“Brett, what do you think of SCHD?”

As soon as I heard the “C” I figured we were talking Schwab US Dividend Equity ETF (SCHD). (Your income strategist can typically “name that dividend ticker” in two beats!)

“Eh,” I replied, visibly struggling to string together a positive response to my AAII presentation attendee.

“SCHD owns some good names. A few,” I shrugged.

“It will generally keep you out of trouble.”

Safety is all the rage in 2022. Pain has been felt on both ends of the stock-and-bond spectrum.

Stocks are down because the Federal Reserve is tightening. Bonds, meanwhile, are supposed to balance the ship when stocks sink. They haven’t. Fixed income has been flogged, too, because rising interest rates have busted bond prices.

With bonds broken, vanilla investors are looking back at stocks and buying the safest stuff—like dividends. Did we call it or did we call it? In these pages on January 5, we looked ahead and shook our heads:

The 2022 edition of the stock market is probably going to be a mess. With the Federal Reserve pausing its money printing, we are likely to see “flights to safety” that will feature—believe it or not—our favorite dividend stocks.

Six months later, the dividend bandwagon is beginning to get crowded. Bloomberg notes that investors have an “income obsession” this year. They’ve put more money into SCHD than they have any other ETF this year.

Cute. Kinda smart. Better than a Bitcoin ETF, that is for sure!

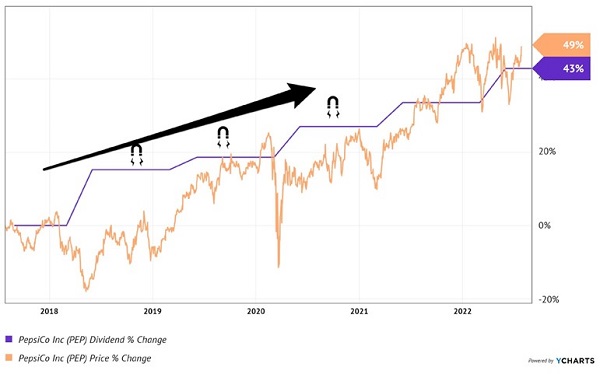

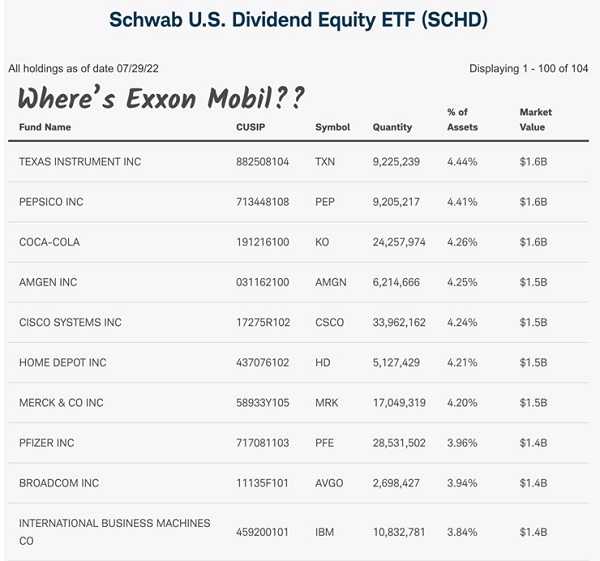

SCHD owns 104 dividend stocks and PepsiCo (PEP) is a top holding. PEP pays a piddly 2.6% but its yearly dividend growth is decent—not great but not AT&T (T) awful, either. These raises are the stock’s sugary “dividend magnet” that drives its price higher:

Decent Dividend Growth from Sugar Water

The 104-stock blend gives SCHD investors a 3.3% dividend. Again, not bad. But there’s a key ingredient missing from this ETF:

104 Dividend Stocks and No Exxon Mobil?

We talk about Exxon Mobil (XOM) often in this column because, well, it’s probably the blue-chip dividend stock to own in the 2020s. After all:

- It’s a bull market in oil.

- It’s a bear market in everything else (with the lone exception of the US dollar.)

- So how could we not own energy dividend stocks?

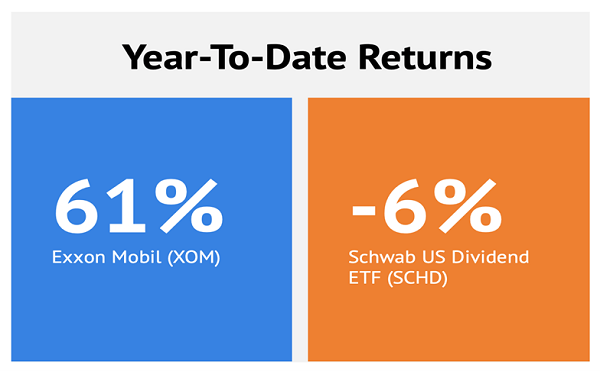

Yet SCHD does not, and its performance year-to-date has suffered as a result! While XOM has sailed 61%, SCHD has sunk 6%:

Oil is dirty and it produces carbon, but we need it to build clean energy infrastructure.

Someday, XOM’s current business model will be obsolete. Between now and then, the firm is going to make a boatload of money—and pay it to us!

The stock trades around $97 as I write. The company earned $4.14 per share last quarter. Last quarter!

Annualize this number, and XOM has a P/E (price-to-earnings) ratio less than six. Don’t annualize it, and we’re near 10. Either way, this is a dirt-cheap growth stock.

Quarterly revenue is up more than 40% year-over-year. EPS (earnings per share) has nearly tripled since last summer. Yet the stock still yields 3.6% and trades impossibly cheap.

The “Crash ‘n Rally” party is just getting going. Soon, the vanilla crowd will begin scooping a healthy side of XOM. This is the dividend flavor of the decade. If you already own it, well done. Enjoy!

If not, well, don’t waste another minute preparing for the inflation retirement storm that is soaking most portfolios. Let’s make sure we protect yours with more payers like XOM. Please click here to get started.

Recent Comments