Insiders may sell their shares for a variety of reasons. Usually, because they need the cash.

But execs who know “what’s up” with their company better than anyone only buy with one purpose in mind.

They believe their stock price is going higher. Or, if it’s a dividend stock, at least it is not going down anytime soon!

We’re going to highlight dividends up to 15.8% (yes, that’s no typo) with recent insider buying. This is especially notable these days because:

- Vanilla investors are worried this is 2008, Part Deux.

- Inflation is still running hot.

- And stocks have been going down for 15 months and counting.

Our buyers today? True dividend believers. Let’s start with Elizabeth and Brian, who saw their firm’s fat 15.8% yield—and threw down their own money.

FS KKR Capital (FSK)

Dividend Yield: 15.8%

Recent Noteworthy Buys:

- Director Elizabeth Sandler: 2,500 shares ($49,100) on 3/9/23

- Co-President Brian Gerson: 3,000 shares ($59,070) on 3/7/23

Let’s start with a BDC, which stands for “business development company” (but could also stand for “big dividend company.”)

BDCs do what many banks won’t, providing financing to small and midsize businesses. They’re similar to real estate investment trusts (REITs) in that they were created by Congress to spur investment in a less-accessible sector. And like REITs, they must pay shareholders at least 90% of their profits in the form of dividends.

Big, fat dividends.

FS KKR Capital (FSK) serves up an especially plump payout—a nearly 16% figure that puts even most of its industry mates to shame.

The underlying business is providing financing to private middle-market companies, primarily by investing in senior secured debt (~70%), though it’s also happy to deal in subordinated debt and other financing. Its 197 portfolio companies are spread across 22 industries, including software and services, capital goods, real estate, retailing and more. It also has low-single-digit exposure to Credit Opportunities Partners JV, a joint venture with South Carolina Retirement Systems Group Trust that invests capital across a range of investments.

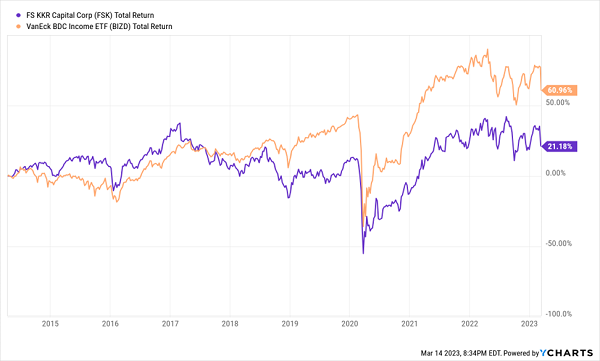

FS KKR Capital has historically been a weak operator, consistently underperforming the BDC industry. That has resulted in a perpetually dirt-cheap discount to NAV—FSK currently trades at just 71 cents on the dollar!

FSK Is Largely Behind the Curve

FSK is also difficult to recommend to retirement-income hunters because of, well, a faint hint of volatility in the payout.

Yikes.

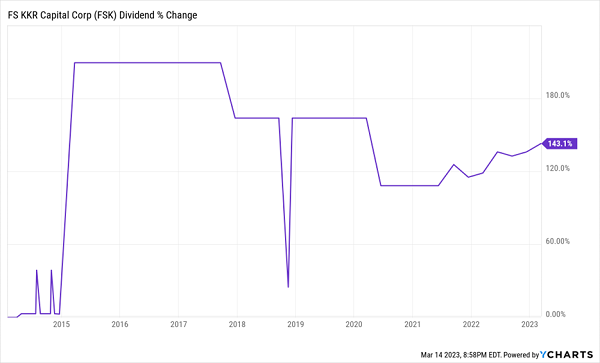

To FSK’s credit, things are starting to look up.

The last quarter saw FS KKR deliver better-than-expected net interest income (NII) and raise its core dividend for Q1 2023 to 64 cents quarterly, from 61 cents in 2022. The company also plans to augment that dividend with a 6-cent quarterly supplemental distribution, which it expects to pay throughout the year. Dividend coverage for the prior quarter was 116%, providing some confidence in the payout.

FSK’s top brass seems to be optimistic about the dividend, too. Execs Elizabeth Sandler and Brian Gerson collectively plunked down nearly $110,000 to buy more stock within a few days of one another.

Energy Transfer LP (ET)

Distribution Yield: 9.9%

Recent Noteworthy Buys:

- Executive Chairman Kelcy L. Warren: 1,660,602 shares ($21.7 million) on 2/27/23

- Executive Chairman Kelcy L. Warren: 1,339,398 shares ($17.4 million) on 2/23/23

It’s hard not to notice someone gobbling up nearly $40 million in stock in roughly a week. And that’s exactly what billionaire Kelcy Warren did during the final innings of February.

Warren, by the way, is the co-founder and current executive chairman of master limited partnership Energy Transfer LP (ET), and he’s only a couple years removed from stepping down from the CEO role.

Energy Transfer is responsible for 120,000 miles of America’s energy infrastructure—according to the company, some 30% of the country’s natural gas and crude oil moves through its pipelines.

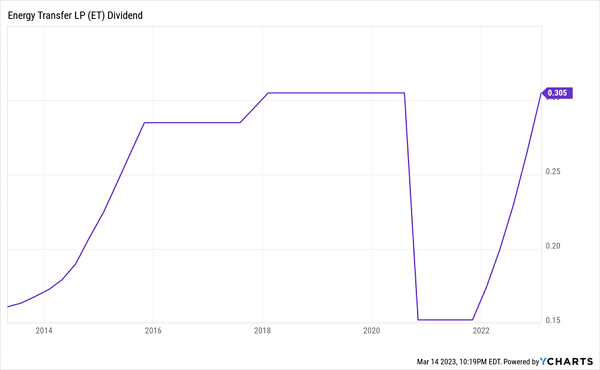

Like most energy names, Energy Transfer was eviscerated during COVID’s “zero oil” crisis. The distribution followed suit, getting halved midway through 2020 to 15.25 cents per unit from 30.5 cents.

But the company has bounced back in a big way. ET has reported several consecutive record-setting quarters, including a blowout Q4 2022 that saw natural gas liquid (NGL) fractionation volumes, transportation volumes, midstream throughput volumes and several other operational metrics set partnership records.

Also over the past few quarters, Energy Transfer has been aggressively restoring the payout. And as we predicted, ET announced another rate hike in late January—bringing the distribution back to its pre-COVID-crash 30.5 cents per unit.

ET’s Distribution Crisis Is Done

Warren, who co-founded ET in 1996, is happy to keep snapping up shares, to the tune of roughly $40 million in late February. I’ll also point out that Energy Transfer saw additional bullish buying back in December—some 80,000 shares worth $924,000 by Director Richard Brannon.

VF Corp. (VFC)

Dividend Yield: 5.8%

Recent Noteworthy Buys:

- Director Juliana L. Chugg: 15,000 shares ($400,350) on 2/13/23

VF Corp. (VFC) is a collection of apparel brands mostly focused on the great outdoors, including Vans, The North Face and Timberland. Though it’s rapidly shedding brands. It got rid of Wrangler and Lee jeans in 2019’s Kontoor Brands (KTB) spinoff, and this year, VFC announced it was selling Eastpak, JanSport, and Kipling.

That latter move is being made to shore up an increasingly problematic balance sheet, which has taken a drubbing over the past few years amid COVID, supply-chain chaos and changes in fashion trends.

And VFC’s Balance Sheet Isn’t the Only Thing Taking a Beating

The “come to Jesus” moment finally came in February of this year, when VF Corp. reported fiscal third-quarter earnings. The company announced a slew of measures meant to “restore financial strength,” including:

- Halting share buybacks

- Selling off the aforementioned brands

- Asset sales, including a sale/leaseback of its international headquarters

- Cost cutting to save $225 million annually by the end of 2024

But the biggest hammer to fall was a 41% cut to the dividend, to 30 cents per share—all but effectively guaranteeing that VFC’s half-century run of uninterrupted dividend hikes will come to an end, as will its membership in the Dividend Aristocrats.

All of the above is what makes this insider buy so intriguing. VF Corp. announced all of this bad news on Feb. 7. And less than a week later, Director Juliana L. Chugg dropped 400 grand on 15,000 shares.

To be fair, she probably believes the dividend is much more stable now. Up until VFC hacked its cash distribution, the stock sported a high-single-digit yield, but also an unsustainable payout ratio. Following the cut, VF Corp. is projected to pay just a little more than half its 2024 profits out as dividends—while still offering up a 5%-plus yield at current prices.

Give Me 4 Minutes, I’ll 4X Your Retirement Income

But would you really feel comfortable planning your retirement around a dividend that’s just been hacked into pieces?

I know I wouldn’t.

I want a cozy, comfortable retirement without bleeding my nest egg dry. And I’m pretty sure you want the same thing, too.

But to get that, we have to do better than a soon-to-be-ejected Dividend Aristocrat. We need to be able to plan around our income with laser precision.

Which is why we only hold dependable payers in our “Perfect Income” portfolio.

What makes these dividend holdings “perfect”?

- They pay you consistently, predictably and reliably.

- They’re built to survive—even thrive—in market crashes.

- They deliver double-digit returns, with safe, secure investments.

- They take just a few minutes every month to “manage.”

- They DON’T involve day trading, buying on margin or any other risky strategy.

- They DON’T involve gambling on penny stocks, Bitcoin or buying puts and calls.

Getting each and every one of these things from any single holding might sound impossible. But it’s par for the course for every position in my “Perfect Income” portfolio.

Let me show you the stocks and funds you need to stabilize your retirement. But more importantly, let me teach you more about this incredible strategy itself and make you a better investor in the process!

Take control of your financial legacy today. Click here for my newly updated briefing on the Perfect Income Portfolio!

Recent Comments