If you’re worried that stocks are expensive, well, they are. The current bull market is making a run at history. But it’s also costly to stay in cash (and lock in zero income). Fortunately, it’s possible to buy some downside protection with yield (hint: think recession-proof REITs – real estate investment trusts).

I understand the “I’m worried so I’m sitting in cash” concern. And I know many investors who continue to sit on their money and hope for a big pullback. But wouldn’t it be nicer to bank 32% total returns with 8%, 9% or even 10% or more of it coming as dividends?

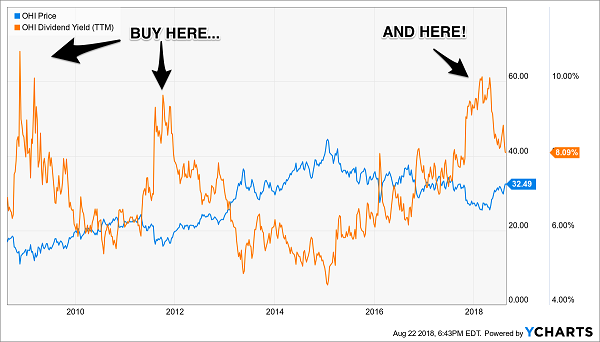

My Contrarian Income Report subscribers who smartly stayed with Omega Healthcare Investors (OHI) – a big paying REIT – have done much better than their scared cash hoarder friends, as well as the broader market in general. The year actually started inauspiciously as OHI announced a dividend “freeze.” The stock slipped. But a freeze isn’t the same as a cut – and OHI’s payout was well covered by its funds from operations (“FFO” – more on why this matters shortly).

The misunderstanding would soon be our gain, as the stock yielded 10% (thanks to years of previous dividend hikes). And anytime that OHI has paid double-digits in the past, it marked a major bottom for the stock. So why would this time be any different?

OHI’s Dividend Limits Its Price Downside

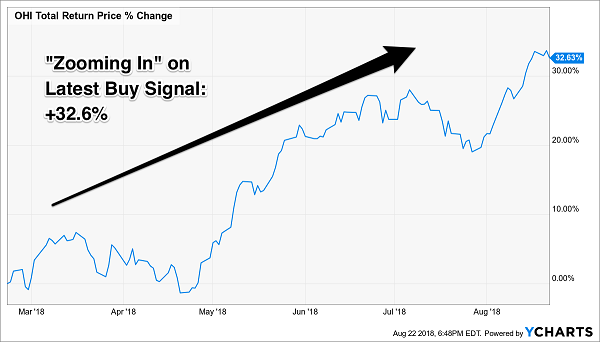

Let’s “zoom in” to see how OHI rallied off its most recent double-digit high to return 32% including dividends!

Better Than Cash – A Big Yield with Upside

Secure REIT yields are the truly the “rubber duckies” of the investing world. Mr. Market can push them underwater for a period of time, but eventually, they rocket up to the surface.

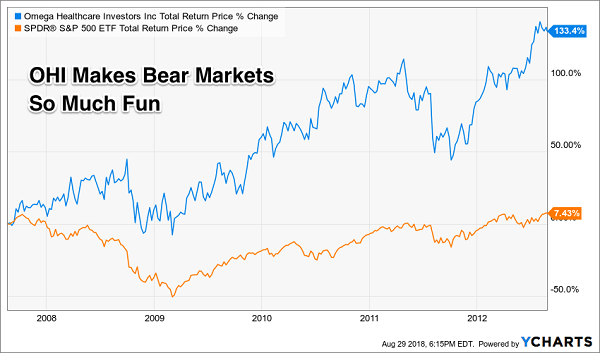

Let’s watch this in action at OHI over and over for fun and profit. We’ll rewind 11 years to the top of the last extended bull market. If you were savvy enough to time the top in 2007, you would still have been doing yourself a disservice by selling your OHI shares (not least, how would know when to have “gotten back in?”)!

This Dividend Payer Barely Went Below the Water

Five years later, as the S&P 500 barely recovered its crash losses, OHI investors had enjoyed 133% returns (including steady, fat payouts throughout). And while the presence of a dividend does not guarantee protection from losses, examples like this one show that payout-focused investors have a serious edge in the markets because:

Buying REIT stocks for their dividends alone makes day-to-day price action irrelevant.

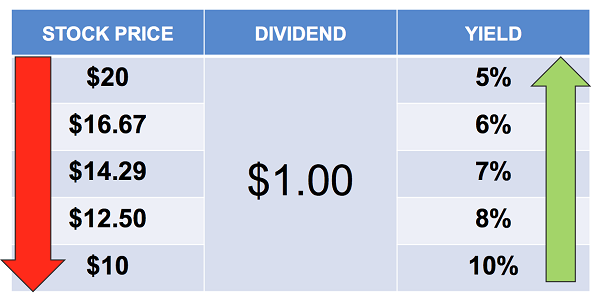

Here’s why. A falling price attracts more dividend buyers. Let’s take a $20 stock with a $1 dividend (a 5% yield) that begins falling in price. As it drops, income investors buy it because they are now able to secure more dividend for their initial dollar:

Which means REIT investors need not concern themselves with short-term price action. They only need to consider if the underlying payout is safe.

And how do we know if a dividend is secure? We simply follow the money.

Funds From Operations (FFO) is the Cash Flow That Matters

FFO represents the amount of cash a REIT actually generates from its operations. It’s where our dividend originates – which makes it the building block for everything else in the REIT-world.

To calculate FFO, we start with net income. Then we add back depreciation and amortization (which are accounting expenses) and subtract profits from property sales (which are one-time events).

REITs are required to pay most of their earnings back to shareholders as dividends – but those are just paper profits. FFO represents the actual rent checks that can be shoveled back to shareholders as dividends.

Obviously, we want to see FFO per share in excess of the dividend per share. If it’s not, it means the dividend isn’t really “covered” and management is funding the payout with borrowed money. Potential danger ahead.

I generally look for dividend-to-FFO payout ratios below 80% for REITs I recommend. Again, every firm is different, and some can get away with a higher percentage than others. Pay attention to management; most competent teams will say what their target ratio is. Note this and hold them to it.

Declining ratios are often a good sign, because they indicate rising FFO. They’re often a precursor to dividend increases. And if there’s anything more bear-market-proof than a safe dividend, it’s one that’s moving even higher!

My Top 2 REIT Buys: Recession and Rate-Proof Landlords for 7.5%+ Yields with 25% Upside

My two favorite REITs today are comfortably positioned in recession-proof industries. They’ll have no problem continuing to raise their rents – and reward their shareholders – no matter what the Fed decides at its next meeting, what President Trump tweets or when the stock market finally takes a breather.

My favorite commercial real estate lender lets us play Monopoly from the convenience of our brokerage accounts. They do all the legwork, building a secure, diversified loan portfolio featuring offices, retail space, hotels and multifamily units.

Management then collects the monthly payments, deposits the checks, and then it sends most of the profits our way as dividends (a legal requirement to have REIT status).

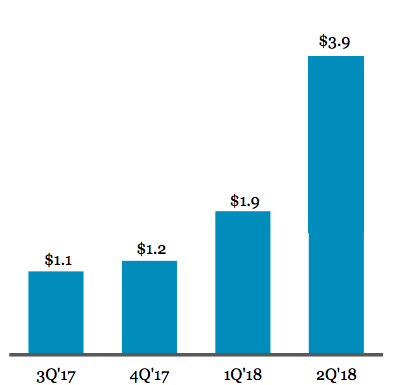

The stock’s current dividend (a 7.7% yield today) is covered by earnings-per-share (EPS) today. And don’t be fooled by the stagnant dividend (not that stability is bad). The firm continues to originate an increasing number of loans:

Quarterly Origination Volume ($ in Billions)

This firm is a conservative lender with perfect loan performance (100%). Its growing portfolio will drive higher profits, which in turn will inspire the next dividend hike. The best time to buy the stock is right now, while it makes the investments which will drive its payout and share price higher from here.

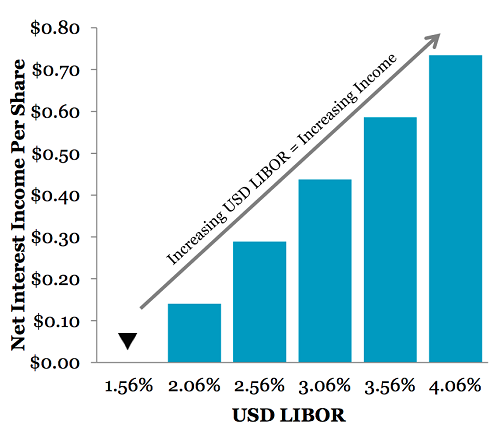

Plus, this firm has also smartly eliminated interest rate risk because it uses floating rates. In fact, it’s actually set up to make more money as interest rates move higher:

More Income as Interest Rates Rise

Same for another REIT favorite of mine, a 7.5% payer backed by an unstoppable demographic trend that will deliver growing dividends for the next 30 years. Interest rates are no problem for this landlord because it will simply continue raising the rents on its “must have” facilities.

Its founder Ed admitted that, fourteen years ago, he had “zero assets, a dream, and a business plan.”

Well, his dream and plan were plenty – the visionary entrepreneur parlayed them into $6.7+ billion in assets!

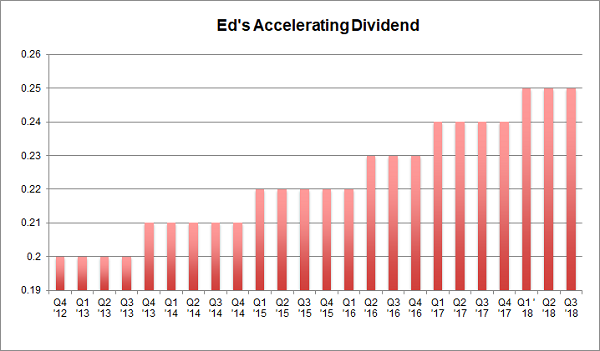

And right now is the best time yet to “bet on Ed” because his growing base of assets is generating higher and higher cash flows, powering an accelerating dividend:

I love dividend increases because they are proof that management is actually making more money, so it can afford to pay us shareholders more. And an accelerating payout is a flat-out cry for help!

Any management team that raises its dividend faster and faster is clearly making more money than it knows what to do with. This usually happens when it achieves a tipping point where its machine no longer requires as much reinvestment to continue growing. So, leadership says: “Please, take a bigger raise, shareholders.”

Meanwhile, investors and money managers who spot dividend accelerators lose their minds because, in theory, there is no valuation too high for a company that is increasing its dividend at an accelerating rate. Their spreadsheets literally break, and they buy the stock in a frenzy (after we already own it, of course).

Ed’s stock should be owned by any serious dividend investor for three simple reasons:

- It’s recession-proof.

- It yields a fat (and secure) 7.5%.

- Its dividend increases are actually accelerating.

These two REITs are both “best buys” in my 8% No Withdrawal Portfolio – an 8% dividend paying portfolio that lets retirees live on secure payouts alone. Now, as active recommendations for my premium subscribers, it wouldn’t be fair to reveal their names here.

But I would like to send you a free copy of my latest special report, Recession Proof REITs: 2 Plays With 7.5%+ Yields and 25% Upside, with all the details.

It includes the names, tickers and exact buy advice on how to start profiting right now.

In short, it’s everything you need to know before you invest a single penny, and it’s yours at no cost whatsoever. Click here and I’ll share how you can get a complimentary copy of my premium REIT research.

Recent Comments