Wall Street can have its casino. We’re going to look past the suits’ “common shares” and instead dial in some steady dividends—up to 10%!—that, for whatever reason, aren’t widely talked about on financial news channels and websites.

We income investors could care less what the S&P 500 or, heaven forbid, glue-sniffing NASDAQ, did in their daily session. When you’ve got “preferred” dividends funding your retirement, we can look down on those who roll the dice with their nest eggs.

These types of preferred-stock funds have a few key advantages:

- They pay their dividends monthly,

- They boast generous yields (between 5.4% and 10%, for example), and

- Their prices don’t drop nearly as much as the S&P or the NASDAQ during market fits.

That’s why I love “preferreds.”

Not Your Common Share Type

When you buy the likes of Apple (AAPL) or Amazon (AMZN), you’re buying what’s called a “common stock.” They’re all roughly the same: You enjoy price appreciation (or depreciation) depending on the company’s fortunes. Maybe you get a dividend, maybe you don’t. And in most cases, you get voting rights to boot.

Preferred stocks are built different. You don’t get a vote. And while shares can (and often do) appreciate, they’re not rapid movers.

No, the allure of preferreds is their big, fat and stable dividends, often yielding 6% or 7%, though some funds can squeeze out much more than that.

Because preferreds are more like bonds in that they’re far more difficult to research and value, most investors typically get exposure via diversified funds that hold dozens, if not hundreds, of preferred stocks at a time, and that typically write checks every single month.

In fact, that’s how I buy my preferreds.

But you can’t just close your eyes and pick a fund at random. Because preferred funds don’t offer a ton of price appreciation, it’s critical that you choose wisely—active management that can identify great values and underappreciated yields make the difference between so-so annual performance and stellar-yet-safe total returns.

So let’s look at both sides of the trade. I’ll introduce you to a few funds that might lure you in with name recognition or deceivingly high yields (so you can avoid them!), then I’ll show you some better options to help you lock in juicy monthly payouts while capitalizing on Washington’s perfect storm.

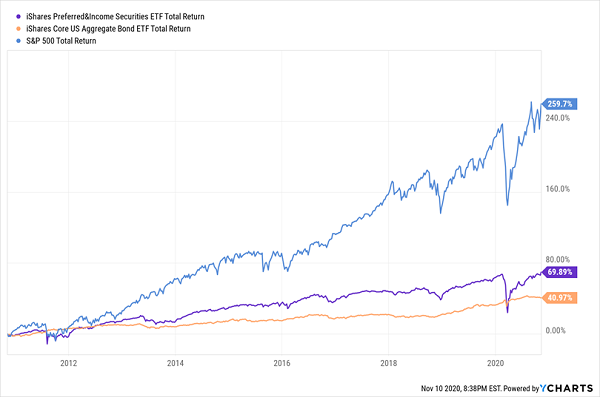

iShares Preferred & Income Securities (PFF)

SEC Yield: 5.4%

Let’s start with the iShares Preferred & Income Securities (PFF).

If you want simple, you want PFF. This basic index fund packs in more than 500 different domestic preferred issues, and it does so for a relatively low fee compared to actively managed products.

There’s nothing remarkable about the portfolio. More than 60% of the preferreds come from financial institutions such as Wells Fargo (WFC) and Bank of America (BAC), which is par for the course.

It’s a plain-Jane index fund, so no wonder that it acts as the unofficial benchmark for a lot of other preferred funds.

That sounds like a compliment. After all, the S&P 500 Index is the “benchmark” for many large-cap funds, and since most managers can’t beat it, those who do are considered pretty successful.

But PFF yields 5.4%. And its average annual return over the past decade? 5.4%.

PFF Is Barely Better Than Bonds

That math doesn’t add up.

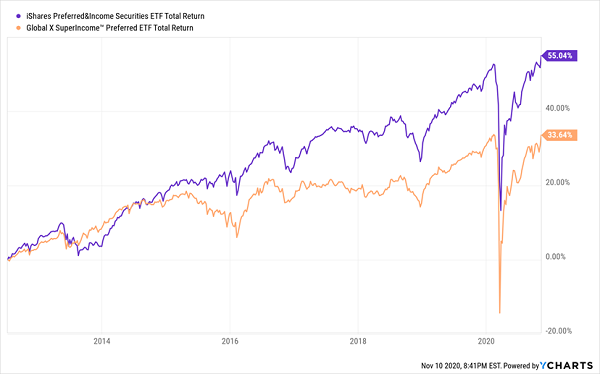

Global X SuperIncome Preferred ETF (SPFF)

SEC Yield: 6.0%

The Global X SuperIncome Preferred ETF (SPFF) tries to differentiate itself from the PFF by offering up more yield.

It’s not exactly subtle about it, either: It literally tracks the S&P Enhanced Yield North American Preferred Stock Index, which is made up of 50 of the highest-yielding preferred stocks in the U.S. and Canada.

Thing is, SPFF sacrifices quality for higher monthly payments—just 21% of the portfolio is investment-grade, with the lion’s share (41%) sitting in BB- to BB+ junk-rated preferreds. Your average preferred fund has nearly three times the investment-grade debt.

Shareholders don’t get much for this tradeoff. At the moment, Global X’s product yields just 60 basis points more than PFF, and you even lose part of that in higher fees (SPFF charges 0.58% to PFF’s 0.46%).

And then there’s the performance.

Lower-Quality Preferreds Take It on the Chin

SPFF perfectly exemplifies the risks of blindly chasing yield.

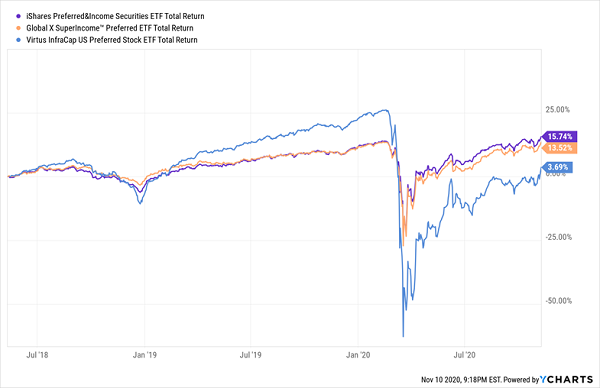

Virtus InfraCap U.S. Preferred Stock ETF (PFFA)

SEC Yield: 10.0%

When it comes to bonds and preferreds, active management is key. A seasoned manager can exploit mispriced preferreds and is better able to avoid potholes that many indexes, which have to buy whatever the computers spit out.

Enter Virtus InfraCap U.S. Preferred Stock ETF (PFFA), a rare actively managed ETF that invests in preferreds of companies with market caps of $100 million or more. Unlike SPFF, the focus is on total returns, not just yield—and yet, PFFA sports a massive double-digit yield of 10%, paid monthly.

That’s because PFFA uses a page out of the closed-end fund (CEF) playbook, utilizing typically 20% to 30% leverage and options strategies to juice both price performance and yield.

In theory, that’s enough to pique my interest, but it ultimately comes down to how management performs. And here’s what we know more than two years since the fund’s May 15, 2018, inception:

So Far, So Far Off the Mark

PFFA isn’t exactly a lost cause—it looks like it can amplify returns on upswings—but it’s clearly exposed to serious downside potential should the market flop.

Don’t Miss My “Crisis-Ready” 10% Monthly Payer Portfolio

PFFA is too risky for a retirement portfolio. Maybe management can learn a few things from 2020’s bear market, but there’s still not much track record to go on.

Fortunately, I know of a few monthly dividend payers that have already proven their ability to line investors’ pockets, and are nestled perfectly within my “buy-in” range right now.

My 10% Monthly Payer Portfolio is an “all-weather” portfolio that doesn’t need a perfect economic environment to churn out all-star income and market-beating gains.

I’ve personally hand-picked and safety-checked this unique portfolio, from every angle, for maximum safety. That includes a can’t-miss 7%-yielding preferred-stock fund that—unlike PFF, SPFF and PFFA—is actually increasing its cash distributions.

It’s a combination of stocks and funds that are so cheap that they could easily hold their own, even if political tumult and a COVID “second wave” put the market’s recent rally on ice—but if the rally does pick up steam, watch out above!

Either way, we’ll be soaking up 10% average yields the whole time!

These picks deliver truly life-changing dividends: In fact, if you drop $500K into this powerful portfolio right now, you’ll kick-start a $50,000 income stream.

That’s $4,166 a month in regular income checks!

Now is the time to get in, while you can still do so at a bargain. Click here to get everything you need—names, tickers, dividend histories and more.

Recent Comments