They’re here again: more articles warning us of the “dangers” of municipal bonds. Don’t take the bait, because these wrongheaded articles will steer you away from some of the safest (and highest) dividends out there.

One claim you’ll read in many of these pieces is that states are losing tax revenue, which could mean they’re gong to default on their debt or go bankrupt. In reality, municipal-bond bankruptcies are really rare.

And I mean really rare: since 1970, the municipal-bond default rate has been 0.0043%, according to Moody’s Investor Services. To put that in perspective, the CDC says your chance of getting hit by lightning is 0.0002%.

So you may be more likely to buy a muni that defaults than be hit by lightning—but not by a lot.

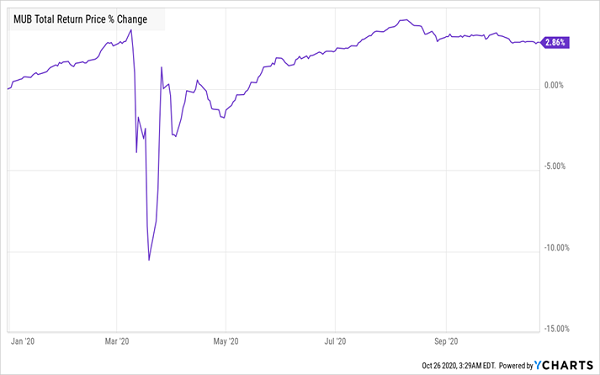

Still, financial advisors are warning clients of this risk, even though the Federal Reserve has repeatedly said it will support the municipal-bond market throughout the pandemic. That’s why muni bonds are actually up for the year:

Muni Bond Fears? Not in This Market!

That 2.9% return isn’t far behind what the S&P 500 has returned year to date, which is a solid result for a low-volatility asset class like munis.

Another reason for muni bonds’ popularity? Low interest rates. Again, the Federal Reserve has said that we will have near-zero interest rates for the foreseeable future, so investors who want yield and safety have been moving from U.S. Treasuries to munis.

And there’s one more factor boosting munis’ appeal right now, too: their dividends are tax-free for most Americans.

That’s a huge advantage. Because most folks know they have to pay taxes on dividend income from stocks and interest payments from Treasuries. But many people still don’t realize that they likely won’t have to pay tax on the interest they get from munis, or from dividends they get from funds that invest in muni bonds. That means the actual yield on munis is worth a lot more than you’d first assume.

Let’s take the benchmark iShares National Muni Bond ETF (MUB) as an example. MUB yields 2.3% now. If you’re an individual earning $150,000 per year, that 2.3% is the same as a taxable 3% dividend. That’s more than you’d get from Johnson & Johnson (JNJ) and its 2.7% yield, or Procter & Gamble (PG), which pays just 2.2%.

Plus, MUB is diversified across hundreds of bonds, so you’re not concentrating on just one company like you would with Johnson & Johnson, Procter & Gamble or another blue chip stock. And you’re getting a higher yield at the same time!

And we can do much better than 2.3%.

This 5.3% Dividend Could Be Worth 8.4% to You

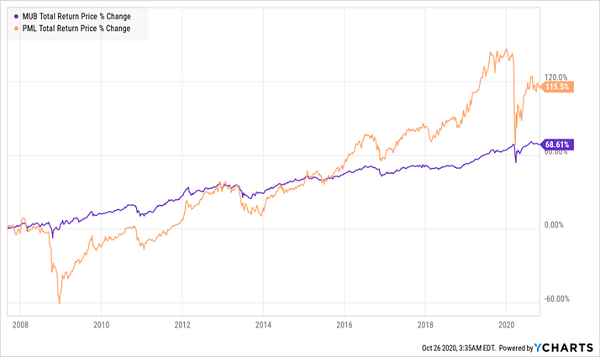

Instead of MUB, you can buy a muni-bond closed-end fund (CEF) like the PIMCO Municipal Income Fund II (PML), which yields 5.3%, or over double what MUB pays. And PML has vastly outperformed MUB for years.

PML Crushes the Index

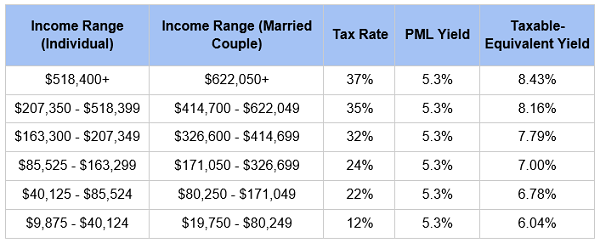

And when we compare PML to taxable-income options like blue chip dividend-payers or utility stocks, we can see that its yield is far superior, especially for higher-income earners. Look at how much you’d need to get from a taxable income stream to meet PML’s tax-exempt dividend:

In fact, even for the lowest income bracket, you’d need to get 6% yield on a taxable income stream to meet PML’s dividends, and not even junk bonds pay that! If you bought a high-yield-bond index fund like the SPDR Bloomberg Barclays High Yield Bond ETF (JNK), you’d get just 5.7% before taxes. After Uncle Sam gets his cut, you’d get less than PML would give you, even though PML invests in a much less risky bundle of assets.

Despite its safety and higher dividend, PML has still surpassed JNK’s return for as far back as the two funds have been around:

PML Crushes the Riskier Alternative

It’s pretty obvious that muni-bond CEFs are a great option to get a high tax-free income stream and superior performance. And PML isn’t even the best muni-bond CEF out there.

Yours Now: 4 Incredible Funds That Crush PML, Pay You Up to 9.4%

A 5.3% dividend is a lifesaver these days, of course. But even with its tax advantages, PML can’t quite match the high, safe cash stream you get from the 4 high-paying CEFs I’ll show you here.

These 4 stout income plays pay you 8.1%, on average—and that’s just the average! You’ll find monster payouts up to 9.4% among this bunch.

Better still, all 4 of these funds are trading at big discounts now. Here’s what that means in an uncertain time like the one we’re facing this autumn:

- If the market falls from here, these 4 funds should outperform: after all, it’s hard for a fund that’s already ridiculously cheap to get a whole lot cheaper!

- If the market regains its footing, these funds are primed to gap higher—and fast!

Either way, we’ll continue to collect our safe (and massive) payouts (up to 9.4%!).

Don’t miss your chance to drastically increase your income stream and set yourself up for massive price gains as the rebound kicks in. Click here for full details on these 4 stout high-income plays: names, tickers, buy-under prices, dividend histories and my complete analysis.

Recent Comments