Hey kid, want some candy?

Don’t worry about the wrapper. It, um, came like that.

No? No candy for you? You’re sure?

OK fine. Maybe you’re not hungry, but how about this 31% dividend?

Don’t worry. The stock made its last dividend payment of $0.27 just fine.

No? No 31% yield for you? You’re sure?

OK fine. And, honestly, smart move. I would imagine that January dividend payment is the last one we ever see from First Republic Bank (FRC).

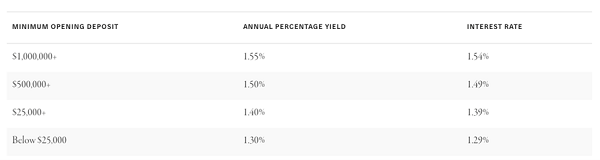

Fundamentally, FRC (and other banks, for this matter) are flawed, perhaps fatally so. They are not paying competitive rates. Check out this screenshot I took from FRC’s website last Friday—just prior to the fire sale to JPMorgan Chase (JPM):

Wow, what a deal. We can open a savings account with a bank that is about to fail and receive a 1.29% interest rate.

One point two nine percent. In a five percent world!

The rates for big opening deposits of $500,000 or even a million dollars aren’t that much higher. Only up to 1.54%—yikes. And the risk! Why would we put more than the $250,000 limit that the FDIC insures into any bank account these days?

As full-time financial analyst and part-time funnyman Jim Bianco points out in his frequent interviews, we all have phones. We all have mobile banking apps. It’s a few taps for an FRC customer to move savings money making 1.29% over to a money market fund paying 5%.

Hence the big problem in the business model of most banks today. They are only making money because they are underpaying their customers.

Dividend history doesn’t mean much when harsh realities set in.

We talked about this last week when we picked on office REITs (real estate investment trusts). Office work is becoming a relic of the past, and commercial landlords are learning this the hard way.

Last August we called out five stocks that looked fine in the rearview mirror. They weren’t. Office Properties Income Trust (OPI) was our star student, declining 58% since our sell call.

We picked on mortgage REITs (mREITs) in that initial piece, too. MREITs don’t own empty buildings. They own paper.

Specifically, they buy mortgage loans and collect the interest. How do they make money? By borrowing “short” (assuming short-term rates are lower) and lending “long” (if long-term rates are, as they tend to be, higher).

This business model prints money when long-term rates are steady or, better yet, declining. When long-term rates drop, existing mortgages become more valuable (because new loans pay less).

The problem lately is that the traditional mREIT’s gravy train derails when rates rise and its mortgage portfolio declines in value. Historically, rising rate environments have been very bad for mREITs and resulted in deadly dividend cuts.

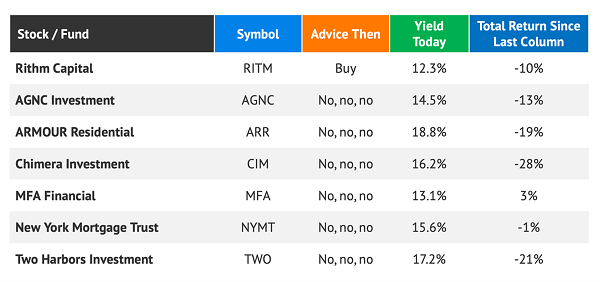

While the payouts in the sector have largely hung in there thus far, we warned last August that everything mREIT was a sell, with the exception of Rithm Capital (RITM).

I’ve always had a soft spot for RITM because it bought mortgage servicing rights (MSRs) hand over fist before rates rose. MSRs increase in value as rates rise, and they serve as a nice hedge when housing slows down. Perhaps my soft spot was a blind spot for yours truly, because RITM had a rough go along with the rest of its peers:

Remember, these are total returns, which include dividends. Most of these companies are paying their dividends and losing more in price. Which, obviously, is not what we want from income investments. We want price stability at minimum.

I expect that long-term interest rates will bounce again in the coming months. That will be bullish for RITM, owner of MSRs, and bearish for the rest of the sector. It could be the tipping point for the other six mREITs, and not in a good way.

The sector-at-large should still be avoided outside of RITM. Let’s not get blindsided by these big stated yields. Cuts could very well be coming.

There are better, safer big yields to buy instead. With a banking crisis unfolding, this is no time to mess around. We need to “crisis-proof” our retirement portfolios by following these important steps.

Recent Comments