Do you also believe that a recession is on the way?

Note that we’re not saying when. Maybe later 2023. Or 2024. For sure 2025.

We are good economists. Casting out predictions without set timelines!

At some point, of course, all of the rate hikes add up. The housing market slows because mortgages become more expensive. Commercial landlords feel the pinch because, well, nobody rents office space anymore!

One by one, industries slow down. Eventually, the much-anticipated recession arrives.

As contrarian investors, we don’t actually care about economic data. GDP. CPI. PPI. PMI.

Whatever. It’s all TMI.

We’re after dividends and growth, in this order. Today, we’ll highlight four stocks that are prepared to provide both. So that we may profit without apologies!

The secret to yield plus price upside? Payouts that pop. These “dividend magnets” pull their stock prices higher regardless of what the broader economy is doing. They are recession resistant.

Microsoft (MSFT) is a great example. The tech giant might not have a century-old dividend like Procter & Gamble (PG) or General Mills (GIS). But compared to most other tech names, its 17-year-old payout is practically ancient.

The Great Recession struck shortly after Microsoft initiated its first dividend, in 2006. On the way out of the financial crisis, Microsoft started getting aggressive with its payout—and shareholders enjoyed not just a doubler-plus in the dividend over the next five years, but a near-doubling in shares, too!

Microsoft With the “Double Doubler”

This synchronized dance between dividend growth and share-price growth is a phenomenon I like to call the “dividend magnet.” And it’s made up of three “prongs” that make dividend growth investing so successful over time:

- Growing Payouts = Growing Yields: If I buy a stock this year, my yield on my original cost basis improves every time that stock raises its dividend. For example: If I buy at $100 and a $1 dividend, my stock yields 1%. But if it doubles its dividend to $2, the yield on my stock also doubles, to 2%. Given enough time and dividend growth, even modest dividends can explode into high-single-digit or even double-digit payouts!

- Growing Payouts Beat Inflation: Inflation erodes the value of the dollar. Let’s say inflation runs at 4% for a year, but your dividend stays flat. That means your dividend effectively shrank by 4% in a year! And while inflation might be slowing down, we still want to make sure we’re well ahead of it!

- Growing Payouts Pull Share Prices Higher: On rare occasions, failing companies will grow their dividends, but they’ll usually be token raises that signal little financial flexibility. But big leaps and bounds in the dividend are a statement—and that statement is “our profits are growing so rapidly, we can afford to share a lot more cash with you!” When other investors see that, they want in on those profits, so they buy shares—driving your stock higher.

So if we want growing stocks, we want to start by looking at growing dividends. And today, I’ll show you a handful of companies that have been delivering breakneck dividend growth—as in, between 50% and 100%—and that typically announce dividend hikes during the third quarter, which we’ve just entered.

Host Hotels & Resorts (HST)

Dividend Yield: 3.6%

2022 Hike: 100%

Projected Q3 Dividend Announcement: Early August

Host Hotels & Resorts (HST) is not, as the name might suggest, a hotelier like Hilton (HLT) or Marriott (MAR). Instead, it’s a real estate investment trust (REIT) that specializes in hotel properties.

Specifically, Host’s property portfolio currently is composed of 77 hotels, representing nearly 42,000 rooms, in 20 top U.S. markets. And those hotels do include properties from Hilton and Marriott, as well as Hyatt (H) and other hotel chains.

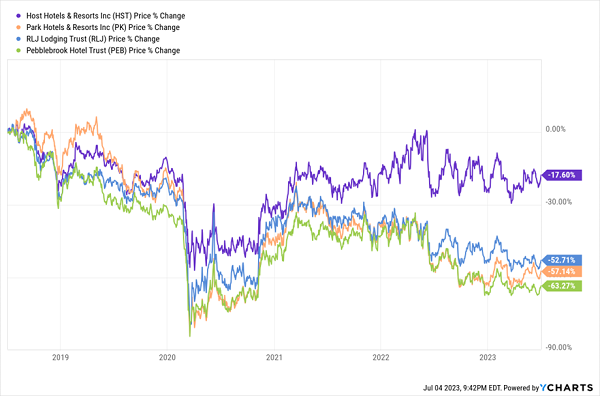

Host’s COVID story is much the same as other hotel REITs: Shares cratered as the pandemic temporarily gutted travel, then roared back to life as pent-up travel demand was unleashed. From there, investors have scratched their heads about what’s around the next corner—better REITs, such as Host, have merely stagnated, while lesser-quality REITs have hemorrhaged much of their post-COVID recovery gains.

Host: Hanging Tougher Than Other Hotel REITs, But It Needs a Spark

Host’s dividend growth over the past couple of years has been explosive, but with a big, fat asterisk attached. HST’s payout has quintupled, from 3 cents per share in 2022 to 15 cents currently. However, that followed a suspension of its 20-cent dividend in 2020, in the midst of COVID—the gains in the dividend since then have been Host simply trying to get itself back to square.

There’s hope in that. The REIT seems to be deliberately marching toward its old dividend total, with four increases in two years. To reach its pre-COVID dividend levels, it would need to tack on another 5 cents per share—another 33% from current levels. That could be done without much strain. Host is projecting adjusted funds from operations (AFFO) of $1.89 per share for all of 2023, and a 20-cent quarterly dividend would translate into an AFFO coverage ratio of just 42%. So keep your eye on Host in early August, when it’s slated to make its next dividend announcement—its next chance to raise the payout.

By the way, that payout ratio also would leave lots of room for further dividend increases, but don’t expect Host to get overly aggressive. After all, HST is just a couple years removed from a dividend suspension. Also, remember: A few years ago, I noted that Host relies on business travel—and shorter-term, business and group travel could struggle as corporate executives closely monitor America’s economic situation.

Ford (F)

Dividend Yield: 4.1%

2022 Hike: 50%

Projected Q3 Dividend Announcement: Late July

Speaking of recovering dividends, let’s take a look at Ford (F).

Ford needs little introduction, but let’s go over the basics. The automaker has been around for more than a century, and its flagship F-series pickup trucks have been America’s bestselling vehicle for roughly four decades. Indeed, bigger vehicles like trucks and SUVs have become Ford’s bread ‘n’ butter—it discontinued most of its passenger vehicles, like the Fiesta and Taurus, last year. And like most automakers, it’s building out its electric line. (Successfully, I might add. Two of last year’s top 10 bestselling EVs were Fords.)

Still, Ford hasn’t been without its issues. The pandemic also wreaked havoc on the automotive sector, claiming (temporarily) the dividends of both Ford and rival General Motors (GM).

The dividend has since returned to its pre-COVID 15 cents per share, and Ford also paid out a 65-cent special dividend in 2023—though that was funded by the windfall from selling most of its Rivian (RIVN) stake, so that’s no indication of future payout growth.

Higher earnings would be an indication, though those aren’t in the cards for now, either. Ford’s profits are projected to decline this year and next, largely on—you guessed it—worries about demand decline because of economic uncertainty.

Could Ford dig deeper into its own pockets to expand the dividend? Technically, maybe, but only a little. It’s already paying out 75% of current profits, and that ratio will only grow if its earnings shrink as projected.

I’ll still have my eye on Ford in late July, when it would be likely to announce any change to its dividend. Even a token increase would indicate a prioritization of the payout—and possibly spur investor optimism around shares.

Howmet Aerospace (HWM)

Dividend Yield: 0.33%

2022 Hike: 100%

Projected Q3 Dividend Announcement: Late September

Howmet Aerospace (HWM) makes advanced engineered products for the aerospace and transportation industries. It produces things like aero engine and industrial gas turbine components, aerospace fastening systems, forged wheels and more.

And before you wave away Howmet on the virtue of its small yield, consider this: Back in 2010, Broadcom (AVGO) kicked off its dividend program at 7 cents per share—at the time, that was good for a diminutive 1.4% yield on a share price of around $19.40. Fast-forward 13 years, and the company now pays $4.60 per share, which comes out to a wild 95% yield to shareholders who have hung on since then.

In short, sometimes, all a small yield needs is time.

Back in 2016, Alcoa (AA) split into two companies—Alcoa and Arconic (ARNC). Fast-forward four years, and Arconic then spun off its rolled products division, which became the current Arconic. What remained was Howmet Aerospace. In 2021, the company resumed dividend payments at 2 cents per share, then announced it would double the payout, to 4 cents, in September 2022.

Howmet Is On Its Own, Off to a Great Start

There’s good reason to think further dividend growth is on the horizon. Commercial and defense aerospace are two potent sources of potential future growth, and estimates reflect that: HWM is expected to grow earnings by 21% next year, and 17% annually over the next five years. Most of its supply-chain issues are in the rear-view. Debt is being paid off. And it currently pays a mere 10% of its earnings out as dividends. That’s a lot of reasons to keep Howmet on your horizon.

GeoPark (GPRK)

Dividend Yield: 5.3%

2022 Hike: 55%

Projected Q3 Dividend Announcement: Early August

GeoPark (GPRK) is a dividend growth story that has flown completely underneath the radar.

GeoPark is a Latin American oil-and-gas exploration-and-production company that boasts assets in Brazil, Colombia, Chile and Ecuador. Its prize asset is the Llanos 34 block—in its own words, “the largest oil discovery in over 20 years in Colombia.” Gross production has rocketed from zero to 75,000 barrels of oil per day (bopd) in less than a decade.

Dividends have exploded higher in a much shorter time period, from 2.06 cents per share in 2020 to 13 cents today—a wild 531% improvement in just three years, including a 58% jump since 2022 (two hikes: a 55% increase to 12.7 cents per share announced in August, and a minor uptick to 13 cents announced in March).

So, where might the dividend go from here?

Like a growing number of E&P firms, GeoPark has decided to tether its payouts to its financial results, rather than establishing a set dividend and hoping oil prices can sustain it forever. In GPRK’s case, the company plans on returning between 40% and 50% of free cash flow after taxes to shareholders (through dividends and buybacks).

That wouldn’t seem conducive to further dividend hikes given that crude oil has been on the schneid for roughly a year. But it’s complicated. After years of stagnating production growth, GeoPark is committing $200 million to $220 million in capital expenditures to build out its production capabilities even further—a potential catalyst for future cash-generation growth. But between that and a considerable debt servicing cost, that’s a considerable sum not available to pad the dividend.

Between that and declining oil costs, it’s possible that GeoPark could pull the brakes on its dividend growth, at least in the short term. We’ll likely see one way or the other come early August. But GPRK could still be a compelling growth story longer-term—one that currently trades at just 0.6x sales and a little over 3x earnings estimates.

It’s Not Too Late: Lock In the “Recession-Resistant Portfolio” Now!

You know what trait is missing from most of these stocks?

Recession-resistance.

Like I said earlier: I don’t sweat economic pullbacks because I focus on rapidly rising dividends, which many times are signs of a recession-resistant stock—but not always. But the Fords and Hosts of the world clearly need the U.S. economy to hum along if they want to keep the pedal down on their dividends.

However, that’s not the case for a small, overlooked basket of recession-resistant stocks that haven’t just been surviving over the past couple years of market tumult—they’ve been thriving.

Better yet? They look like they could be the market’s best protective plays for the recession to come, regardless of whether it hits in 2023 or 2024.

To the uninformed investor, these stocks will seem downright boring. In fact, I’m betting that you haven’t heard of any of these—after all, the mainstream media rarely covers some of them, and it outright ignores others.

But selecting companies with a proven track of increasing their dividend payments is the safest, most reliable way to get rich in the stock market. And I want to show you how it’s done. Click here to get a copy of my 5 Recession-Resistant Dividend Stocks With 100% Upside report, including full analyses of each pick … and I’ll throw in a few other bonuses, too!

Recent Comments