With a recession likely at some point, we’re going to focus our attention today on recession-resistant dividend stocks.

With all the talk of a “soft landing” or even “no landing”—the nightmare inflation scenario in which the economy keeps humming—we contrarians are going to take a step back. And respect the yield curve.

In a normal economy, longer-dated bonds would pay more than shorter-dated issues. After all, more time, more things that can go wrong. Which is why you and I are smartly prepping for a recession, regardless of what the latest financial narrative is.

The 10-year Treasury bond has paid less than its 2-year cousin for many months and counting. This is reason enough for us income investors to be cautious:

Why We’re Discussing Recession-Resistant Dividends

Our recession hack? Low-volatility dividend stocks.

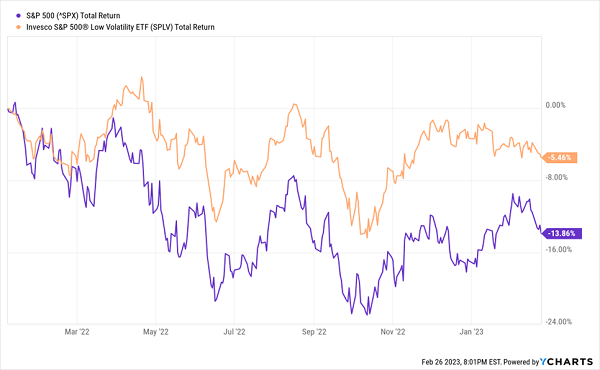

“Low vol” is an industry buzzword during scary times. And for good reason—it works. Let’s take the 2022-23 bear as an example. A low vol basket has done much “less bad” than the broader stock market.

Low Vol Has Been “Less Bad” Lately

How do we find low-volatility stocks? Well, we look for low “beta,” which is how much (or how little!) an investment moves compared to some benchmark. So naturally, with stocks, beta usually measures a stock’s movement against the S&P 500.

For example: Let’s say a stock has a beta of 0.75. That means, broadly speaking, when the S&P 500 drops by 1% in a day, the stock will probably only drop by 0.75%. It hardly ever works out that perfectly on a daily basis, but over time, lower-beta stocks typically have much calmer stock movement.

Let’s chat about seven secure payers that yield 4.4% to 6.3% and move less than the broader market.

Utilities

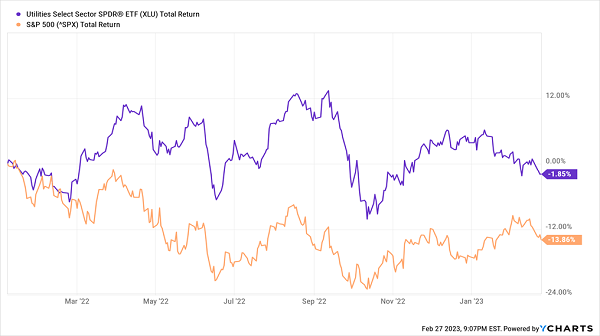

Few things say “low-volatility” and “recession-resistant” more than utility stocks, which can keep on humming because what they serve—electricity, natural gas, and water—are the bare necessities of life.

Utilities Haven’t Given Up Much Ground

Three utility players check off a lot of boxes at the moment:

- OGE Energy (OGE, 4.5% yield) should be a familiar name if you’re a regular reader. OGE recently merged its midstream business with Energy Transfer LP (ET) to become a pure-play electric utility; its OG&E (Oklahoma Gas & Electric) subsidiary currently serves roughly 900,000 customers across Oklahoma and Arkansas. Simply put: It’s a well-managed company that keeps costs down and dividends up. It’s a smooth operator, too, with one-year (0.63) and five-year (0.67) betas that suggest the stock is roughly a third less volatile than the broader market. Sadly, like the last time I covered OGE, the stock remains prohibitively expensive.

- Pinnacle West Capital (PNW, 4.7% yield) might sound like a business development company (BDC), but it’s actually an electric utility that serves nearly 1.3 million Arizona customers via its Arizona Public Service and Bright Canyon Energy subsidiaries. In addition to a high yield, it has a one-year (short-term) beta of 0.70, and a five-year (long-term) beta of just 0.43—the latter means that over the past five years, PNW has been less than half as volatile as the broader market! Not bad. But it’s still mired by a regulatory action from a couple of years ago; the utility actually posted a 21-cent-per-share loss in the most recent quarter.

- NorthWestern Corporation (NWE, 4.4% yield) reflects a growing trend in the utility space in that it’s heavy in clean energy. NWE says 44% of the energy it provides for South Dakota comes from wind projects, and 59% of its generation in Montana is from carbon-free sources. (It also powers parts of Nebraska.) Again, you can’t ask for a steadier stock, given one- and five-year betas of 0.45 and 0.46, respectively. But it’s priced for perfection, at a price/growth-to-earnings ratio of 4 (where anything above 1 is considered overpriced). Clearly, investors have already piled into the stock seeking safety.

Consumer Staples

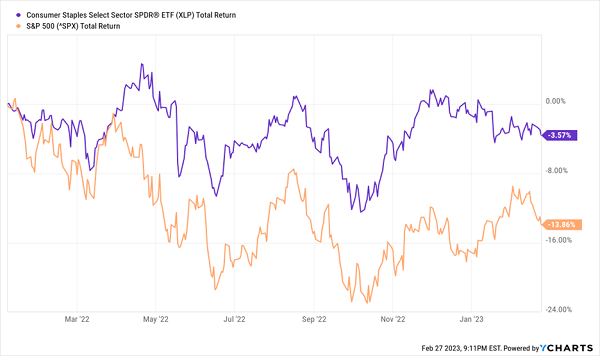

Every bit as necessary as electricity, nat-gas and water are food, toiletries and—well, cigarettes.

OK, you might not necessarily consider tobacco a necessity, but the companies that sell tobacco sure act like consumer staples. And that’s a good thing.

Staples Have Also Held Their Ground

Philip Morris International (PM, 5.2% yield) is one of the biggest names in tobacco, selling Marlboro worldwide, as well as Parliament, Chesterfield and numerous other cigarette brands.

But what makes PM interesting is its goal of becoming mostly smoke-free by 2025. Philip Morris has greatly expanded its smokeless product portfolio to meet those means: Iqos, Lil, Veeba, Shiro. And more recently, it acquired Swedish Match, which makes Snus nicotine pouches, moist snuff and related products.

And despite the constantly rising prices of tobacco products, PM’s wares remain recession-proof and volatility-proof. The company’s one-year beta of 0.76 and five-year beta of 0.71 show that investing in Philip Morris involves much calmer seas than the S&P 500. A 5%-plus yield also keeps investors interested when they know price gains could be thin.

Again, though, you’re buying high for this protection.

Less worrisome from a price perspective is Universal Corp. (UVV, 6.2% yield), which is a truly unique tobacco play. That’s because it doesn’t produce cigarettes—it supplies the tobacco that goes in the cigarettes. Specifically, it’s a supplier for producers across 30 companies on five continents. And its business is further diversified via a separate ingredients operation that includes FruitSmart, Shank’s Extracts and Silva International.

It’s a beautifully boring, behind-the-scenes play in consumer staples. And it acts like it. Its five-year beta of 0.70 is plenty low, and a 0.42 one-year beta is downright sleepy.

Financials

Financial stocks are the ultimate cyclical sector—historically, these are not stocks you want to own in a recession.

And Yet, Here We Are

But you can’t just pick any ol’ bank and hope to do well in a downturn.

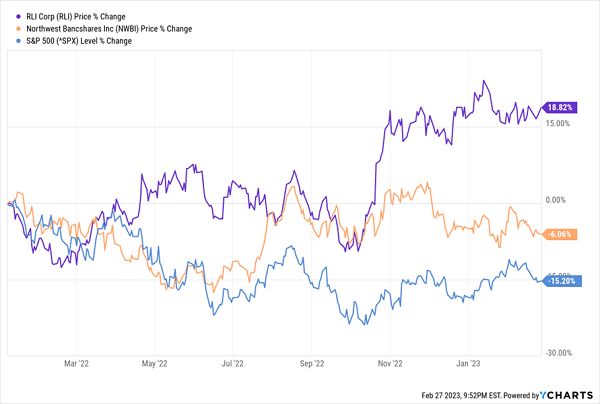

Illinois-headquartered insurer RLI Corp. (RLI, 6.3% yield) is a specialty insurer that provides business insurance, personal insurance and surety bonds, among other products. Its high-growth property insurance division has drawn interest of late—a sign that RLI isn’t just somewhere to get high dividends and low volatility (0.55 one-year beta, 0.42 five-year beta), but real long-term growth potential. It is worth noting, however, that the yield is heavily propped up by special dividends. RLI paid out $8.04 in dividends over the past 12 months, but $7.00 of that was a special payout. On the one hand, these special dividends have occurred for years on end and allow RLI to pay more when its profits allow; on the other hand, you can’t count on that full 6%-plus in yield year in and year out.

Northwest Bancshares (NWBI, 5.6% yield) is a more traditional payer, and every cent of its 5.6% yield is from regular dividends. NWBI is the holding company behind regional financial Northwest Bank, which operates 142 full-service community centers in Ohio, Pennsylvania, Indiana and New York. What makes NWBI a stronger recession play compared to most financials is its comparatively lower-risk loan profile, not to mention extremely low betas of 0.50 (one-year) and 0.59 (five-year).

It’s Not Too Late: Lock In the “Recession-Resistant Portfolio” Now!

The seven stocks above sport the kinds of pivotal strengths we need as we march right into the mouth of a likely recession.

But the ultimate survivors of 2023 will need to share one trait above all others:

Recession-resistance.

While every major market index was dead money in 2022, and while most of the darlings of the stock market have been getting crushed, a small, overlooked basket of recession-resistant stocks haven’t just been surviving—they’ve been setting up to thrive.

And now, they look like they could be the market’s best protective plays heading into a turbulent 2023.

To the uninformed investor, these stocks will seem downright boring. In fact, I’m betting that you haven’t heard of any of these—after all, the mainstream media rarely covers some of them, and it outright ignores others.

But these “Hidden Yield stocks” offer savvy investors the potential to double their money roughly every five years, regardless of what the wider market does.

How can they do this when even idiot-proof blue chips can’t?

It all boils down to what I call “The Three Pillars”:

Pillar #1: Consistent Dividend Hikes

Pillar #2: Lagging Stock Price

Pillar #3: Stock Buybacks

Selecting companies with a proven track of increasing their dividend payments is the safest, most reliable way to get rich in the stock market. And I want to show you how it’s done. Click here for details and discover how to get a copy of my 5 Recession-Resistant Dividend Stocks report, including full analyses of each pick right now!

Recent Comments