The economy is a mess—and that’s presenting quite the opportunity for these landlords, and contrarians like us. Tenants are still paying, but these stocks are priced like a few are flaking.

That’s not the case. Plus, one firm is about to take advantage of a weak 2020 market to go shopping and secure future cash flows at a bargain.

Real estate investment trusts (REITs) are trading at 2020 discounts. Investors trashed these stocks swiftly and thoroughly when they realized April 1, 2020 rent payments were going to be a disaster. But we now have a few months of pandemic landlording in the books, and there’s evidence that some REITs are going to be all right after all.

The secret to REIT picking, right now, is to identify the companies that are still collecting payments like it’s 2019.

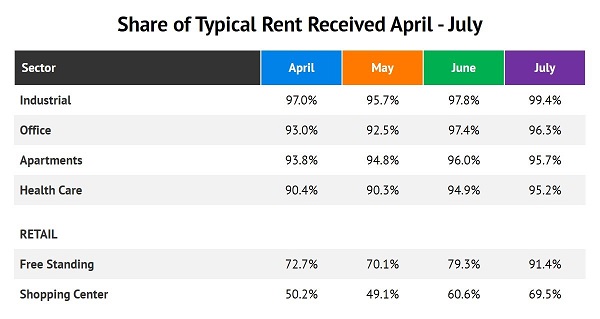

Here’s the rent collected by the REIT sector for April, May, June and July—all of our newly completed “shutdown” and “re-opening” and “just kidding, we’re closing again” months. It’s no surprise that industrial tenants are the most reliable:

(Source: Nareit)

Occupancy for the best industrial REITS never seems to dip. Take W.P. Carey (WPC), a picky landlord that only extends leases to companies in industries that can withstand “dislocations in the market.” Its underwriting team is acing its second dislocation test.

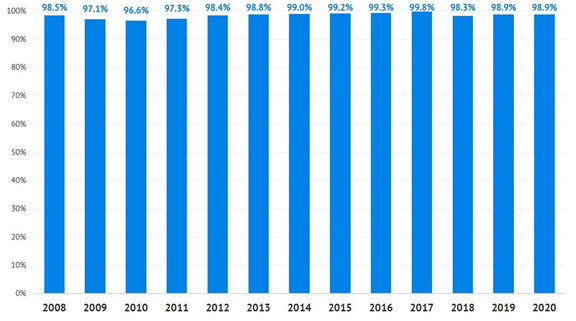

The firm’s occupancy rate held strong during 2008 at 98.5% and merely dipped to 96.6% in 2010. Through the first two quarters of 2020, its properties are humming at an incredible 98.9% occupancy (same as 2019 levels):

Occupancy (% Square Feet) Staying Strong

This is a 2019-quality business at 2020 prices, thanks to WPC’s smarts and broader panic respectively. This is a firm that raises its dividend every single quarter (since 2010). So, when we see a forward yield quoted for WPC at 5.9%, we know that’s a bit understated—it doesn’t consider the four payout hikes we’ll see between now and next August.

There aren’t many multi-year guarantees left in the financial world. But WPC is one of the few gems that we can buy today and sock away for years. Not only does it have steady cash flows and contractual rent increases in the books through the 2020s, but it also has plenty of breathing room to be able to deliver more dividends.

By the way, July looks good too, with the firm collecting 98% of the rents it was owed last month.

The firm is now taking advantage of low real estate prices by going shopping. CEO Jason Fox said he expects “to close a number of deals in the second half of the year.” He’s got $1.8 billion to play with thanks to a revolving credit line that is basically untouched.

Fellow REIT STORE Capital (STOR) yields an equivalent 5.9%. It also owns and operates industrial properties which likewise remain in demand in our socially distanced world.

STORE has a lot going for it. For starters, it’s diverse, with 2,554 properties in 49 states, and its customers operate in 113 industries (though as we’ll see below, a significant portion are retail-focused). It also sports a sky-high 99.5% occupancy rate.

Like WPC, STORE lowers its risk through its “triple-net-lease” model, where the tenant pays all the expenses: insurance, maintenance and taxes among them. STORE simply collects the rent!

Finally we can’t discuss industrial REITs without discussing the granddaddy of them all, Prologis (PLD). This powerhouse has grown its dividend by 45% over the last five years. Unfortunately, it is priced for perfection today at 30 times cash flow. The stock pays a modest 2.3% today.

A great dividend stock at an OK price? That’s not enough for me. When I’m looking for a “perfect income buy,” I really want it all:

- Maximum current yields,

- Rock-solid cash flows (like these industrial REITs), and even

- The potential to double in price as the dividend continues to climb.

The price we pay determines how much we’ll make (or even lose!) on a high quality dividend stock. Solid “fundamentals” are important but they alone are not enough. We must put on our contrarian hats and cherry pick these blue-chip dividends only when they are in the bargain bin.

If we do this, not only can we collect secure yields of 5.9% or better. We can also double our money as these dividends continue to climb.

Can I share more? Please click here and let me explain my Perfect “Crisis-Proof” Income Portfolio in detail.

Recent Comments