If you’re like most folks, you’re about to put your portfolio on autopilot as the lazy days of summer roll in.

It’s an easy trap to fall into, but you must not take the bait, as I’ll explain in a moment. Later on, I’ll show you two hidden dividend-growers that should be on your buy list now. Both are ready to double their payouts in short order!

First, back to the season at hand.

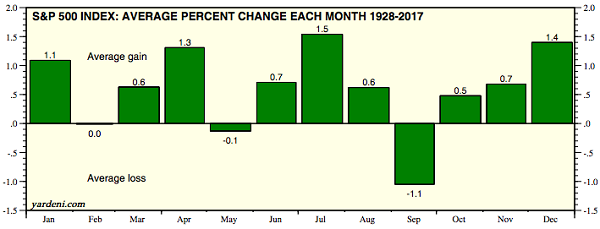

I can see why most folks check out around now. After all, July has been the best month for stocks over the last 89 years, and August hasn’t been too bad, either.

Mr. Market’s Sunny Summer

Source: Yardeni Research

In fact, the last two Julys have been positively scorching, with stocks climbing 3.5% last year and 2% in July 2015.

But there’s one big difference from the last two years, and it’s this: the S&P 500 has spiked a lot higher year-to-date: 8.5%, to be exact. The index now sports a nosebleed P/E ratio of 24!

That has me worried that this July could turn out like July 2014. You might recall that the S&P 500 had soared some 8% heading into that month, only to give back nearly a quarter of those gains before August 1.

And with second-quarter GDP forecasts being cranked back and the White House’s infrastructure and tax plans in suspended animation, who knows what the back half of the year will bring?

Look, I’m not saying you need to cancel your trip to the cottage here. But I am saying we need to keep a wary eye on our portfolios, especially with September—typically the ugliest month for stocks—around the corner.

The good news? You can take a vacation from volatility and boost your income stream with a few quick tweaks—including adding the 2 sweet summertime buys I’ll show you shortly.

But first, we need to talk about …

The One Place Not to Put Your Money Now

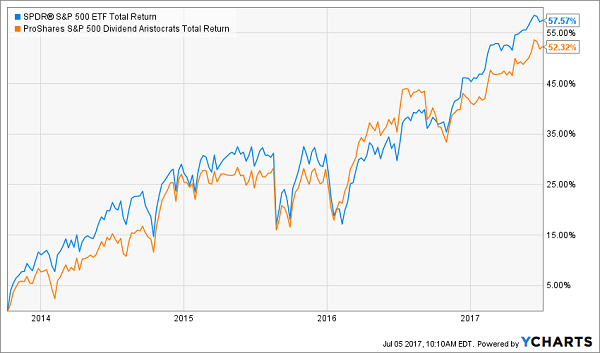

When things get rocky, it’s tempting to run to the comfort of the vaunted Dividend Aristocrats—the 51 companies that have hiked their payouts for at least 25 straight years.

The problem? Most of these so-called royals are over-the-hill penny pinchers: the ProShares S&P 500 Dividend Aristocrats ETF (NOBL), which tracks all 51 of them, yields just 1.7% today. You could buy the whole index through the SPDR S&P 500 ETF (SPY) and get 1.9%!

Worse, too many so-called Aristocrats are dribbling out weak dividend hikes just to keep their membership in the club. And as I demonstrated with Pfizer (PFE) on June 26, dividend growth is an absolutely vital driver of share prices.

The result? Our Aristocrat ETF is actually trailing—and has consistently trailed— SPY since its inception in October 2013, even with dividends included!

Commoners: 1, Aristocrats: 0

Now I’m not telling you to avoid all Dividend Aristocrats here.

But you do need to steer way around those with the earmarks of a pauper: weak payout growth, overheated valuations and payout ratios (or the percentage of earnings paid out as dividends) that stray much above 50%.

(To give you a starting point, I named 3 Dividend Aristocrats that deserve the title and 2 pretenders in my June 2 article.)

But let’s move beyond the Aristocrats. To find the companies with high-octane dividend growth that’s sure to squeeze their share prices higher, we’re going to look in 2 places most people don’t, starting with…

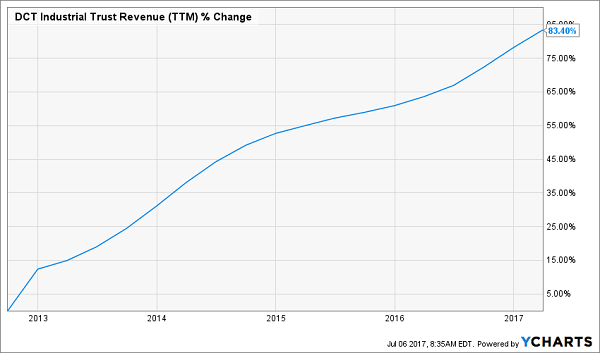

A Red-Hot Industrial REIT

Consider this: if online retailers double their 10% share of US retail sales (practically guaranteed), they’ll need another 600 million square feet of warehouse space.

That puts industrial real estate investment trusts like DCT Industrial Trust (DCT) in the sweet spot: it owns stakes in 74.0 million square feet of leasable space across the US.

Tenants can’t wait to move in. In the first quarter, occupancy jumped to 97.5% from 95.8% a year ago. And look at the spike in DCT’s revenue over the past five years:

Fatter Rent Checks Roll In

Even so, there are a few things keeping this pick below the herd’s radar.

One is its modest dividend yield—just 2.3%. Another is the fact that it only started boosting its dividend again in late 2015, after a six-year freeze; including that first hike, the payout’s up about 10%.

That’s pretty weak, but DCT can easily do more: it’s paid out a very low (for a REIT) 50% of adjusted funds from operations (FFO; the REIT equivalent of earnings per share) as dividends in the last 12 months. Plus, management is calling for a 7% to 9% jump in FFO this year.

And while I’m at it, let me dash another overdone worry: that DCT is too expensive at 23.8 times trailing-twelve-month FFO.

Truth is, that’s reasonable for a growth REIT with a massive e-commerce tailwind, and it’s right about where DCT’s ratio was a year ago. And based on the midpoint of management’s 2017 forecast, the trust’s forward price-to-FFO ratio falls to 21.4.

Let’s grab this one now, before the share price races further away from us.

The Perfect Digital Advertising Play (It’s Not Google)

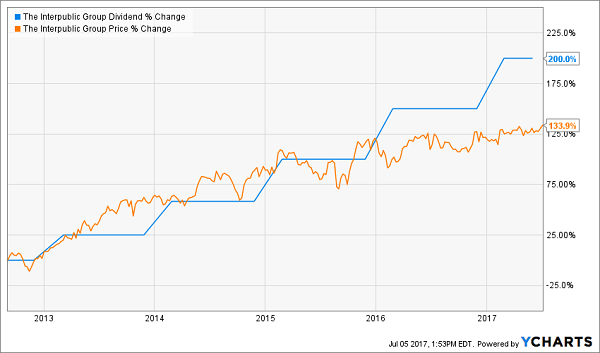

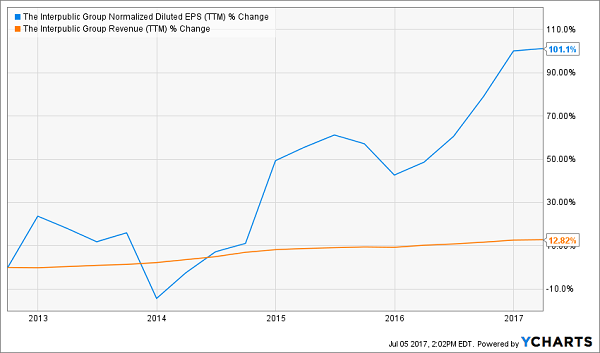

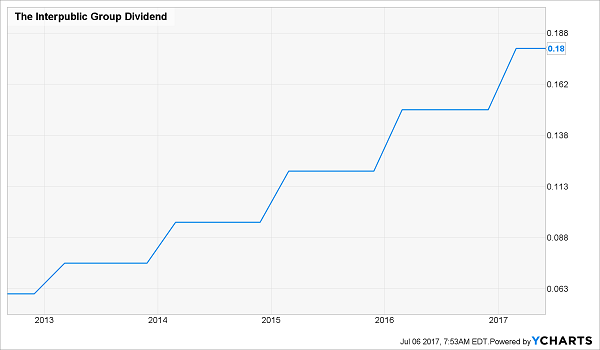

Interpublic Group (IPG) yields 2.6% and has much stronger dividend growth than DCT: the advertising giant has tripled its payout in just five years!

Look at what that’s done to the share price:

A Classic Triple-Double

Take a close look at that chart. You can clearly see that the stock jumps up with every single payout boost … except the last two. That means a catch-up is way overdue. And it will come.

Why?

Because the company keeps cashing in on the shift to targeted online ads—a shift that’s far from finished. That’s driven a double-digit revenue growth and a doubling of earnings in the past five years:

A Creative Juggernaut

Yet despite that performance, the market values this one at just 16.4 times earnings! That’s far below its five-year average of 19.0 and the S&P 500’s over-inflated number. It’s totally ridiculous for a company that owns some of the biggest names in the ad business.

Sure, the herd could keep ignoring IPG, but I’m betting it won’t, because management can grab their attention with a fat dividend hike at any time. The company pays out just 39.9% of free cash flow as dividends, has low debt and almost $800 million of cash waiting to be doled out. Click “buy” now.

Just Released: 7 Urgent Buys for Up to 800% Payout Growth

You’ll totally miss out on stocks like IPG if you make the same mistake almost everyone does: focusing on current yield when it’s dividend growth that matters.

Let’s take another look at the spike in the ad firm’s payout:

As I mentioned above, if you bought today, you’d get a 2.6% yield. That’s more than you’d get from your typical S&P 500 stock … but still pretty ho-hum.

But if you’d bought five years ago—when the current yield was 2.2%—you’d be pocketing a fat 6.5% on your original buy today!

That’s because, as the ad giant’s payout shot higher, more investors bought in, driving the stock price up but keeping the current yield roughly the same (because you calculate yield by dividing the annual dividend payout into the share price).

But if you only look at the current yield, you’ll skim right over “hidden” yields like this one—and they’re what really matters!

There’s more, though.

Because I’m pounding the table on 7 stocks with even faster dividend growth than DCT and IPG, so the yield on a buy today will shoot higher much quicker.

I’ve put all 7 of these cash gushers in a NEW special report—“The 7 Best Dividend Growth Stocks With 100%+ Upside”—YOURS FREE.

Here are just a few of the stocks you’ll discover in this breakthrough FREE report:

- The water company that’s turning every $1 in sales into $10 in free cash flow. This one could easily give shareholders a nice raise today—and its next dividend hike will be BIG.

- The smooth operator that’s hiked its dividend TWICE in the past year. At this rate, it will double its payout in 4 or 5 years, turning our 4.7% yield into a rock-solid 9.4% income stream!

- The 800% dividend grower: This ignored company has boosted its payout eightfold in just four years, and it’s just getting started! Plus, management is jumping on the stock’s absurdly cheap valuation, carefully using share buybacks to set us up for even bigger gains.

- PLUS 4 more stocks set to double their payouts fast.

I’m ready to show you all 7 of these standout companies now. All you have to do is click here and I’ll share my full strategy and give you a copy of this eye-opening special report.

Recent Comments