, 8% and even 10.2%!

The “Perfect Investment”

In know that sounds crazy, but I assure you it’s real.

It’s all thanks to an unsung group of investments I call “dividend conversion machines”—so named because they “convert” pathetic S&P 500 dividends into gigantic cash payouts.

They’re the closest thing I’ve ever seen to the perfect investment!

20%+ Price Gains … in 12 Months or Less

My team and I have pinpointed the 4 best Dividend Conversion Machines for your portfolio now, including that 10.2% payer I mentioned earlier.

Plus, we’ve got these 4 powerful investments pegged for massive price upside, too. I’m talking 20%+ gains, on top of those massive dividend payouts.

So to go back to our first example, you’d be set for $20,000 in gains, plus your $10,200 in dividends, just 12 months out from now.

A $30,200 windfall!

Recent Comments