We’re going to ride this Silicon Valley Bank (SIVB) fiasco to big dividend payouts—I’m talking yields up to 12.6%!—and quick upside, too.

I’ll walk you through exactly what we’re going to do below. Then I’ll name two unloved (for now!) dividends we’ll target.

We’re Not Dropping a Quarter Into GameStop II

One thing we’re not going to do is sell anything short—even though, as Bloomberg recently told us, the “shorts” cleaned up on SVB. All in, they pocketed $2 billion as “tech bros’” fav bank froze, then crashed.

We contrarian dividend players tip our hats to these daring degenerates. They rolled the dice and things broke their way.

Here’s the thing, though: big short-seller losses are far more common than wins. Because for every SVB there are two (or more!) tales like GameStop (GME)—a stock that needs no intro.

You remember the story:

- Hedge funds were massively short GME (more than 100% of its shares were sold short).

- Internet bros and gals learned this and started buying, forcing the shorts to cover their positions, which drove the stock higher still (a classic “short squeeze”).

- Hedge fund Melvin Capital blew up entirely.

- “Long” buyers who got out before the stock price collapsed made a fortune. Those who held on lost everything.

(By the way, if you haven’t seen the Netflix documentary Eat the Rich: The GameStop Saga, you should. It’s a fast, fun watch.)

We contrarian dividend traders prefer to stay out of short selling. For one, there’s no income in it. In fact, short sellers have to pay dividends on shares they’ve shorted—something most folks don’t realize.

Second, when you buy a stock “long,” your losses are limited—the worst that can happen is it goes to zero. With short selling, your potential losses are unlimited because there’s no telling how high prices can go.

But there is a way we can flip short interest—the percentage of a company’s “float” sold short—to give us an edge. Which brings me to the 2-step strategy we’re going to put into action today.

Essentially, we’re on the hunt for dividend payers with:

- High short interest (or 10%+ of the float sold short). That gives us a shot at a short squeeze. The fact that the shorts are on the hook for the payout adds extra pressure.

- Insider buying. You likely know the old adage about insider trades: there are many reasons why an exec might sell their firm’s stock. But they only buy for one: they think it’s headed up. (I’ll go ahead and add a second—they think the dividend is safe.)

With that in mind, let’s talk tickers:

Insiders and Short Sellers Scrap Over This 12.6% Payer

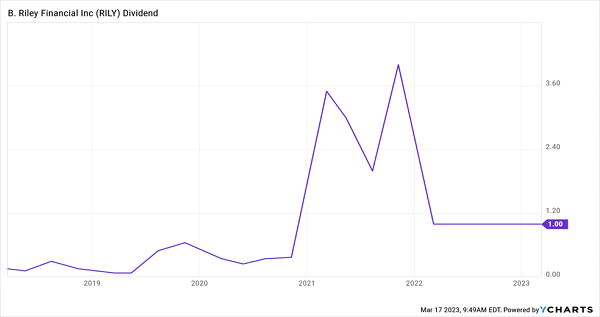

B. Riley Financial (RILY) is a tantalizing swing-trade possibility with a massive 12.6% dividend.

And we’ve got a nice insider buy lighting the way in from Chairman and Co-CEO Bryant Riley, who recently bought $387,205 of the stock. The shorts? They’re swarming, with 19% of the company’s float sold short. And remember, these folks are paying that 12.6% dividend! Which is why I don’t expect them to stay short for long.

Riley is a financial-services firm in a bunch of businesses, including wealth management, capital markets, consulting, and auction and liquidation.

The company tends to grow by acquisition, which leads to choppy cash flow, revenue and, well, dividends—though it’s $1-a-share quarterly payout has held up the last couple of years, with two special dividends thrown in:

RILY’s Payout Soars—Then Holds the Line

There are a couple concerns here, though: one, Riley’s free-cash-flow payout ratio is negative—so it’s paying a dividend while generating negative free cash flow. That’s obviously not sustainable for long.

But there are a couple other things to bear in mind, like last year’s market denting revenue at capital markets and wealth management. Plus some brokers decamped after Riley bought National Securities in ’21.

And you do have a healthy balance sheet here, with $2.45 billion in debt and $2.15 billion in cash and investments.

This all points to the challenge with Riley: it has a lot of moving parts. But its high short interest—enhanced by its sub-$1-billion market cap and huge dividend—suggest a pop in the stock. Riley’s president certainly thinks so!

This 6.6% Payout Is Sticking It to the “Shorts”

HASI (HASI) is a name you might remember if you’re a member of my Contrarian Income Report service: we bought the stock—then under the Hannon Armstrong moniker—in April 2017, when it yielded a gaudy 6.6%.

A little over two years later, in September 2019, we sold for a 54% total return. That run had whittled HASI’s yield down below 5% when we bowed out. (This was HASI’s only “crime”—it performed so well we had to take our cash off the table!)

Fast-forward to today and we have another shot to buy at a 6.6% yield. That makes HASI another intriguing play, with a holding period longer than I’d recommend with RILY.

Right now, for example, we’ve got short interest on the “high-ish” side, at 9% of the float, plus a couple insider buys on the table, with CEO Jeffrey Lipson recently picking up $73,080 of HASI shares and Executive Vice-President Susan Nickey adding $47,820 worth.

HASI is classified as a mortgage REIT, even though it finances green-energy projects for governments. This is a nice niche because going with HASI saves governments the hassle of issuing bonds themselves.

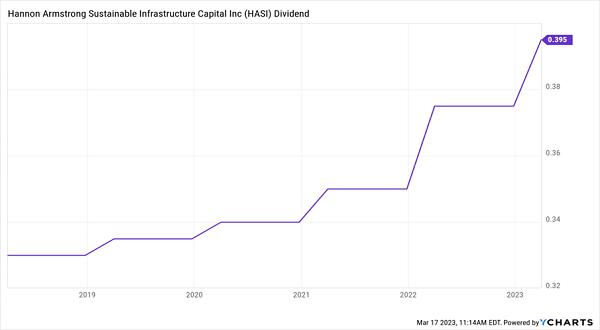

The REIT ended 2022 with $4.5 billion of projects in the pipe, up from $4 billion at the end of ’21. It also closed $1.8 billion of financing deals despite the 2022 dumpster fire, up from $1.7 billion in ’21. Plus, in addition to its high yield, HASI’s payout is growing steadily:

HASI’s Dividend Goes “Green”

At the end of the day we’re left with a government-backed business with a high yield and a growing dividend. Let’s side with Lipson and Nickey—and collect our 6.6% payout as the shorts get taken to the cleaners.

You’re Seconds From Getting the Next 6.6%+ Paying Winners

As you no doubt know, indicators like short interest and insider buying are tough for individual investors to track down on their own.

Which is why I want to offer you a no-risk 60-day trial to my Contrarian Income Report service today.

By taking CIR for a “road test,” you can farm this research out to me. With the tools I have here at CIR, I’ll guide you to contrarian income plays with big, safe dividends—plus hidden upside that most people simply miss.

Click here and I’ll share my complete CIR investing strategy with you and show you how to start your 60-day trial. I’ll also include a free copy of my exclusive Special Report, “The Perfect Income Portfolio: How to Safely & Securely 4X Your Income—Almost Immediately.”

The strategies inside will give you my best tools for boosting your dividends and your nest egg, potentially letting you retire much sooner than you think you can.

Don’t miss out. Click here to take me up on this no-risk offer and get access to the full Contrarian Income Report service now.

Recent Comments