Most folks think retiring on $527K is a dream—but most folks haven’t heard of high-yield closed end funds (CEFs). With yields as high as 22%, these unsung income plays can fast-track your race to financial independence.

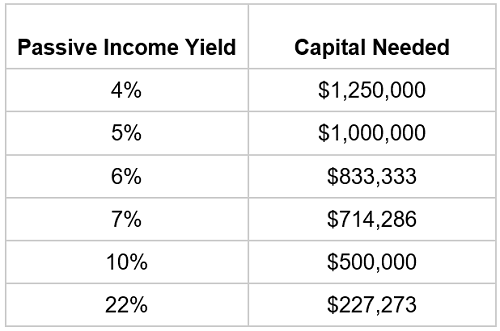

Here’s how: let’s say you’re looking to clock out and use your portfolio to replace $50,000 in yearly employment income. Many financial advisors will tell you that the most you can withdraw out of a conservative stock portfolio is 4% a year (this is known as the 4% safe withdrawal rate). Simple math tells us that this means you will need $1,250,000 to retire.

High-yield investments like CEFs turbocharge that because we’ll need less capital to get that $50,000 annual income stream. If we can find an investment giving us a 5% yield, we only need a million, so we could reduce the amount we’d need to save by $250,000. And if we can get higher yields, we can cut it down even more.

The Bigger the Yield, the Less Needed to Save

So it follows that a retiree who finds a 7% passive income stream needs half a million dollars less than a retiree blindly following their financial advisor.

But is a safe 7% dividend stream possible? With CEFs, the answer is a resounding yes.

CEFs are designed to invest in familiar assets—stocks, bonds and real estate investment trusts (REITs), for example—but are professionally managed to buy and sell assets at the best possible time to hand out a high income stream to investors. The best CEFs yield 7% or more and have done so for over a decade without cutting their payouts.

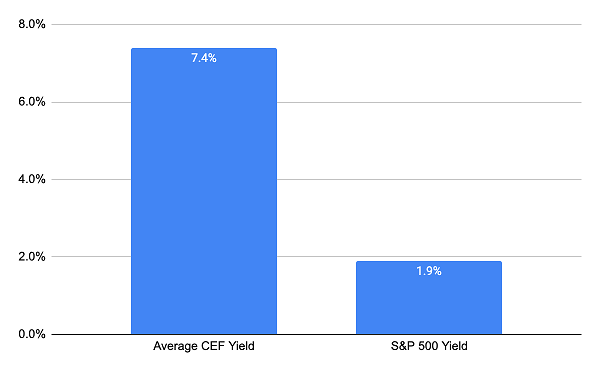

A Massive Income Boost

Source: CEF Insider

As you can see above, the average CEF yields 7.4% today, nearly four times more than the S&P 500’s average payout. Plus, CEFs are diversified across many different asset classes, including municipal bonds, corporate bonds and stocks in various sectors and countries, so you can build a portfolio of several different funds and get a diverse mix of assets while still getting a retirement-level income stream.

And we can do better than 7.4%. With many high-quality CEFs paying more than that, we can boost our dividends up to over 9% without breaking a sweat.

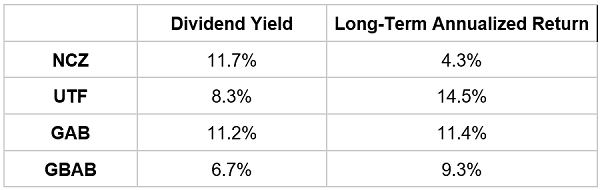

A Diversified 4-CEF Portfolio Yielding 9.5%

Take, for instance, this 4-fund portfolio: the AllianzGI Convertible & Income Fund (NCZ) for corporate bonds, the Duff & Phelps Utility and Infrastructure Fund (DPW), for utilities, the Gabelli Equity Trust (GAB), for stocks and the Guggenheim Taxable Municipal Managed Duration Trust (GBAB), for municipal bonds.

Combined, that gets us a portfolio with a 9.5% dividend yield and an annualized return of 9.9% per year.

High Income, Steady Returns

So, with just these four funds, we’ve created a high-yield CEF portfolio that can get us into retirement with $50,000 in annual income on just a $527K investment.

And these aren’t even the best CEFs out there! There are plenty of others you can combine into a diversified portfolio that pays a massive yield. This is one reason why these little-known funds are the income investor’s short cut to a worry-free retirement.

Bankroll Your (Wealthy) Retirement With My 4 Top High-Yield CEFs

I just released my top 4 CEFs for your retirement portfolio—and on the surface, they look a lot like the 4 I just showed you here.

For one, they’re diversified across the economy, giving you instant exposure to retirement-friendly utilities, corporate bonds and blue-chip US stocks.

High dividends? You bet. These 4 cash-rich picks throw off a rich 9.4% yield now.

But here’s where they really stand out: their discounts are so massive I’m calling for 20%+ price upside. Think about that for a moment: invest your $527K in these four and, in just 12 months’ time, you could be looking at $105,400 in price gains and another $49,538 in dividend payouts!

These 4 reliable CEFs are the secret to a well-funded retirement, especially in the age of COVID-19. Don’t miss out. Click here to get instant access to these 4 funds’ names, tickers, dividend histories and every bit of research I have on them.

Recent Comments