Bill Gross is one of the great characters in the investment world: flamboyant, bold—and generally disliked by those who worked for him.

But his PIMCO Total Return Fund saw over 9% annualized returns in its first decade, despite being a supposedly “boring” bond fund.

Those gains made Gross one of the most powerful people on Wall Street—so much so that during the subprime mortgage crisis of 2007 to 2009, the government called on PIMCO to help take care of the toxic assets that had sparked the worst recession in a century.

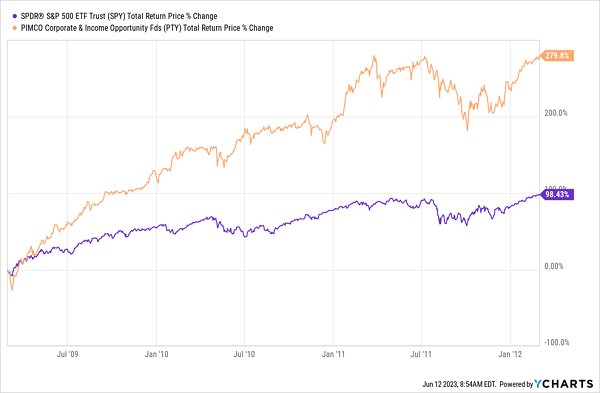

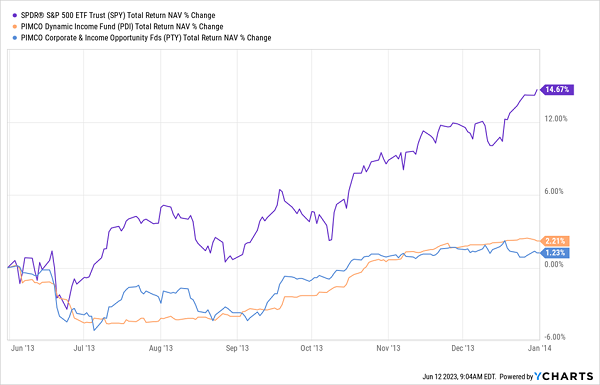

PIMCO’s Contrarian Subprime Play Paid Off Big

Gross, for his part, did help, thereby helping investors earn even more money. PIMCO used its closed-end funds (CEFs), including the PIMCO Corporate & Income Opportunity Fund (PTY)—shown in orange above—to buy these assets cheap. That resulted in the fund crushing the S&P 500 (in purple), an unusual feat for a bond fund.

(This, by the way, was when I got into CEFs, and seeing these profits combined with these funds’ income—PTY yielded around 10% then; it yields 10.9% now—made me a lifelong fan of these assets.)

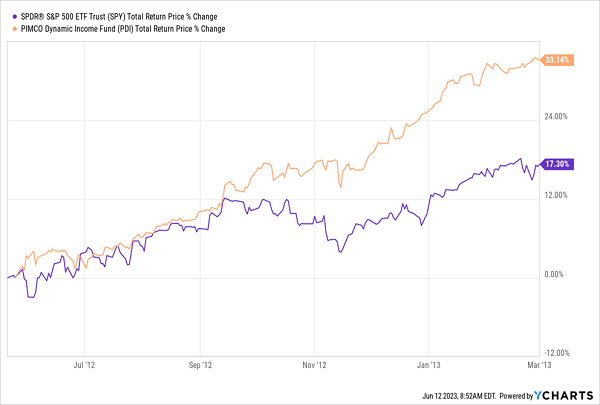

Gross saw the power of CEFs and launched new ones, like the PIMCO Dynamic Income Fund (PDI), which yields 14% today and has actually raised payouts by 25% since its 2012 IPO. It issued many special dividends, too, which helped PDI’s early total returns surge ahead of the S&P 500:

PDI Crushes Stocks

At the time, a lot of the credit went to Gross, which is why PIMCO funds pulled back when he left the company in 2014. However, the first five years after Gross’s departure saw PIMCO’s CEFs return to form.

The reason for PIMCO funds’ strong performance had more to do with market timing and the company’s approach to bonds. PIMCO, for example, is one of the only firms to use complex bond derivatives to lower risk (through things like hedging) and boost returns. And PIMCO’s CEF track record proved those tools work well in the long run. That said, the company’s funds do tend to lag for shorter periods—but there’s a pattern to those lags that we can profit from.

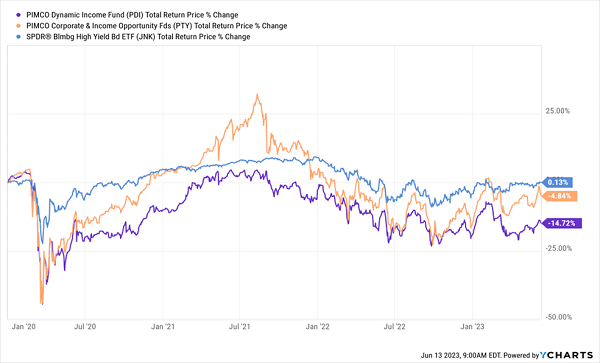

PIMCO Funds Lose Their Shine?

As you can see above, PDI (in purple) and PTY (in blue) have trailed the corporate-bond benchmark SPDR Bloomberg High Yield Bond ETF (JNK) from the start of the pandemic to now.

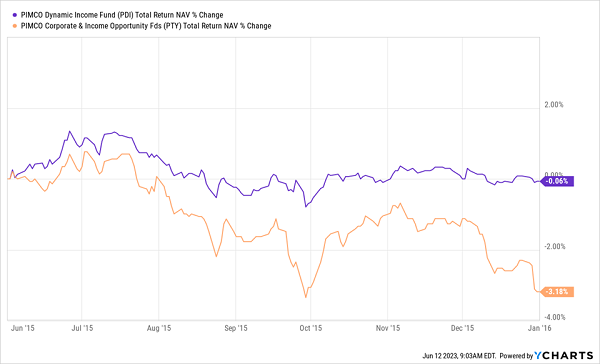

Could it be that PIMCO’s edge is gone? While that does sound logical, the reality is a bit different, as this chart showing the net asset value (NAV, or underlying portfolio performance) of PDI (in purple) and PTY (in orange) shows.

Fed Uncertainty Weighs on PIMCO in the Short Run

Back in late 2015, the Federal Reserve started to pivot from low rates to raising rates, and PIMCO funds underperformed as a result. This was after Gross’ watch ended, but something similar happened during his time at the company in late 2014.

2014 Fed Pivot Also Weighed on PIMCO CEFs

At that time, the stock market kept making all-time highs, thanks to the Fed’s loose monetary policy (which was pivoting from a tighter stance), and PIMCO’s CEFs also struggled. When the Fed pivoted again in 2022—wait for it: PIMCO’s funds also lagged.

Fed Hikes, PIMCO Falls

Note that the PIMCO funds’ fall in 2022 was dramatic, as was the decline in pretty much everything as fear set in. But the same pattern holds: PIMCO funds didn’t do well at a time of market uncertainty over the Fed’s change in policy.

Which brings us to today, with the Fed’s policy changing again, this time toward a pause in rate hikes. That makes both funds buys now—which might sound strange, as both look far from cheap, trading at premiums to NAV.

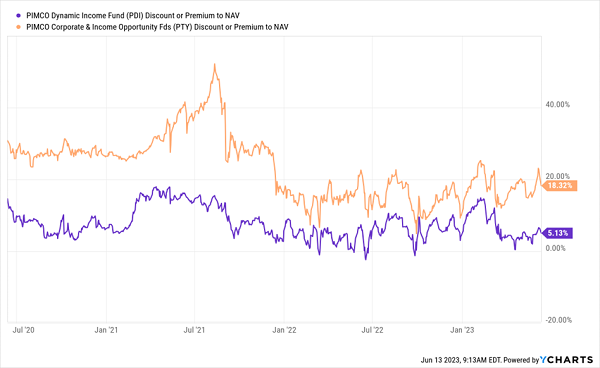

But premiums are common at PIMCO funds, due to the company’s strong reputation and the top talent it pulls in. With PIMCO funds, then, the key is to look at historical trends in the premium. And we can see that both PTY and PDI are good values today, on a historical basis:

The “Hidden” Discounts on PDI and PTY

Moreover, recent moves in the bond market mean corporate bonds are now yielding 5.8% on average, with 7%+ yielders easy to find. So PIMCO can maintain big payouts for years just by buying and holding bonds.

And that’s just a base case: if PIMCO continues with the strategies it’s used in the past—as it undoubtedly will—it’ll likely deliver a big yield that grows, with strong gains and special payouts along the way.

These 5 “Lifetime Profit” CEFs Crush Stocks (and Yield 10.1%)

Here’s something most people don’t know about CEFs: the most established funds of the bunch almost never lose money—and they pay us dividends 6 TIMES the typical S&P 500 payout!

Here’s what the numbers say: of the 343 CEFs that are a decade old or older, only 34 have lost money over the last 10 years, for a 90% win rate!

It gets better: of the 34 that did lose money, the majority were energy funds. Dump those laggards and CEFs’ “win rate” jumps to an incredible 99%!

I’ve sifted through the entire CEF universe to come up with the best funds to recommend in my CEF Insider service. And I’ve taken my top buys from our portfolio and dropped them into an exclusive Special Report I want to share with you today.

These 5 picks yield an incredible 10.1% between them, and I’m calling for 20%+ price upside from each one in the next year.

Recent Comments