I have no idea why “income” investors mess around with dividend reinvestment plans (DRIPs). Most don’t yield enough to matter.

If the goal is to retire on dividends, why not “automatically” bag a 10%+ income stream and 100%+ upside?

Better yet, this outsized cash flow drops into your account—and grows—every single month!

It takes almost no work. (Just one small, but potent step, which I’ll show you shortly.)

Before we get to that, let’s look at just how easy it is to use this proven strategy to double—and even triple—the cash stream your portfolio is throwing off today.

This simple system looks like a garden-variety DRIP, but it has one simple “hack” that amps up our dividend and sets us up for fast 100% upside, too.

Making DRIPs Obsolete

The humble DRIP is a no-brainer for most folks. Offered by most brokerages, these plans automatically reinvest your dividends into stock of the company that paid them. This adds to your share count and bulks up your income stream.

Sounds great so far, right? The best part is that you typically pay zero brokerage commissions on these purchases.

Problem is, most DRIPs don’t pay enough today. For example, if the dividends are reinvested in the S&P 500, the index pays barely more than 1% today. We could lose that in an hour of volatile trading!

Even blue-chip dividend funds don’t pay more than 2% or 3%. Not even close to cash flow needed to retire on.

This is where my strategy comes in. We’re going to “unplug” our dividends from the stocks that paid them and “redirect” this cash into a group of stout dividend payers yielding 7%, on average.

The best part?

These sturdy income plays throw off a dead obvious signal when it’s time to buy or sell! All we do is wait for that signal to appear, then buy—and keep piling in our dividend cash as these powerful income plays roll higher.

That makes DRIPs obsolete!

Here’s the best part: if you build an entire portfolio based on the steady 7%+ payers I’ll show you in a minute, you could easily generate $42,000 a year in income on a $600K nest egg—nearly four times more income than an investor who sticks with the S&P 500.

I know what you’re thinking: “Brett, how can a payout that high possibly be safe?”

Let me put your mind at ease, because every month, I personally run each one through a rigorous “dividend safety check,” starting with three things that are absolutely critical:

- Rising free cash flow (FCF)—unlike net income, which is an accounting measure that can be manipulated, FCF is a snapshot of how much cash a company is making once it’s paid the cost of maintaining and growing its business;

- A payout ratio of 50% or less. The payout ratio is the percentage of FCF that went out the door as dividends in the last 12 months. Real estate investment trusts (REITs) use a different measure called funds from operations (FFO) and can handle higher payout ratios, sometimes up to 90%;

- A healthy balance sheet, with ample cash on hand and reasonable debt, equal to, say, 50% or a stock’s market cap (or the value of all outstanding shares) or less.

How have we done?

Our subscribers have bagged predictable 10.3% annualized returns since our launch in August 2015. Best of all, most of that steady gain was in cash, thanks to the portfolio’s outsized dividend yield.

Not Your Parents’ Dividend Reinvestment

And as I mentioned above, this “retire on dividends” portfolio is perfect for dividend reinvestment because we receive big payouts every single month.

To show you what I mean, consider closed-end funds (CEFs), an overlooked corner of the market where dividends of 7% and up—often paid monthly—are common. We hold nine CEFs in our Contrarian Income Report portfolio, mainly larger issues with market caps of $1 billion or higher.

We don’t have to get into the weeds here, but CEFs give off a crystal-clear signal that a big price rise is coming. You’ll find it in the discount to NAV, which is the percentage by which the fund’s market price trails the market value of all the assets in its portfolio (known as the net asset value, or NAV).

This number is easy to spot and available on most any fund screener.

This makes our plan simple: wait for the discount to sink below its average level and make our move. Then we’ll keep rolling our dividend cash into that fund until its discount reverts to “normal.”

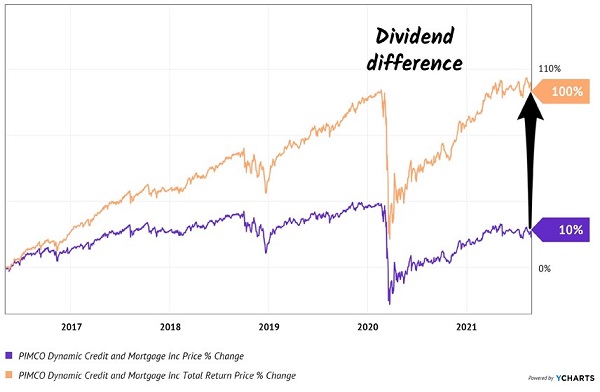

How My 1-Step “Buy Signal” Drove a Fast 100% Win

Discount-to-NAV gave us the high sign when we bought the PIMCO Dynamic Credit and Mortgage Fund (PCI) back in May 2016.

Fund manager Dan Ivascyn, a superstar in the fixed-income world, taps PCI’s portfolio of government bonds (both US and emerging market), mortgage-backed securities and high-yield corporate bonds to generate the fund’s mega-yield, paid monthly. It was a sweet 8.7% yield when we purchased.

Not only did we collect PCI’s generous payout, but we also enjoyed a 10% price increase over the years. Thanks to this rising tide and big “dividend difference,” we doubled our money in a safe bond fund!

PCI: A Dividend Double

In fewer than six years we were able to collect 70% of our original purchase price in dividends. Plus, the fund gained value while it was paying us! It was like an annuity, but better. It paid more, and our capital kept growing.

Who needs a vanilla DRIP when we have funds like PCI?

Our PIMCO Dynamic Credit and Mortgage Fund (PCI) has since merged into sister fund PIMCO Dynamic Income Fund (PDI).

While we’ll miss standalone PCI, we should be optimistic about its future, because PDI boasts the same great PIMCO management team. Plus, it pays 10.5%—tough to argue with in this sub-2% world!

Yours Now: My Next 7%+ (Monthly) Income Buys

Before you run out and buy PDI today, please note that it is trading at a premium to its NAV. As a true contrarian income investor, I always demand a discount from my CEFs.

Take a no-risk trial to Contrarian Income Report—full details on that and my complete monthly-dividend strategy here—and I’ll explain why.

Meantime, if you’re looking for some stout monthly high yielders to buy NOW, fear not! I’ve got you covered there, too.

Those would be the stocks, high-yield REITs and CEFs in my powerful “7% Monthly Payer Portfolio.” With just $500K invested, this dynamic collection of investments will hand you a rock-solid $35,000-a-year income stream. That’s easily enough for most folks to retire on.

The best part is you won’t have to go back to “lumpy” quarterly payouts to do it. Thanks to this breakthrough portfolio’s reliable monthly dividends, you can look forward to the steady drip of nearly $3,000 in income, month in and month out, give or take a couple hundred bucks!

Full details on these stout income plays are waiting for you right here. You’ll discover:

- A well-hedged 8.1% payer in one of the most in-demand sectors right now,

- The brainchild of one of the top fund managers on the planet that’s throwing off an amazing 7.8% yield.

- And a rock-steady 6.3% dividend whose managers own significant stakes. We love to see this in an investment because it aligns management’s interests with our own.

Don’t miss your chance to start tapping this retirement-changing dividend stream while you can still get in at a bargain. Click here to get full details on every stock in my “7% Monthly Dividend Portfolio”: names, ticker, symbols, buy-under prices—everything you need to know to buy with confidence.

Recent Comments