Make no mistake: The “Mallpocalypse,” the “Retailpocalypse,” whatever you want to call it, is very real, and its shockwaves are being felt in just about every corner of the brick-and-mortar retail world. In fact, there are only a few true havens left – including a few higher yielders in the 5%-6% range. We’ll get to those in a minute.

Every other week, it seems like there’s another story about a retailer going bankrupt or shuttering locations. Just consider some of the store closings lined up for this year:

- Abercrombie & Fitch (ANF) is going to shut down 60 of its 868 locations in 2018.

- Prviately held J. Crew closed 39 stores between late last year and January 2018 – more than the 20 it initially announced.

- Sears (SHLD) will shut down 103 units in 2018.

- JCPenney (JCP) and Macy’s (M) are each slated to close a handful of locations this year.

That’s obviously bad news first for the companies involved – the media has beaten the dead horses of Macy’s, JCPenney and Sears for years, and rightfully so as they shrink their physical footprints without making a real dent online to match.

But they’re not the only victims.

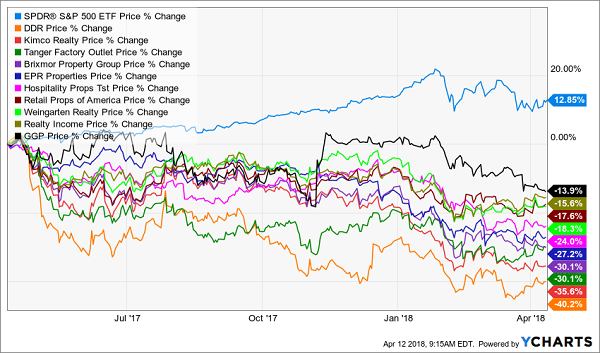

No, retail’s demise is hitting their landlords especially hard too. The real estate investment trust (REIT) sector is taking it on the chin. Check out the chart below – the 10 biggest retail REITs have dropped between 14% and 40% over the past year (while the market has risen nearly 13%!):

Retail REITs Have Dropped 14% to 40%!

That’s a double whammy for retirement investors, who dove into these REITs not just hoping for growth, but naturally the outsize dividends and income growth their traditionally stable business models provide. Instead, these yields are just countering some (but not even close to all) of the losses these stocks are sustaining.

A few REITs do sport businesses that appear more resistant than others to Amazon’s axe. But even then, not all of these rare exceptions are thrivers – just merely survivors. Let’s look at a crop of three REITs yielding roughly 5%-6% that might fit the bill, and sort out the cream.

Getty Realty (GTY)

Dividend Yield: 4.7%

One business that Amazon hasn’t exactly seemed keen on getting into is gas stations, which is good news for Getty Realty (GTY). Getty owns convenience store and gas station properties, and leases them out to a host of operators including BP (BP), ConocoPhillips (COP) and Exxon Mobil (XOM).

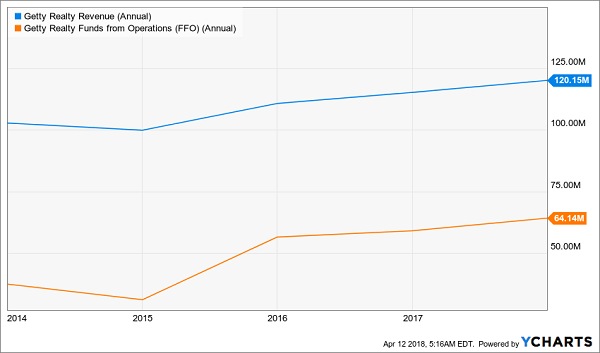

This REIT has a troubled past. Seven years ago, Getty Petroleum – one of its biggest customers – suffered oil cleanup costs so severe that they eventually forced the company to go under. Getty Realty, though, survived by repossessing the gas stations it leased out to Getty Petroleum, then leased those out elsewhere. Now, the company has a reach of 907 properties across 28 states and the District of Columbia.

Low to moderate gas prices have kept Getty’s customers fueling up like crazy, with the number of miles driven on U.S. roads increasing for years. Better still, those low gas prices have helped boost sales in convenience-store sales – also the higher-margin side of the business.

But it hasn’t played out that way at all. Low gas prices have not only attracted drivers, but driven up sales in their convenience-store operations, which boast far better margins than fuel sales. Better still, the company engages in long-term triple-net leases with rent escalations of 1%-2% per year. That helped fuel a nearly 9% increase in funds from operations in 2017.

Maybe Amazon will one day decide to disrupt this industry, too. But until then, Getty looks solid.

Simon Property Group (SPG)

Dividend Yield: 4.8%

By all rights, Simon Property Group (SPG) should be a dead REIT walking. After all, Simon – one of the largest retail REITs on the market – is also one of the most recognizable names in traditional malls.

Yet SPG has held up relatively well. Its 11% losses over the past year don’t exactly merit a champagne toast, but that’s certainly more resilient than most of its peers. Better still, those losses have helped prop up Simon’s dividend to nearly 5%, making it worth a closer look to see if we’re dealing with a true diamond in the rough.

One thing I want to highlight up front is the company’s ability to pivot into the new retail reality.

For one, Simon recently announced plans for five of its “key locations” – the company will be redeveloping shuttered Sears locations to introduce features such as new shops, dining halls, restaurants, entertainment venues and even fitness facilities. In short, Simon is actively answering the question about what to do when these mall-anchor giants are finally forced to pack up their tents.

The company also is developing mixed-use properties, such as its project at Atlanta’s Phipps Plaza that will include dining, retail, a LifeTime Fitness facility and even Class A office space.

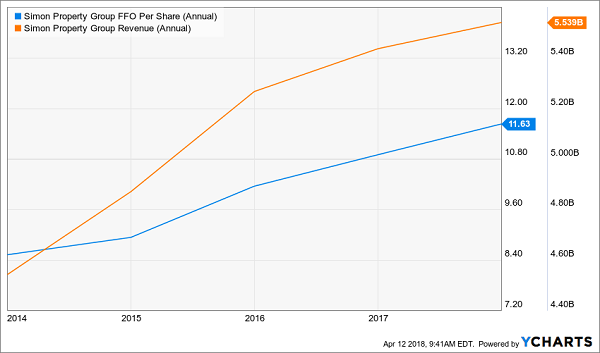

More importantly, Simon is still finding a way to squeeze even more profit out of its existing locations. The company raised rents by about 2.9% year-over-year, helping it improve its funds from operation by 6.9% to $10.49 per diluted share.

Yet SPG is trading at less than 70% of net assets. In short, the market sold the nasty rumor, but still hasn’t bought the much more uplifting news.

Does It Look Like This Mall Stock Is Dead?

Tanger Factory Outlet Centers (SKT)

Dividend Yield: 6%

Tanger Factory Outlet Centers (SKT) certainly isn’t immune from fears of the Mallpocalypse. Shares are down some 30% in the past year as the stores-are-dead narrative has blasted just about every retail REIT.

And on its face, you’d imagine Tanger would, in fact, be right in the crosshairs. After all, Tanger owns, operates or has an ownership interest in 44 upscale outlet malls across 22 states, with 510 different companies – from Ecco to Kate Spade and Tumi – setting up shop in its malls.

But for all the worry of Amazon breathing down its neck, just look at Tanger’s numbers.

Occupancy of 97%, while slightly down year-over-year, is basically in range of its operating history since 1993. Meanwhile, SKT actually grew its adjusted funds from operation from $2.37 per share in 2016 to $2.46 in 2017.

I’m also impressed with management’s aggression on the dividend front. Tanger boasts a three-year dividend CAGR of 13% — an escalation of its dividend growth that’s essentially unmatched in its history.

Forget These Middling Yields: Grab These 7.5%+ Payers (with 25% Upside!)

While you could get lucky by jumping into the best of a bad breed, why take the chance when you could secure 7.5% income right now and 25% gains in the next 12 months from my two favorite REIT plays.

My favorite commercial real estate lender lets us play Monopoly from the convenience of our brokerage accounts. They do all the legwork, building a secure, diversified loan portfolio featuring offices, retail space, hotels and multifamily units.

Management then collects the monthly payments, deposits the checks

– and then it sends most of the profits our way as dividends (a requirement of its REIT status).

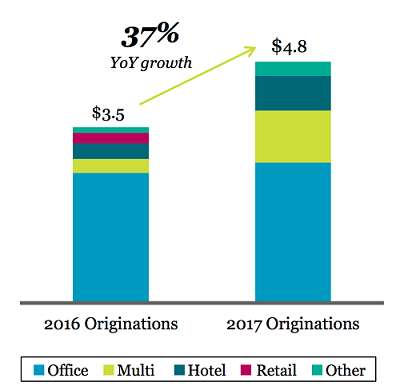

The stock’s current dividend (a 7.7% yield today) is covered by earnings-per-share (EPS) today. And don’t be fooled by the stagnant dividend (not that stability is bad). The firm continues to originate an increasing number of loans:

37% Loan Growth Today Tees Up Dividend Growth Tomorrow

This firm is a conservative lender with perfect loan performance (100%). Its growing portfolio will drive higher profits, which in turn will inspire the next dividend hike. The best time to buy the stock is right now, as it makes the investments which will drive its payout and share price higher from here.

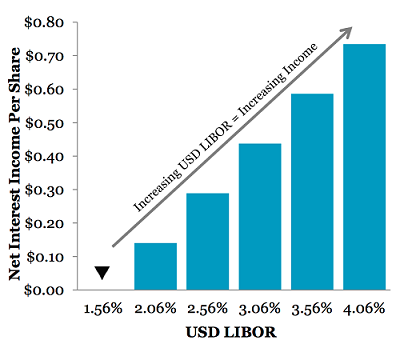

Plus this firm has also smartly eliminated interest rate risk because it uses floating rates. In fact, it’s actually set up to make more money as interest rates move higher:

More Income as Interest Rates Rise

Same for another REIT favorite of mine, a 7.5% payer backed by an unstoppable demographic trend that will deliver growing dividends for the next 30 years. Interest rates are no problem for this landlord because it will simply continue raising the rents on its “must have” facilities.

Its founder Ed Aldag admitted that, fourteen years ago, he had “zero assets, a dream, and a business plan.”

Well his dream and plan were plenty – Ed parlayed them into $6.7+ billion in assets!

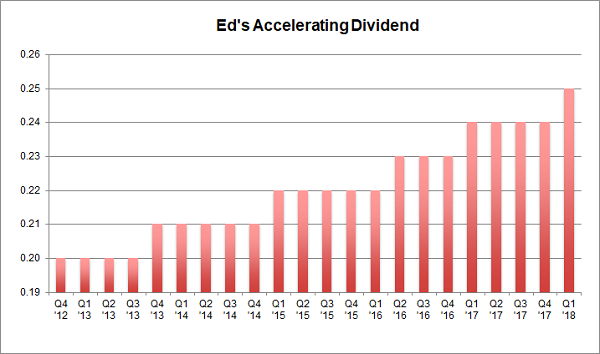

And right now is the best time yet to “bet on Ed” because his growing base of assets is generating higher and higher cash flows, powering an accelerating dividend:

I love dividend increases because they are proof that management is actually making more money, so can afford to pay us shareholders more. And an accelerating payout is a flat out cry for help!

Any management team that raises its dividend faster and faster is clearly making more money than it knows what to do with. This usually happens when it achieves a tipping point where its machine no longer requires as much reinvestment to continue growing. So leadership says: “Please, take a bigger raise, shareholders.”

Meanwhile investors and money managers who spot dividend accelerators lose their minds because, in theory, there is no valuation too high for a company that is increasing its dividend at an accelerating rate. Their spreadsheets literally break, and they buy the stock in a frenzy.

Ed’s stock should be owned by any serious dividend investor for three simple reasons:

- It’s recession-proof.

- It yields a fat (and secure) 7.5%.

- Its dividend increases are actually accelerating.

These two REITs are both “best buys” in my 8% No Withdrawal Portfolio – an 8% dividend paying portfolio that lets retirees live on secure payouts alone. And they can even enjoy price upside to boot, thanks to the bargain prices they’re buying at.

Now, as active recommendations for my premium subscribers, it wouldn’t be fair to reveal their names here.

But I would like to send you a free copy of my latest special report, Recession Proof REITs: 2 Plays With 7.5%+ Yields and 25% Upside, with all the details.

It includes the names, tickers and exact buy advice on how to start profiting right now.

In short, it’s everything you need to know before you invest a single penny, and it’s yours at no cost whatsoever.

Recent Comments