These 5.7% and 8.9% dividend payers are ready to rally.

Whether they pop this year or next, we shall see. It’s a matter of when rather than if—which is what we gladly sign up for as income investors.

The broader stock market appears to be on a near-term sugar high. Crypto is going (a bit) crazy and meme stocks (of all things) are back. Count us careful contrarians cautious!

We instead turn our attention to natural gas—a market that has already corrected.

Remember when “natty” prices were supposed to go to the moon this winter? We feared that Europe, without Russian gas imports, would be in for a long cold season.

Fortunately, the heat stayed on. Here in the US, heating bills are even trending cheaper!

Natural gas producers responded to high prices and increased supply. Plus, Mother Nature cut Europe a break with a mild winter. As a result, we have a market that is oversupplied.

As a result, natural gas prices have plummeted. They are down 75% from their peak last year. Seventy-five percent!

This drop deserves our attention because just as the “cure” for high prices was high prices, the same goes for low prices. They’ll only stay in the basement for so long while producers begin to cut production.

Natural gas industry leader EQT Corp (EQT) is already looking ahead to the next imbalance. On a conference call last week, CFO David Khani explained how these low prices will dent supply while boosting demand:

“It’s basically sending a signal to cut production because pricing is forcing your activity off-line. And it’s also going to send demand up.”

Today, natural gas fetches just $2.35 per million BTUs, near a multi-decade low for prices. EQT sits prettier than most, with a cash flow breakeven price of $1.65 per million BTUs in 2023 (40% below the industry average).

EQT yields a modest 1.9% today. For contrarians in search of higher current yield, we turn to The Williams Companies (WMB) and its 5.7% dividend.

WMB moves energy (mostly natural gas) from here to there through its network of pipelines. It’s the toll booth we income investors like to own, with its collections adding up to a secure 5.7% dividend.

The company’s tolls flow directly into investors’ pockets because the firm has already built out its infrastructure. Yes, management still invests some money in growth projects, but most of its cash flows are ours in the form of a regular (and growing!) dividend.

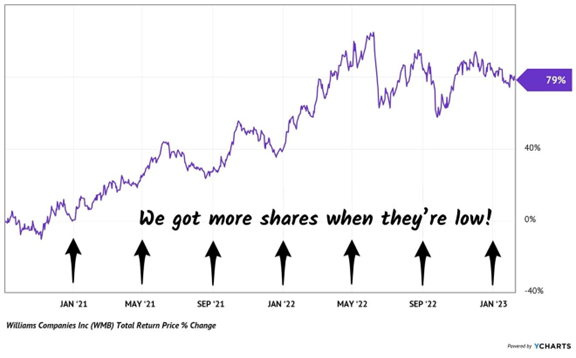

My Contrarian Income Report subscribers are sitting on 79% total returns (including dividends) since we added WMB to our portfolio in September 2020. This is a great stock to dollar-cost average (DCA) because it does tend to sway in the constant breeze of natural gas prices.

Buying WMB methodically (say every four months) is a great way to “time” this stock. By putting set amounts of cash to work, we can easily acquire more shares when prices are low and fewer when they are dear:

WMB is Built for a DCA Strategy

Didn’t DCA when we discussed it? Or buy at all? Here’s a golden second chance to scoop WMB for about as cheap as it gets.

While we’re in the bargain bin, let’s touch on Kayne Anderson Energy Infrastructure Fund (KYN), which pays a generous 8.9% today. It owns a collection of master limited partnership (MLP) stocks as well as other energy blue chips. (No K-1 worries here. KYN gets around this by issuing you one neat 1099—much cleaner. Anyone with a taxable account is used to a 1099 for dividends already!)

The Williams Companies (WMB) makes up 9% of KYN. This fund is a way to buy WMB and other energy toll bridges for just 87 cents on the dollar.

KYN should be trading closer to its net asset value. Heck, the fund traded at a premium as recently as 2018. Energy was in a bear market then. Now, it’s making a multi-year run higher.

But when there is fear in the energy sector, we can buy KYN for less than the value of the stocks it holds. Today, its portfolio is selling at a 13% discount to its NAV. This is about as cheap as we’ll ever see it.

My only knock on KYN is that it doesn’t pay its dividends monthly!

And who wants to wait 90 days to get paid?

Which is why I prefer these 7%+ monthly payers right now.

Recent Comments