As we return Mariah Carey to the ocean depths for another year, we turn our attention to our next seasonal siren—double-digit dividend stocks.

They are, after all, the perfect way to retire on dividends, right? Put $500,000 in a portfolio of 10% payers and we’re looking at $50,000 in annual dividend income. Plus we get to keep our principal.

Right?

Not always. Most double-digit divvies are “cheap for a reason.” These are dogs dressed up as dividend payers. But the payouts are often in danger. Which means price stability is equally dicey. Which is why we often say no thanks to these mega-headline yields.

That said, we’re not going to say no simply because a stock has a big dividend. No stone unturned here at Contrarian Outlook! Some of our favorite historical plays have been underappreciated 10%+ yields.

It’s rare. But it happens.

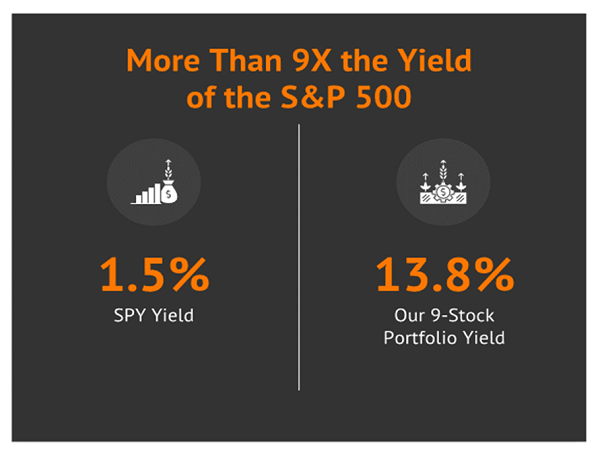

Today we’ll consider a nine-pack of dividend stocks that averages a terrific 13.8% annual yield. If secure, these payouts will fund a heck of a retirement party.

Let’s look into them. We’ll start with energy dividends. The Federal Reserve’s recent pivot could be very bullish for oil prices. So much so that the Fed may regret its latest Wall Street pillow talk as the year progresses. If the economy accelerates and inflation reignites, crude oil prices could boom.

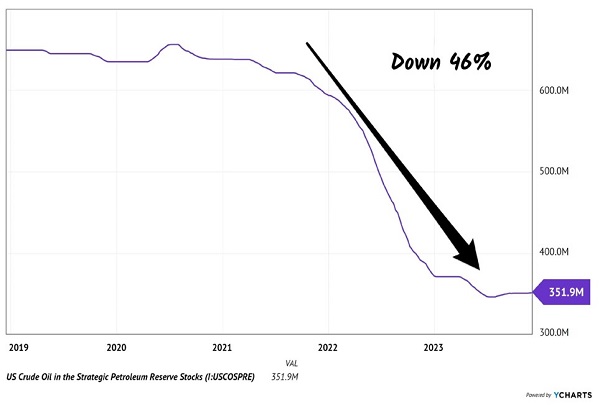

If that happens, the “rainy day” stockpile of oil, the US called the Strategic Petroleum Reserve (SPR), won’t be available for any future inflation rescue. We’ve already burned through 46% of these barrels in recent years (yikes). America began cooking through supply as fast as your editor tosses logs into his backyard Solo Stove:

SPR Now Light on the Reserve Part

Since 2021, we’ve swallowed 300+ million barrels of oil. The “emergency” was inflation. I suppose it worked, but our rainy-day Texas Tea fund is down by nearly half.

If we saved for two rainy days, we have one left! In theory, the government is supposed to replace the barrels they’ve burned. And now, with oil cheap, our elected officials can buy low.

In practice, I’d be shocked if that happened in an election year. Uncle Sam as a buyer drives up the price. No bueno for voters.

Still, the SPR is more or less tapped out for the time being. Uncle Sam can’t keep withdrawing. This is supposed to be an emergency fund.

With SPR supply coming off the market, crude has a catalyst for higher prices. Supply is down, so… (fill in the Econ 101 blanks!)

…bullish for oil! Meanwhile the black goo is 20% off its recent highs and it’s one of the most despised assets on the planet because, well, it’s down. (Talk about circular reasoning!)

We contrarians like low. That’s where the money is made. Thanks to low prices, these four energy dividends are high:

- Equinor (EQNR, 11.2% yield): Equinor isn’t a first-to-mind name here in the U.S., but it’s a major European player—a Norwegian integrated petroleum giant that also deals in oil and gas commodities, as well as renewables.

- Berry Corp. (BRY, 13.3% yield): California-based Berry Corp. is an upstream E&P firm that’s primarily engaged in oil production, though it also has some natural gas operations.

- CVR Energy (CVI, 14.4% yield): is an oil and renewable fuels refiner and marketer that, via its CVR Partners LP (UAN), also has a nitrogen fertilizer arm.

- Petroleo Brasileiro, aka Petrobras (PBR, 18.2% yield): This state-owned Brazilian firm is one of the world’s largest oil and gas exploration and production firms.

Unfortunately, all four of these stocks offer extremely inconsistent dividends. Berry Corp. and Petrobras have variable payouts, while CVR and Equinor put special dividends to use to augment their regular dividend programs. That’s great times when business is good and their wallets are flush, but we certainly can’t plan our retirements around these inconsistent payouts. I view these stocks more as potential short-term trades than long-term buy and holds.

For those of you who prefer more kick than energy, let’s pass the five spice for some Chinese fintech. (I’ll give you a moment to ponder that leftover eggnog in your fridge.) LexinFintech Holdings (LX, 12.7% yield) or Lufax Holding (LU, 12.7% yield) are two ultra-high-yield stocks that are, to put it lightly, not for the feint of heart.

They’re both not only Chinese-based American Depositary Shares (ADSs), but they both operate within the financial technology industry. LexinFintech operates Fenqile.com, an online consumer finance platform (installment loans and online direct sales with installment payments) that also offers the Le Hua Card (credit services). Meanwhile, Lufax Holding offers secured, unsecured and consumer finance loans.

The Chinese government may say their consumer lending business is going OK. These two nosediving stock prices disagree:

Bad Times for Chinese Lenders

LU and LX offer high dividends—and almost nothing else. These payouts have next to no track record, and they’re semi-annual to boot, making them less than ideal for regular retirement expenses. In China, you have an extremely volatile economic situation to worry about. And in the case of Lufax, you have a stock that recently changed its ADS ratio (that had the effect of a 1-for-4 reverse stock split—and also recently received a warning from the NYSE about shares falling below the exchange’s continued listing standards.

On the Pacific Ocean in between, we have our shipping stocks. Also not for the feint of heart, but potential beneficiaries from a lovingly dovish Fed. If the global economy accelerates, shipping stocks are likely to benefit. Many dish big dividends.

Depending on the screener you use, you might actually see several dry bulk and other shipping names offering double-digit yields. But be careful—even the most powerful screeners have difficulty dealing with dividend data (which is why we developed our own Income Calendar tool).

In fact, of several shippers that showed up in my high-yield net, only one actually offers a double-digit dividend anymore—the rest have either drastically cut or even suspended payouts, and the screeners have just yet to catch up!

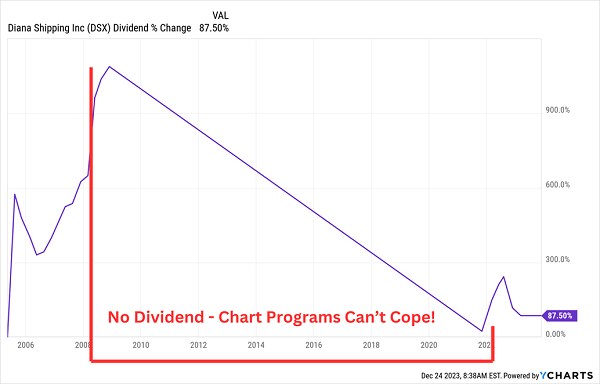

Diana Shipping (DSX, 19.9% yield) is the only “real deal” of the group. This shipping stock specializes in dry bulk vessels, boasting a fleet of 41 vessels ranging from Ultramaxes (60,000-69,999 deadweight tons, or dwt) to Capesizes (130,000-199,999 dwt). Diana celebrated a banner year in 2022, enjoying a 35% year-over-year surge in revenues and a more-than-doubling (+120%) of the bottom line. But it’s on pace for big declines in 2023, and the pros are expecting those declines to slow (but continue) in 2024.

That’s normal in the notoriously volatile shipping space, but you don’t want nauseating moves in profitability from your retirement holdings—especially if dividends are equally as volatile. While DSX’s dividend has held steady at 15 cents per share for a few quarters, that’s down from as much as 27.5 cents just a year ago.

More importantly, there’s the matter of a payout that disappeared from 2008 through 2021!

The Farthest Thing From an Income Guarantee!

We’ll wrap our discussion with the final two double-digit divvies in our grab bag. Vodafone Group (VOD, 11.1% yield) is a British multinational telecom company with operations in Europe and Africa—a bit scaled down from a couple years ago when it also operated in Asia and Oceania.

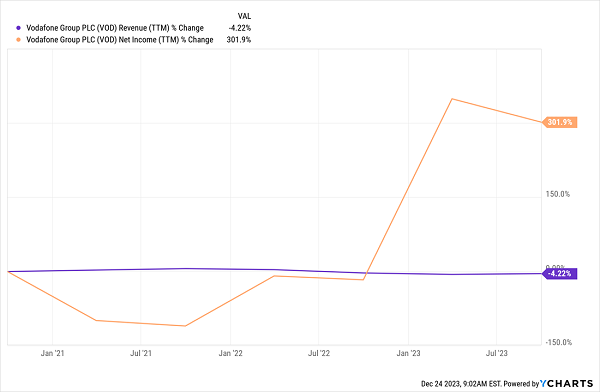

Vodafone has delivered something we expect out of telecommunications companies (extremely stable revenues) as well as something we don’t (explosive profit growth). Last year, VOD prioritized cost cuts, announcing a plan to achieve 1 billion euros in savings. That helped deliver a nearly 5x jump in profits in the year ended March 2023.

That’s More Like It!

But investors haven’t been swayed at all. Debt remains high, and CEO Margherita Della Valle, who was installed at the start of 2023, said “Our performance has not been good enough. To consistently deliver, Vodafone must change. We will simplify our organisation, cutting out complexity to regain our competitiveness.” I worry about the potential for cuts in the dividend—which has remained stagnant since 2020—and VOD price action implies that I’m not alone.

A dividend cut would certainly help VOD’s financial situation, but that’s one party you don’t want to be early to.

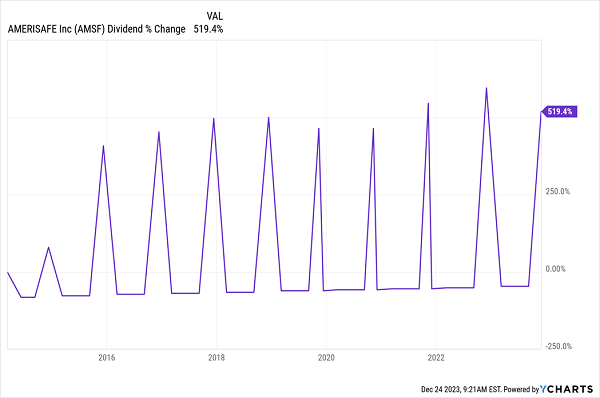

Amerisafe (AMSF, 10.3% yield) is an insurance stock, but one that’s quite different from the pack—it’s a specialty player that deals in workers’ compensation. The company operates in 27 states and deals in “high-hazard” industries such as construction and trucking.

AMSF uses special dividends in an extremely responsible way, from a fiscal management standpoint. It offers a modest quarterly dole that comes out to a yield of about 3%, then pays out (sometimes massive) specials as profits allow. For years, it had paid a fat $3.50 annual special dividend, and it bumped that up to $4 in 2021, then $4.31 in 2022, though it pulled back that payout a bit to $3.84 in 2023. The regular dividend, though, continues to head in the right direction.

Broadly Speaking, AMSF’s Dividend Trend Is Our Friend

In contrast, however, the business is shrinking. The top and bottom lines have contracted every year since 2019. And while AMSF is tracking for a slight rebound in 2023, the declines are expected to resume yet again in 2024.

Give Me 4 Minutes, I’ll 5X Your Retirement Income

Amerisafe is hardly in any dividend trouble—indeed, its special dividends protect its regular payout. But the big specials that make up most of AMSF’s super-sized yield could be difficult to fund at current levels, and the last thing we want in retirement is a declining annual income.

In fact, the last thing you want is to make any sacrifices when choosing your retirement holdings.

While it might sound greedy, we need to “have it all” when picking our retirement holdings.

Big yields? Yes.

Growth potential? Absolutely.

A bargain price? A must.

And while we’re at it, we need investments that can survive a few gut punches—whatever Jerome Powell, the economy, and presidential elections can throw their way.

If it sounds like too much to ask, believe me, it’s not. Because those are exactly the kind of investments you can find right now in my “Perfect Income” portfolio.

My “Perfect Income” portfolio attacks retirement investing from a different angle. Rather than trying to time the market and chase trends, we target high-yield holdings (roughly 5x the S&P!) that walk their own path, no matter what the Fed, Congress or the rest of the world throws their way.

So, what makes these dividends “perfect”? Well, they have to have a few things in common:

- They DO pay consistently, predictably and reliably.

- They DO survive—and even thrive—in market crashes.

- They DO deliver double-digit returns, with safe, secure investments.

- They DO require minimal management time—just a few minutes every month!

- They DON’T involve day trading, buying on margin or any other risky strategy.

- They DON’T involve gambling on penny stocks, Bitcoin or buying puts and calls.

Let me show you the stocks and funds you need to stabilize your retirement. But more importantly, let me teach you more about this incredible strategy itself and make you a better investor in the process!

Take control of your financial legacy today. Click here for my newly updated briefing on the Perfect Income Portfolio!

Recent Comments