In a recent survey of CEF Insider readers, a few asked me whether I prefer equity or debt closed-end funds (CEFs) and why.

It’s an intriguing question because the two fund types act very differently. So let’s dive into these differences, and the benefits both breeds offer, so you’ll know which fits best in your portfolio now.

Equity Vs. Debt Funds

Put simply, an equity CEF has more than half its assets in stocks, while a debt CEF has more than half its assets in debts—usually corporate bonds, junk bonds or municipal bonds. Sometimes the lines get blurred, like with convertible-bond funds that also buy stocks. But in most cases, a CEF will focus either on stocks or one type of bond or another.

Of the nearly 500 CEFs tracked by CEF Insider, 206 are equity funds and 293 are debt funds, with municipal-bond funds being the most popular (162 such CEFs are out there).

Something else to keep in mind: it takes different skills to manage an equity or a debt fund: plenty of big-name firms, like BlackRock and Eaton Vance, manage both, but the individuals running each are almost always different people. (And there are plenty of smaller firms specializing in one or the other, as well.)

Headline Number Deceives

So what’s the bottom line here? To get to that, we’ll start with the 30,000-foot view.

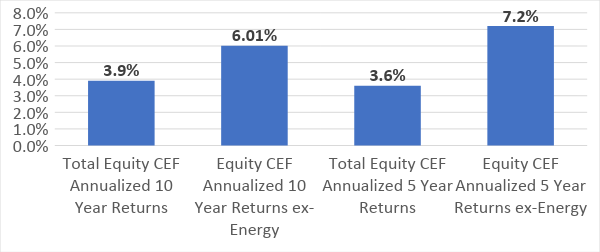

Over the last decade, equity funds have put up a 3.9% annualized total return, while debt funds have returned an annualized 6.1%.

So case closed, right? Debt funds are the way to go.

Not so fast.

Because there’s a big swing factor here, and that’s energy. Many energy CEFs came out just as oil crashed in 2014, and that drags down returns a lot. Cut out energy and suddenly equity-CEF returns pop to 6% annualized over the last decade.

Less Energy, Higher Returns

Source: CEF Insider

The way energy obscures the picture for equity CEFs is just one way people misunderstand the power of these funds. The other is in cash flow.

Remember that CEFs have high dividends—an average 6.5% payout, far above what you’ll get from even high-yield ETFs. This is a secret source of gains many people just don’t get.

Let’s say you bought an S&P 500 ETF, like the Vanguard S&P 500 ETF (VOO) or the SPDR S&P 500 ETF (SPY). Either would get you a dividend below 2%. But if you wanted, say, a 6% income stream from your investments, you’d need to sell shares every so often to supplement the low dividend.

And that’s a problem.

By doing so with an index fund, you’d sell during downturns like the ones we’ve seen all month. That would mean selling at a loss when you should be snapping up bargains.

CEFs avoid this problem. By having professional managers control the buying and selling (and sustaining the high payout), you won’t need to sell into a downturn for cash flow.

Which brings me to my next point: the discount.

Right now, equity funds’ average discount to NAV is 6.8%. This is the one drawback of equity funds: their discounts tend to be narrower than those of debt funds, mainly because investors are more confident that equity funds can sell their assets in a correction.

But there’s a silver lining: the outlier opportunity. If an equity fund’s discount swings out much wider than the norm, it will tend to snap back fast, letting us grab a nice gain or jump on an unusually high (and sustainable) dividend yield.

Unloved Debt Funds Set to Rebound

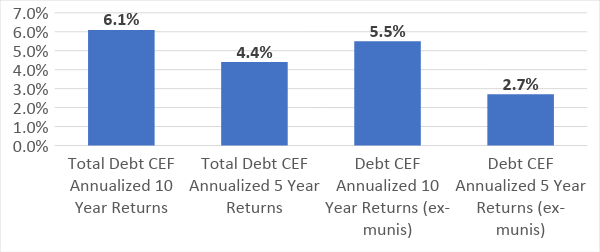

The best thing about debt funds, as I touched on earlier, is their bigger returns. But this is misleading, as this chart shows:

Better Returns Quickly Disappearing

Source: CEF Insider

Here we see that debt CEFs’ returns have been falling; while we got 6.1% per year over the last decade for all debt CEFs, that’s fallen to 4.4% in the last 5 years. More crucially, debt-CEF returns have come to lean more heavily on municipal-bond CEFs: without munis, returns slip to 5.5% per year in the last decade to 2.7% per year for in the last 5 years.

Why the big change between the 10- and 5-year timeframes?

This accelerated in 2015, with rate-hike fears scaring speculators away from high-yield and corporate bonds, which crushed a lot of debt returns in the shorter term. But that’s also an opportunity; those weaker returns also mean much bigger discounts for these funds—including the 107 debt CEFs that have had over 6% annualized returns in the last 5 years and the 24 that have had over 9% annualized returns in the same period.

Since buying CEFs when their discounts are unusually large tends to trigger unusually large returns, that means the bad news for debt CEFs in the last 5 years is becoming good news for CEF investors.

Revealed: My Top 4 CEFs for 7.1%+ Yields and Fast 20% Upside

Here’s the best news: I’ve done all the research necessary to find the best high-yield CEFs out there—so you don’t have to.

The result is a FREE Special Report unlike any we’ve published before. In its pages you’ll find the 4 CEFs I’ve handpicked for strong growth and high—and growing—dividends in the years ahead.

I’ve been analyzing CEFs for years—I’m one of only a handful of analysts who dedicates 100% of their time to these unique funds—and I’ve come to just one conclusion:

If you want to build a portfolio that can keep your retirement income safe—and growing—when the next crash hits, holding at least one or two of these 4 funds is an absolute must.

Here’s why:

- Life-Changing Dividends: The 4 CEFs in my new Special Report boast 7.1% CASH payouts, on average—4 TIMES MORE than your typical S&P 500 stock.

- BIG Upside: All 4 of these low-key funds have been completely ignored as the herd stampedes into the big names in the CEF world. That’s left them trading at ridiculous discounts to NAV. But that won’t last. When these weird markdowns snap shut, they’ll catapult us to 20%+ price gains!

Add it all up and you’re looking at a nearly 30% total return in the next 12 months here, with a big chunk of that in CASH.

I’ve put everything you need to know about these 4 stealth funds in my NEW special report—which is waiting for you now.

Recent Comments