Is the 60/40 (stock/bond) portfolio now 100/0 in favor of stocks?

That’s been the subject of several financial headlines lately. The authors are suggesting that the traditional mix of 60% large-cap stocks and 40% safe bonds won’t generate enough money for us to retire on unless we’ve got a cool $10 million or so. And, they’ve got a point, with the S&P paying less than 2% and US Treasuries yielding under 1%.

But even a 100/0 portfolio won’t help you too much. Put it all in the popular SPY ETF, and we’re still under 2%! Plus, this “heart attack kid” can fluctuate by 1% or even 2% per day. Too much volatility, not enough income.

But, rather than “pull the plug” on the 40% of bonds contained in a traditional 60/40 retirement portfolio, we contrarian-minded income seekers can simply rearrange the holdings to give us a mix that is:

- 53% stocks (and equity funds),

- 47% bonds (and fixed-income funds), with a

- 7.2% average dividend yield.

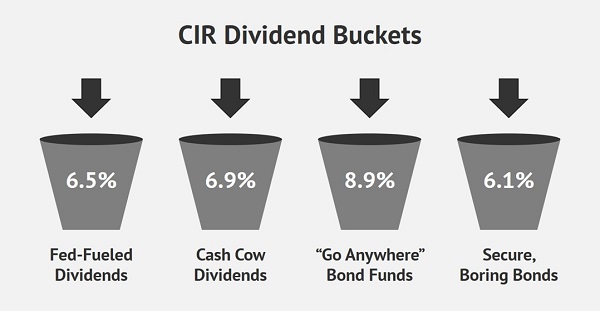

If this looks familiar, it’s because this is the current configuration of our Contrarian Income Report portfolio. Our CIR portfolio is split up into four buckets:

- Fed-Fueled Dividends yielding 6.5% (with serious near-term upside),

- Cash Cow Dividends paying 6.9% (multi-year stock holdings),

- “Go Anywhere” Bond Funds dishing 8.9% (multi-year bond positions), and

- Secure, Boring Bonds dealing 6.1% (to buy and hold almost forever).

Who is this portfolio designed for? Anyone who wants their current or upcoming retirement funded by dividend payments.

What if we’re planning to retire in five years, ten years, or more? With current “active” income coming in, we may not need 7.2% yields. At least not yet.

For my fellow young bucks out there, consider a “higher octane” dividend growth focused portfolio that emphasizes capital appreciation tomorrow over yield today. This is where the 100/0 portfolio may make sense. After all, if you don’t need the dividend payments today (but you enjoy counting them and the safety they provide) then go ahead and try to become as wealthy as you can by buying dividends that could pop 21% or better in 2021, for example.

The big dividends are important for those of us nearing or in retirement. Generous yields help us turn our nest egg into cash flow without turning our backs on a harmonic blend of stocks and bonds.

Which sounds great, but you’re probably wondering: Brett, where the heck did we find secure yields this generous in today’s zero-point-nothing world?

We find these dividends in two places. Let’s begin with fixed income.

How to Buy Secure Bonds That Pay Up to 8.9%

First, instead of buying our bonds via popular E-T-Fs, we are buying C-E-Fs (closed-end funds). They provide us with three key advantages:

- Higher current yields,

- Cheaper valuations, and

- More upside

CEFs have fixed pools of shares, so they can (and do) trade higher and lower their NAVs, or “fair” values. As contrarians we can step in when they are temporarily out-of-favor, such as after a pullback when liquidity is low, and buy them at generous discounts.

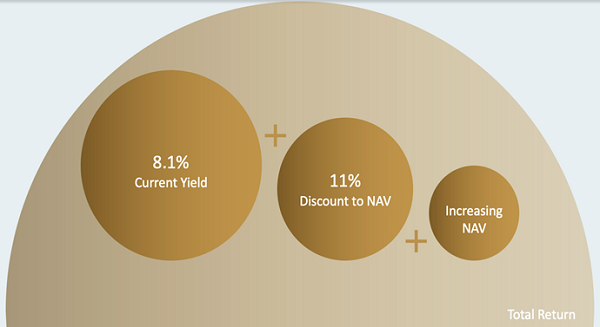

For example, the Western Asset Emerging Markets Debt Fund (EMD) is likely to benefit from a declining dollar. It offers three ways to profit:

- Its 8.1% yield,

- The fund’s 11% discount to NAV, and

- The likelihood that its NAV will get a boost in dollar terms as our greenback declines.

3 Ways to Double-Digit Total Returns with EMD

EMD’s bonds are also going to be increasingly popular as interest rates stay anchored to zero for years to come. For example, the fund owns secure government bonds paying 8.75% issued by a nation with a debt-to-GDP ratio of just 27%. (By comparison, we had a triple-digit debt ratio here in America before our 2020 mess.)

The nation is Peru. The country was a financial train wreck in the 1970s and ‘80s, so investors still demand high coupons (memory is long for investors in South America, prone to debt debacles such as in Argentina!). And it’s much easier to buy these bonds than to hike Machu Picchu. We can get them at an 11% discount from the convenience of our own computers by typing in E-M-D.

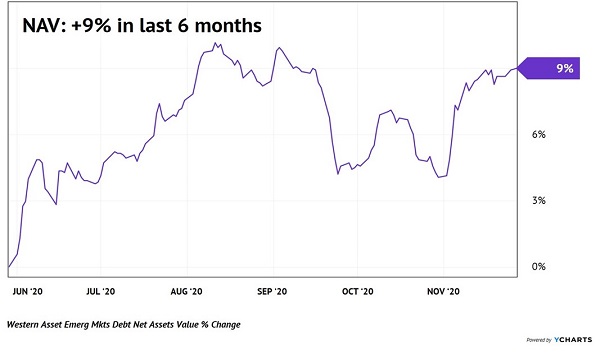

Other investors are beginning to figure this out. Over the last six months, EMD’s NAV (the value of the bonds it owns) has increased by 9%:

EMD’s Portfolio: +9% in Six Months

These NAV gains are net of EMD’s monthly distributions. When we add together the fund’s:

- Higher NAV,

- Monthly payouts, and

- Narrowing discount window,

We see that investors have enjoyed 16% returns over the past six months. That’s excellent for a bond fund. And this gravy train is likely to keep rolling, thanks to the greenback falling out of bed.

When there are returns like these to be had in Bondland, why would we even bother considering stocks? Because believe it or not, there are even better opportunities on the board!

How to Buy Secure Stocks Yielding Up to 6.9%

With the bull market still in effect, equities are likely to continue outperforming bonds. (Yes, as mentioned, we can do even better than 16% gains in six months we achieved with EMD, if we buy stocks smartly.)

But we needn’t throw away our dividends in hopes of keeping up with the bull. We contrarians recently employed a discount mechanism to purchase shares for just $0.84 on the dollar.

This strategy is an ode to my mom, who—to this day—refuses to pay the sticker price. If there’s a coupon to be found, she’ll find it.

We recently discussed the Gabelli Dividend & Income Trust (GDV), managed by legendary value investor Mario Gabelli, as a top-notch CEF. In late September, we spotted a rare opportunity to buy Mario’s portfolio for just 84 cents on the dollar (thanks to its then-16% discount to net asset value, or NAV).

GDV holds blue-chip dividend payers and growers such as Mastercard (MA), Microsoft (MSFT) and JPMorgan (JPM). These high-quality stocks wouldn’t normally qualify for our CIR portfolio because everyone in the world knows they are great shares to own. Even though these companies are constantly raising their dividends, constant demand for their shares keeps their prices high and current yields low. So, they never meet our current yield requirement.

GDV gave us a way to have our dividend and enjoy some additional upside in these high-quality dividend shares too. The fund pays a monthly dividend that adds up to a sweet 6.3% annual yield.

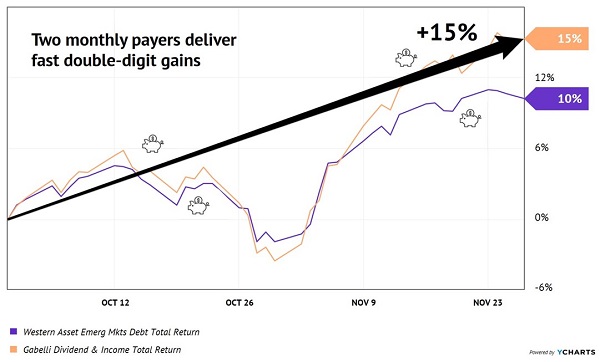

Since we had that conversation, GDV has rocketed 15% higher in just two months. We hope you followed our official CIR recommendation to purchase shares. If so, you’ve received two monthly dividends already!

Even Better Than EMD: 15% Gains in Two Months!

If you don’t yet own GDV, I would wait to add new money. Shares still trade at a generous 14% discount to NAV, and yield 6.3%, so there’s no reason to sell them. But with investor sentiment a bit greedy at the moment, a pullback in the broader markets could present an even more compelling opportunity.

If you’re looking to turn your nest egg’s “pile of cash” into a 7.2% yielding machine that you can actually retire on, these are the types of investments that you should consider. As you can see, when we get the timing of these purchases right, they really do present us with the “perfect income portfolio.”

I don’t use that term lightly. To qualify as a perfect income investment, a bond or stock fund must:

- Provide us with 200%, 300% or even 400% the income of a “lame” mainstream ETF,

- Give us a real shot at legitimate upside (16% in six months, 15% in two months for example), and

- Demonstrate the appropriate safety for a retirement investment.

It’s the best way I know to crisis-proof a retirement nest egg. And it doesn’t require any options trading or penny stock slinging. To receive my number one income investing secret to invest in right now, click here.

Recent Comments