There are plenty of stocks out there, right now, with payouts growing fast—heck, some of them give shareholders a “raise” every three months.

You won’t find these “Dividend Accelerators” among the big names of the Dow.

A number of them are real estate investment trusts (REITs)—“landlords” of everything from apartments to warehouses. And they’re not just dividend-growth machines; most throw off higher current yields than the typical S&P stock, too.

And I mean much higher: right now, the REIT benchmark Vanguard Real Estate ETF (VNQ) yields 4.5% as I write. The typical S&P 500 name? A sorry 1.5%.

You can thank the federal government for that: it gives REITs a pass on corporate taxes as long as they pay 90% of their income as dividends. The resulting savings—and the fact that this hoard must be passed to us—drive those big dividends, and often lightning-quick dividend growth, too.

So if you like a fat yield and a dividend that soars every year (and sometimes quarterly), REIT-land is the place for you.

And there’s more. Look, I know we’ve talked about the “Dividend Magnet” again and again here on Contrarian Outlook. But there’s a good reason why: a rising dividend is the No. 1 driver of share prices. Take a look at this:

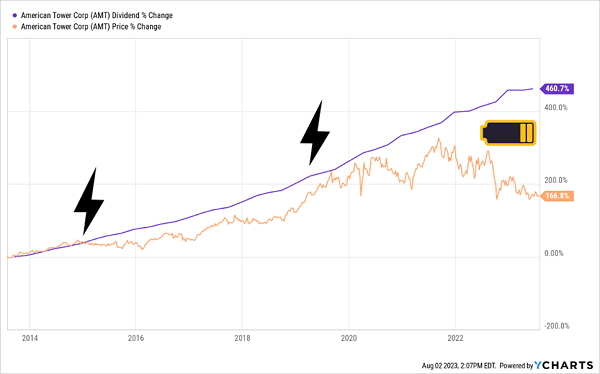

American Tower: Quarterly Raises Power a Strong “Dividend Magnet”

That’s the share price of cell-tower REIT American Tower (AMT) over the last decade. You can see the smooth orange line of monthly payout hikes driving the share price higher—until the payout levels off at the right side (more on that in a moment).

That tight correlation is why AMT was one of our first picks after we launched my Hidden Yields dividend-growth advisory. We bought in November 2018 and rode this helium-powered payout to a 57% total return by the time we sold in March ’22.

Why on earth would you sell a stock like that? For one, higher long-term interest rates could be an issue for AMT (and many other REITs) if they remain sticky. Moreover, its long-term debt jumped after it acquired data-center REIT CoreSite at the end of 2021, a purchase we were concerned it overpaid for.

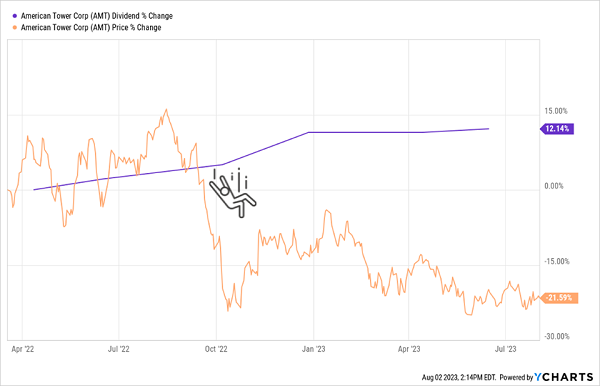

By making our move last March, we got out before that became an issue. And sure enough, the dividend trend shifted late last year, when AMT’s dividend, which had been rising quarterly, stalled.

End result: even though AMT’s payout is still up 12% from our sell date in March ’22, the company’s plunging stock price snatched that back and more.

Shifting With the “Dividend Winds” Saved Us From a Storm

It’s a good example of why dividend trends are the key to banking long-term gains (and avoiding losses) in stock investing.

So where does that put us today?

We’re still looking toward REITs—particularly industrial REITs—for high, fast-growing payouts, as stabilizing interest rates and a still-strong economy make their borrowing costs more predictable and let them keep raising the rent. The kicker is the onshoring trend, as US manufacturers pull out of China, Russia and other economic quagmires and bring them home.

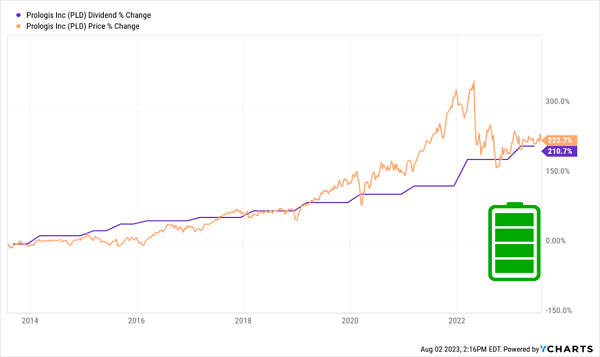

The biggest of the warehouse-owning bunch is Prologis (PLD), which has a staggering 1.2 billion square feet of manufacturing and warehouse space across the US.

To be sure, PLD doesn’t get our hearts racing on the current-yield front, with just a 2.8% payout. But it more than makes up for that with a payout that’s not only growing every year but accelerating.

Check out the two outsized payout hikes on the right side of this chart, plus the near point-for-point rise in the share price, along with the payout, in the last 10 years:

PLD’s Dividend Magnet Keeps Getting Stronger

Prologis’ secret weapon is its “fortress” balance sheet. Right now it has just $28 billion of long-term debt, which amounts to 25% of its market cap and 30% of assets.

That kind of financial strength is rare among REITs. What’s more, PLD has borrowed cheaply: it pays a weighted average interest rate of just 2.9%, with a weighted average term of 9.7 years. And it has no major debt maturing until 2026.

Which brings us back to onshoring, which is keeping PLD’s warehouses 97.5% occupied as of the end of the second quarter. And the REIT’s steady rent hikes, thanks to a lack of warehouse space in the US, are expected to boost cash flow by about 8% this year.

All of this makes the stock’s pullback in the last 15 months, which it has come nowhere close to recovering from, an extra-long buying opportunity. But that opportunity will likely end—or at least be quite a bit less attractive—as the dividend hikes continue.

These 5 Payers Will Be the Next 5 “Dividend Magnet” Winners (Buy Now!)

I love to talk about the Dividend Magnet because it is, quite simply, the best predictor of future stock-price gains that I’ve ever seen.

We just saw it in action with Prologis. And we’ve used it in my Hidden Yields service to score returns of 61% , 112% and even 148%! All by purchasing stocks you’ve likely heard of: cash-rich companies literally hiding in plain sight.

Now, with the rebound kicking in and inflation on the wane, is a terrific time to put this powerful strategy to work. To make it simple, I’ve dropped my top 5 Dividend Magnet picks—those with the fastest-growing payouts primed to yank their stocks higher—into a new Special Report I want to share with you now.

Recent Comments