Stocks or bonds? For income-focused investors, why not blend the best of both worlds to collect interest and enjoy share price upside?

This is the goal of convertible bonds, a “country club” favorite. (Before the holidays you may be tempted to add some convertibles to your portfolio simply so that you can brag about them to friends and family!)

Convertible bonds, like the preferred shares we discussed last week, pay regular interest. In this way, they act like bonds. You buy them and “lock in” regular coupon payments.

But convertibles are also like stock options in that they can be “converted” from a bond to a share of stock by the holder. So you can think of them as bonds with some stock-like upside.

Switching from creditor to shareholder can be a lucrative move. But buying convertibles does require individual research – and heartburn. Take Tesla’s (TSLA) debt that holders can “convert” next March into Tesla stock for a $359.87 conversion price. Today that’d be an underwater trade for bondholders, with the stock price about $15 lower. This means investors are likely to continue holding Tesla bonds rather than pay $15 per share out of pocket to own the stock:

These Bond Holders Have Heartburn

This sounds fine until we consider that convertibles already pay less interest than regular bonds because of their additional lottery ticket potential. When we buy convertibles, we need upside – and we’re not amused when Elon Musk’s “antics” send his company’s share price lower.

I’d rather save us the research, headaches and heartburn by “outsourcing” our convertible bond portfolios to industry experts. As usual, we’ll look to closed-end funds here for three reasons.

First, we can find CEFs that pay more than individual convertibles we’d be able to buy. Fund managers get the first phone call on these types of deals. Plus, they have access to cheap money that lets them leverage their returns relatively safely. We’re going to discuss an excellent convertible-focused CEF fund yielding 5.9% in a moment.

Second, CEFs can (and often do) trade for discounts to their net asset values (or NAVs – the street value of the convertible bonds they hold). Thanks to current pessimism in CEF-land, the fund I’m going to highlight trades for just 87 cents on the dollar.

Third, we can hire a manager like Thomas Dinsmore to work for us for free. He usually charges a 1.1% management fee, but thanks to his Ellsworth Growth and Income Fund’s (ECF) current 13% discount, Dinsmore’s remuneration is “comped.”

For you Contrarian Income Report subscribers, this discussion on convertibles may ring a bell. Our asset manager Nuveen recently expanded its Preferred & Income Securities Fund’s (JPS) mandate. Along with preferred securities, the fund began buying hybrids such as convertible securities. (Again, this is a fancy way of saying the fund started purchasing debt that has options to convert to equity.) I advised subscribers not to worry about JPS’ mandate change because we trust the management team.

While few know JPS, more aspiring country clubbers know CWB. The SPDR Barclays Capital Convertible Bond ETF (CWB) is the most popular mainstream (read: widely marketed) vehicle to purchase convertibles. It lets investors brag that they own a basket of convertible bonds. But if their friends are impressed, their accountants are not.

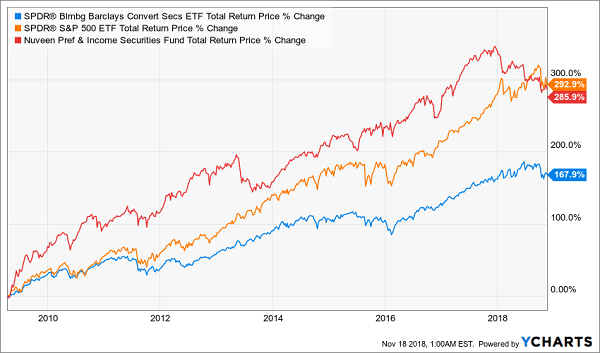

CWB has, on the surface, been fine. It’s generated 168% returns over the last ten years:

Putting CWB’s +168% Gains in Perspective

The problem is that its stock market competition, the S&P 500, returned 293%, and its bond market competition, JPS, returned 286%. Which means this “dumb ETF” blended the two strategies and did worse than them both!

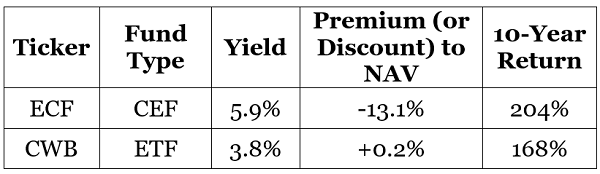

We have one “pure play” option in CEF-land that meets our criteria as a potential investment. Dinsmore’s fund ECF pays 5.9% today (versus CWB’s 3.8% yield) and trades at a generous discount to its NAV (versus a slight premium for CWB):

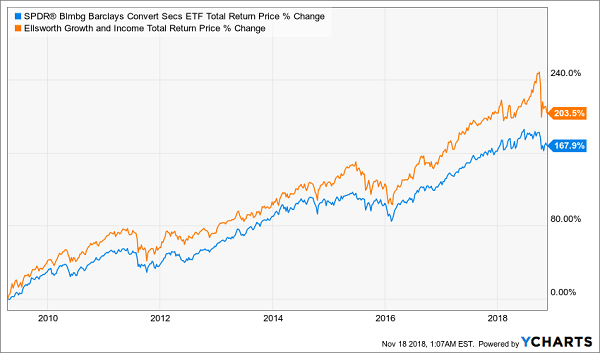

ECF has returned a tidy 6% on its portfolio since inception and it’s outperformed its too-popular ETF cousin over the past ten years as well. Including dividends, ECF has generated 204% profits versus our only 168% for CWB:

Once Again, the Smart CEF Money Wins

So should we run and add ECF to our “No Withdrawal” Retirement Portfolio? Not yet. I actually prefer three other CEFs as smart “back door” ways to play convertible bonds. And all three of my “best fund buys” boast 8%+ yields right now. Here are the details.

Retire on Just $500K with These CEFs Paying up to 9.4%

Secure closed-end bond funds are a cornerstone of my 8% “no withdrawal” retirement strategy, which lets retirees rely entirely on dividend income and leave their principal 100% intact.

Well, it’s actually even better than that.

Retirees who follow this strategy enjoy principal that is more than 100% intact thanks to price gain potential. Remember, ECF alone contains 13 cents per dollar per share in “free money” that is available today thanks to its discount to NAV. When the fund swings back into favor and this bargain window closes, investors will enjoy price gains in addition to their generous yields.

Plus investors who buy heavily discounted funds today will lock in more “dividends for their dollar” for life. This is the ultimate dividends-only retirement strategy.

To achieve this, I research and recommend only elite closed-end funds that:

- Pay 8% or better…

- Have well-funded distributions…

- Trade at meaningful discounts to their NAV…

- And know how to make their shareholders money.

Plus I talk to management, because online research isn’t enough. I also track insider buying to make sure these guys have real skin in the game.

Today, I like three “blue chip” closed-end funds as best income buys. And wait ‘til you see their yields! These “slam dunk” income plays pay all the way up to 9.4% dividends.

Plus, they trade at 10% to 15% discounts to their net asset value (NAV) today. Which means they’re perfect for your retirement portfolio because your downside risk is minimal. Even if the market takes a tumble, these top-notch funds will simply trade flat… and we’ll still collect those fat dividends!

If you’re an investor who strives to live off dividends alone, while slowly but safely increasing the value of your nest egg, these are the ideal holdings for you. Click here and I’ll explain more about my no-withdrawal approach.

Recent Comments