Are the best things in life actually free? It depends how we handle the hidden costs.

Free coffee is good. At home, I drink one mega-cup per day. At fixed income conferences, I typically scale that “complimentary” consumption up to double-digits per day. (Hey, they’re just hotel cups.)

Free breakfast is usually better than just free caffeine. And open bar, of course, reigns supreme for your income strategist.

No doubt these freebies are baked into ticket costs, but I will gladly accept the bacon and beer challenge to get my money’s worth.

When readers write in to ask my thoughts on “risk free” yields on certain bonds, it’s time for us to talk. No bond is perfect and inflation insurance—like it or not—always comes with a hidden cost.

US Treasuries played the “risk free” role from 1980 to 2020 so well that investors in them began to take this income buffet for granted. Yields went down for 40 years, so bond prices (which move inversely to yields) went up. Anyone who bought Treasuries during this epic bond epoch got some price upside with their payouts.

But rates can only fall for so long. By the end of last year, they had hit their lower bound, at least for now.

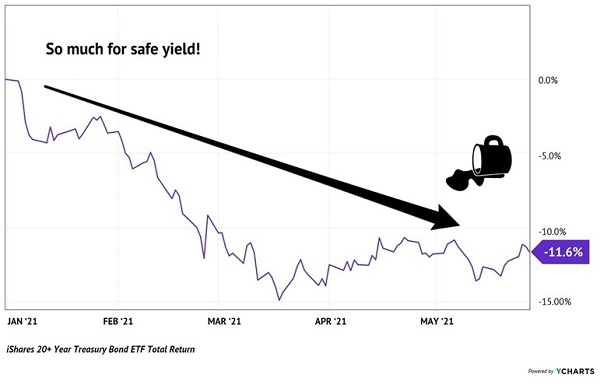

Bond bulls who recently bought the popular iShares 20+ Year Treasury Bond ETF (TLT) probably didn’t think their four-decade win streak would end at year 41. But TLT owners are down nearly 12% on the year, wondering why they risked so much on a pathetic 1%+ payer:

“Risk Free” Treasuries:

Going Down Like Free Conference Coffees

Treasury Inflation-Protected Securities (TIPS) are the “risk-free” choice for 2021. I’m hearing votes from many thoughtful readers, writing in with questions like:

What are Brett’s thoughts on conservative, inflation-protected investments like TIPS? There are some TIPS funds yielding 3.5% to 4% risk free.

There are those words— “risk free”—again! Like an open bar binge gone too far, they can get us into trouble if we are not careful.

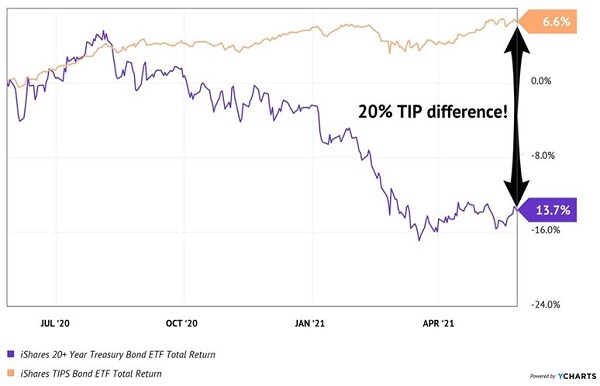

TIPS have certainly been better than Treasuries over the last twelve months. Let’s put the trendy iShares TIPS Bond ETF (TIP) up against its traditional sibling. We can see that TIP has certainly done its job—paid its yield, plus some price appreciation:

20% TIP (Differences) Appreciated

However, let’s not mistake a timely trade for an eternal truth. TIP (and similar funds) have the same loss potential as fixed-rate Treasuries. The trick to buying inflation-protected bonds is when inflation expectations, but not necessarily rates, are beginning to rise.

In other words, we should use them to buy the inflation rumor and sell the news.

That said, TIP itself yields just 1.3%. Typical lame ETF. As usual, we can double our inflation-protected dividends by considering closed-end funds (CEFs). The Western Asset Inflation-Linked Income Fund (WIA) is the CEF play here.

WIA yields 2.8%, plus it trades at a 6% discount to its net asset value (NAV). TIP, on the other hand, trades at par. So, we get a bigger yield with WIA plus we get to buy it for 94 cents on the dollar.

But aren’t these dividends still sounding a bit sad? It’s like finding out that Heineken is the import beer at the open bar. After all, if we’re playing higher rates, then let’s play them.

And we’ve been on the beat since the start of the year. In our kickoff column for 2021, you and I said that small banks were the place to be. In fact, we told the world they were our favorite dividend stocks for 2021.

The “spread” between the long and short end of the interest rate curve is ballooning to something from nothing. Bank profits directly benefit. It is a huge windfall because their borrowing costs (tied to short-term rates) are staying low while their lending profits (tied to long-term rates) pop.

We like small banks better than big banks because the smaller firms actually know their customers. And their balance sheets are much easier for us to read.

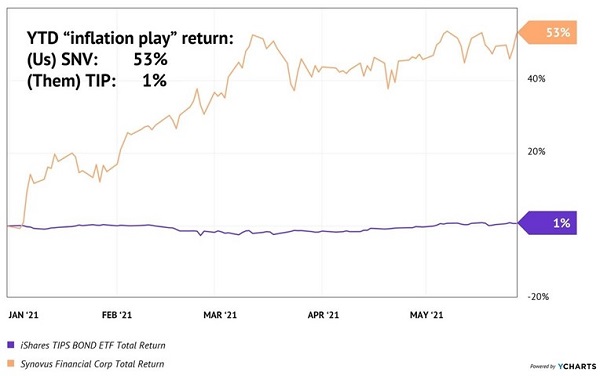

Synovus Financial (SNV), the stock we profiled in that column, has made the TIP ETF look childish. It’s up another 53% this year after a torrid close to 2020:

A Better Way to Play Inflation Expectations

I’ve been hearing from Contrarian Income Report subscribers who are up a cool 180% on our SNV position. They are concerned (well, relatively speaking) that SNV’s yield is now too low. Should profits be booked, and placed elsewhere?

To which, I will continue to paraphrase the Western philosopher Indiana Jones:

“Maybe. But not today.”

Our CIR portfolio is dedicated to 6%, 7% and 8%+ yields. When we bought SNV, it qualified with a sky-high 6.6% yield.

Now, that was not a risk-free purchase by any means. Other investors worried that SNV’s loan portfolio was toxic. We understood the concern but disagreed—and our contrarian view was richly rewarded.

A huge part of our success was letting this winner run. We could have sold SNV when its current yield dropped below 6%, or 5%, or 4%. Heck, the stock pays new money “just” 2.8% today!

But our original money still earns 6.6% (our “yield on cost,” which is what we care about), and we’re not going to argue with serious price appreciation. We bought right. Let’s not overthink it—just continue to sit tight.

TIPS might be overthinking it here. Sure, I can’t get in my car (with Sirius XM always turned to Bloomberg Radio) without hearing about inflation. It’s a popular idea at the moment. But so was crypto last month. And these digital coins are down 50% since then. We don’t let the emotion of the moment dictate our moves (unless it gives us bargain prices).

While the Synovus ship has largely sailed, I have my eye on 7 more “Fed-Fueled” stocks to buy immediately. These little-known dividend payers boast rock-steady 8% annual dividends, with much more room to grow.

Like Synovus, they are benefiting directly from Jay Powell’s printing press.

Unlike Synovus, these Fed-Fueled dividends have not doubled. At least not yet! Please let me share more information about them before these “printing press beneficiaries” really get rolling.

Recent Comments