A smart bond portfolio (picked by humans rather than “dumb” machines, of course!) will take the stress out of retirement investing. It’s like an annuity, but better – because we get to keep our capital.

And our Contrarian Income Report portfolio pays us more than any annuity product the big firms peddle to line their pockets with fees. Our handpicked basket yields 7.3% as I speak. And this is pure interest. You don’t spend any of your capital!

That’s right. Your money stays intact – or better. And it can potentially do much better and grow by up to 68% in a couple of years (more on this shortly). All by buying safe bonds.

Most Wall Street spreadsheet jockeys say we investors can’t have both the income and safety of bonds and the upside of stocks. We have to choose, or allocate, or whatever. They’re wrong – here’s why.

Two Steps to 8%+ Yields and 68% Gains

To make money with a bond fund, we want:

- Meaningful current and future yield, and

- Upside price potential, too.

I define meaningful current yield as 5% to 10%. This eliminates most mutual and exchange traded funds (ETFs), which is no surprise – most of these vehicles are marketing-driven. I’ll show you how to find 5%+ bond payers that are performance-driven in a moment.

Next, let’s talk upside. Between dividends and capital gains, the investment must have the potential to deliver total returns of 8% to 10% or more per year. Dividends will make up the bulk of these profits, of course. The additional upside gives us a nice kicker and a margin of safety to boot.

For bond funds, upside can come in two ways. First, when the price of a fund lags its net asset value (NAV), there is a “discount window” which could subsequently narrow or close. A buyer pays, say, $0.90 for $1.00 of actual investment value (who wouldn’t do that all day long?) We specifically target funds when they are unfairly out-of-favor and have big discounts so that we can profit when investors realize these windows are open too wide:

Funds can also gain when NAV itself increases. This means the “liquidation value” of the fund – the value of the bonds, stocks, options or whatever financial instruments it holds – goes up.

These upside drivers also provide us with a margin of safety on our investment. When it comes to income investing, the best defense is the best offense. You can’t keep a good dividend payer down – especially when it’s underpriced today.

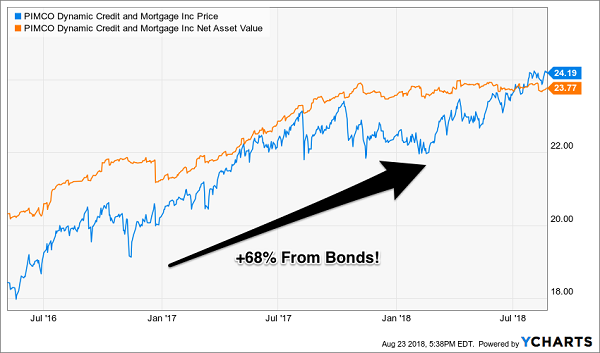

This is exactly what happened when we purchased PIMCO’s Dynamic Credit and Mortgage Fund (PCI). Not only did we collect the fund’s generous dividend (which ranged between 8% and 9%+) but we won two more ways when its:

- NAV increased (orange line below), and

- Its discount window tightened as its price (blue line) caught up with – and eventually surpassed – its NAV.

Two Ways to Win for 68% Total Returns

We have earned 68% total returns (and counting) from PCI in just two-plus years thanks to the distributions we’ve collected, the NAV gains we’ve enjoyed and the discount window closing entirely – and flipping to a premium!

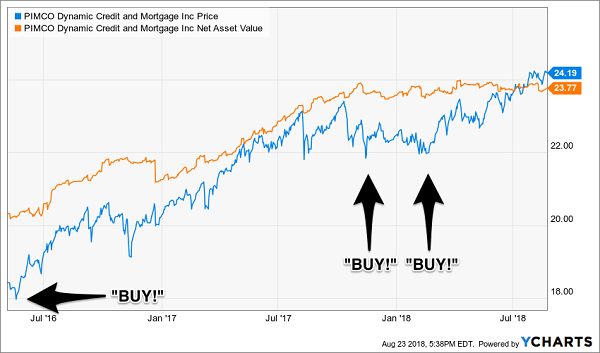

For much of PCI’s run, I’ve had a “buy” rating on the stock when this “triple threat” potential remained in place. Not only did we call a great run in this fund, but we also “pounded the table” to buy the dips, too:

Our Buy Ratings To Date on PCI

For a period of time in between our “buy” calls, PCI was cruising along as a “hold” for us. This happened after its price rallied so furiously that its discount window, for a period of time, narrowed completely.

When this occurs, it makes sense to simply bank dividend payouts and wait for our next buying opportunity. That’s exactly what happened with PCI. Its NAV continued to head higher (orange line) while its price dropped lower (blue line) – which triggered another buying opportunity late last year.

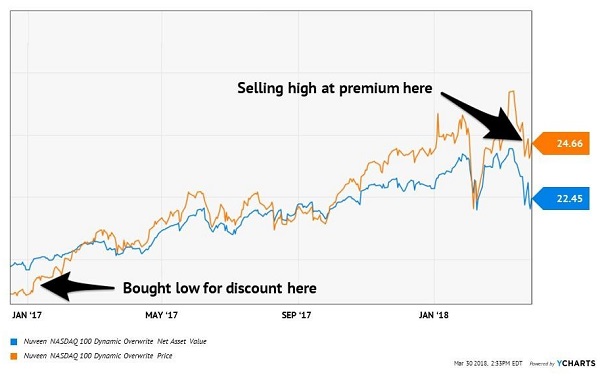

When a fund rallies to too rich a premium to NAV – when we’re paying, say, $1.10 for a $1.00 of actual investments (why would we do that?) – we sell it. That’s what we did last month when we banked 41% total returns on our Nuveen NASDAQ 100 Dynamic Overwrite Fund (QQQX). The fund became too popular with the first level-types, rallying quickly from a discount to an aggressive premium:

We Bought Low and Sold High

And Get Your Management Fee “Comped”

Another advantage of buying at a discount? When the discount is greater than the management fee- and we don’t buy if it isn’t! – we in effect pay zero management fee.

Let the “first-level” investor types waste time over which dumb computer-driven fund pays the least. You and I can pay a well-connected bond manager nothing while we lock in 8%+ yields with big upside when we buy their funds at a discount to NAV.

Again, this isn’t available to most investors because they only consider mutual funds and ETFs. But that isn’t the best way to buy bonds.

68%+ Upside and Safe 8%+ Dividends—in One Buy

What’s more, you can grab these lofty payouts whenever you’re ready: all at once, on a yearly, quarterly or monthly schedule … or simply whenever you have new money to invest.

It’s all up to you!

Best of all, each of these four incredible investments are about to explode and give us massive price upside, too.

How massive?

I’m talking 20%+ yearly price upside here, on top of dividends of 8%, 11% and even higher—without having to buy in the middle of a market meltdown, like our 2009 buyers did.

Just 2 days ago, I released the whole incredible story on these four Dividend Conversion Machines to the public for the first time, including their names, ticker symbols, exactly how they work and how to buy (hint: you can grab these four incredible Dividend Conversion Machines straight from your brokerage account.)

Recent Comments