Is it time for us contrarians to “buy the dip” in bank stocks?

We’re drowning in big bank-scare headlines. Silicon Valley Bank (SIVB) knuckled under in days, Signature Bank (SBNY) wasn’t too far behind, and across the pond, Credit Suisse (CS) needed a buyout bailout from rival UBS (UBS).

The next bank run, however, won’t be with the big boys. Too big to fail, baby. Here, we’ll find not only government help but also secure yields of up to 5.1%—trading at a discount, no less.

Why the big guys? Well let me show you. Last week, my software firm received this email from one of our vendors:

“Brett, Just wanted to give you our new banking details. We’re out of SVB; we’re moving to JPM.”

JPM for the win. And they’re not the only big bank benefiting.

CNN recently reported that Bank of America (BAC), Wells Fargo (WFC) and Citigroup (C) “have all experienced a significant increase in deposits” since SVB’s shenanigans sent shockwaves through the regional bank industry.

Citigroup was speeding along account openings, CNN adds. BofA? Bloomberg says it hoovered up more than $15 billion in deposits in a matter of days.

The Federal Reserve has rushed in to limit regionals’ bleeding. But while this isn’t 2008, there are many losers in the banking industry—and a few winners at their expense!

The nation’s largest banks don’t have the “client concentration” problem (all tech bros) that sank SVB. Big bank depositor bases are far more diverse, as are their assets.

3 Big Banks on the Dip

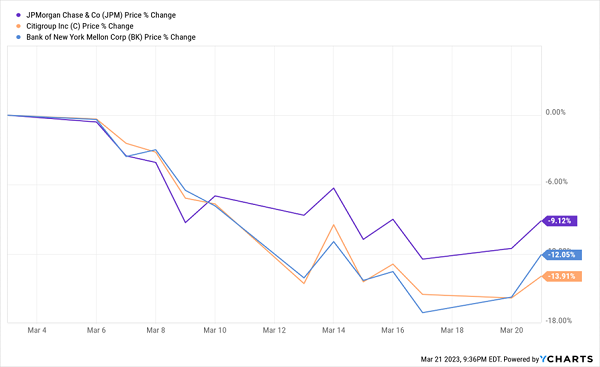

JPMorgan Chase (JPM, 3.1% yield), new home to many SVB refugees, was America’s largest bank at the end of 2022, with $3.2 trillion in global assets. It’s such a sturdy name in the banking sector that it’s on the other end of the bailout spectrum, helping another troubled bank stay afloat. JPM was among 11 large banks that recently pledged to deposit $30 billion into troubled First Republic Bank (FRC), and CNBC reported that JPM is actually advising FRC on strategic alternatives including a capital raise or outright sale.

JPM has a fortress balance sheet, is soundly profitable and highly liquid, with $540 billion sitting in deposits with central banks. The recent run on bank stocks has done nothing but make JPM a little more attractive—the stock’s 1.4 price-to-book ratio and 3.2% dividend yield still aren’t screaming “buy!” to me. But it’s certainly safe, as is a dividend that accounts for just 33% of the bank’s profits.

Citigroup (C, 4.5% yield) boasts a safe dividend, with a scant 29% payout ratio—and it trades at just half its book value. At $1.8 trillion in assets, it’s firmly fixed among America’s “Big Four,” and it’s also part of the FRC bailout.

But profits are lower quality here. Operating expenses continue to plague the company and helped induce a fourth-quarter earnings miss. Citigroup’s consumer banking division is also downsizing in Asia and emerging markets, narrowing an international opportunity. So while C shares certainly appear safe from a dividend perspective, it’s hardly the cream of the big-bank crop.

Bank of New York Mellon (BK, 3.3% yield), off by double digits since the run on financial stocks started earlier this month, is the 11th biggest bank by assets and another of the 11 institutions trying to keep First Republic afloat. Is it being thrown out with the bathwater? This is no consumer bank, but an investment bank—one that’s been plenty generous to investors, coming off a 9% dividend increase and a fresh $5 billion buyback plan.

Prior to the SVB brouhaha, Bank of New York Mellon was guiding for net interest income (NII) growth of 20% this year and was working on containing costs. It’s firmly facing the right direction—and trading at a slight 5% discount to book at present.

Regional Banks

The real pain has been felt at regional banks. SVB, Signature Bank, and First Republic are all considered to be in the regional set, after all, and perception matters—if those banks could fail, another regional could be next. This fear hasn’t sparked full-on bank runs, but it has caused some depositors to pull money from local institutions and sink it into the big boys.

But “regional bank” is an overly broad term extended to banks huge and tiny—from tens of billions of dollars in market cap to a few hundred million. And some of the much larger regionals might be taking more damage than they deserve.

2 Regional Banks to Keep an Eye On

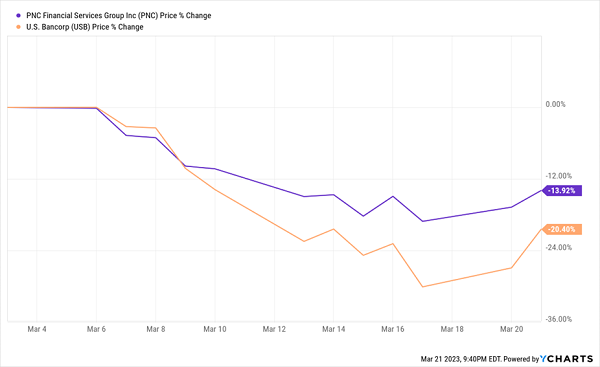

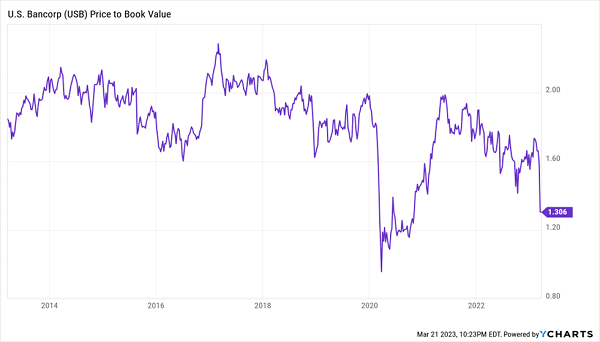

U.S. Bancorp (USB, 5.1% yield), the fifth-largest bank with $585 billion in assets, is a so-called super-regional that operates in 26 states, mostly in the western half of the nation. And it joined America’s mega-banks to preserve First Republic, ponying up about $1 billion.

USB shares have been cut by more than 20% in the regional-bank rout, driving shares to a much more reasonable valuation of about 1.1 times book. That doesn’t sound great, but U.S. Bancorp shares have long traded at a premium—this recent stumble has brought prices back to pandemic-era levels.

USB: Not a Steal, But a Relative Bargain

USB has long been a high-quality bank that, if anything, is likelier to enjoy an influx of deposits coming from smaller regionals than it is to lose deposits to mega-banks. Its dividend accounts for a hair more than half of its profits, so it’s possible tighter capital requirements could shave it down. But even with a theoretical 20% haircut, USB’s payout would still deliver a respectable yield north of 4%.

PNC Financial Services (PNC, 4.9% yield), for instance, is a “super-regional” bank that has some sort of presence in every state, as well as international offices in Canada, the U.K., Germany and China. It’s actually the sixth-largest bank by assets, at $552 billion, and it too is among the Bailout 11 trying to save FRC. And despite a nearly 5% yield, coverage looks healthy with a payout ratio of just over 40%.

But a tightening of stress tests could be problematic for PNC. While plugging away at research, I came across a KBW note examining possible stress-test tweaks. PNC was among the regionals that produced “challenging results.” Translation: If the Fed does clamp down, it might have to pull back on loan growth to improve its liquidity and capital position.

It’s Not Too Late: Lock In the “Recession-Resistant Portfolio” Now!

Banks might look like a bargain right now, but they could stay that way for a while. With recession seemingly on the horizon, the last thing we want to do is jump into cyclical, economically sensitive financial stocks too early.

No, if we’re looking to get our retirement portfolios into “survival mode,” we want to value one trait above all others:

Recession-resistance.

While every major market index was dead money in 2022, and while most of the darlings of the stock market have been getting crushed, a small, overlooked basket of recession-resistant stocks haven’t just been surviving—they’ve been setting up to thrive.

And now, they look like they could be among the market’s best protective plays heading through a turbulent 2023.

To the uninformed investor, these stocks will seem downright boring. In fact, I’m betting that you haven’t heard of any of these—after all, the mainstream media rarely covers some of them, and it outright ignores others.

But these “Hidden Yield stocks” offer savvy investors the potential to double their money roughly every five years, regardless of what the wider market does.

How can they do this when even idiot-proof blue chips can’t?

It all boils down to what I call “The Three Pillars”:

Pillar #1: Consistent Dividend Hikes

Pillar #2: Lagging Stock Price

Pillar #3: Stock Buybacks

Selecting companies with a proven track of increasing their dividend payments is the safest, most reliable way to get rich in the stock market. And I want to show you how it’s done. Click here to learn how to get your free copy of my 5 Recession-Resistant Dividend Stocks With 100% Upside report, including full analyses of each pick … and I’ll throw in a few other bonuses, too!

Recent Comments