Exchange-traded funds (ETFs) shattered growth records in 2017, with inflows topping $464 billion last year. The global ETF market now boasts more than $4.5 trillion in assets, and a large part of the appeal has been driven by dirt-cheap fees.

But many of these fund’s fees are “cheap for a reason.” We’ll talk about five today that lure investors in with appealing current yields – but then proceed to dump their dumb money out the back door.

These five funds may have sweet dividend yields, but they have produced sour total return results thanks to one fundamental flaw or another.

ETRACS Linked to the Wells Fargo Business Development Company Index ETN (BDCS)

Dividend Yield: 8.7%

One of the most basic appeals of the exchange-traded fund is the cheap diversification they provide. For just a few basis points, you can have a basket of funds that express any sort of market bet you want to make – income, growth, sector-specific, international.

However, that asset can become a detriment in the event that you’re betting on a troubled area of the market with several bad players. And business development companies (BDCs) certainly apply.

BDCs, which provide financing to small- and midsize companies, are similar to real estate investment trusts (REITs) in that they’re required to pay out 90% or more of their income as dividends to shareholders, and typically deliver high yields as a result. However, this field is rife with competition and interest-rate risk, which has led the ETRACS Linked to the Wells Fargo Business Development Company Index ETN (BDCS) to underperform the broader market since its inception despite its massive dividend yield.

While there are a few good players in the space, the fund is most heavily weighted in larger BDCs such as Ares Capital (ARCC) and Prospect Capital (PSEC) – and their lackluster performance has drowned out some of the smaller winners.

So while it often pays to diversify, BDCs and the BDCS ETF is an example of an unhappy exception.

Horizons Nasdaq 100 Covered Call ETF (QYLD)

Dividend Yield: 7.2%

What would you say if I told you there was a fund that allowed you to participate in the upside of the tech-heavy Nasdaq-100, while also enjoying defense and a 7%-plus yield? Chances are you’d jump all over it.

But while the Horizons Nasdaq 100 Covered Call ETF (QYLD) sounds great at a glance, the devil is in the details.

The QYLD is one of my favorite examples of how basic indexing isn’t always the superior strategy – and that sometimes, it really pays to have active management.

In this case, the ETF is trying to put the well-worn income-generation tactic of selling covered calls to work for investors, holding the Nasdaq-100 and trading options against it. This strategy allows investors to enjoy some of the Nasdaq’s upside, but also fall back on income when the index is flat or declines.

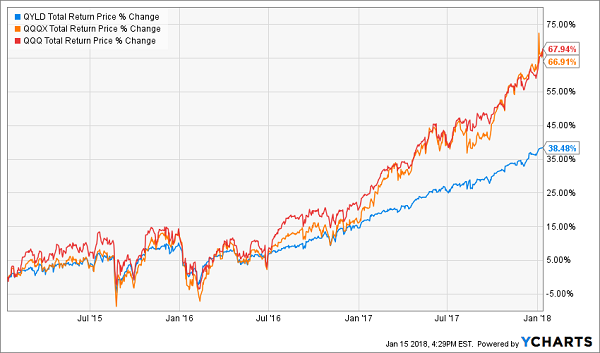

The problem? QYLD has a singular mandate to trade only front-month options, limiting its flexibility (and thus profitability), and only on the Nasdaq-100 index rather than its individual stocks (where it could reap better premiums). Thus, while you could expect this kind of strategy to somewhat underperform the PowerShares QQQ Trust (QQQ) Nasdaq-100 ETF in a roaring bull market, the QYLD is off by nearly half!

Meanwhile, the Nuveen Nasdaq 100 Dynamic Overwrite Fund (QQQX) – a similar but actively managed closed-end fund – charges higher fees, but has essentially matched the QQQ on its way through the clouds.

Horizons’ QYLD Isn’t Worth the Cost Savings

iShares U.S. Preferred Stock ETF (PFF)

Dividend Yield: 5.6%

In fact, there are a few other areas of the market where you can find significantly better performance by dishing out a few extra dollars every year.

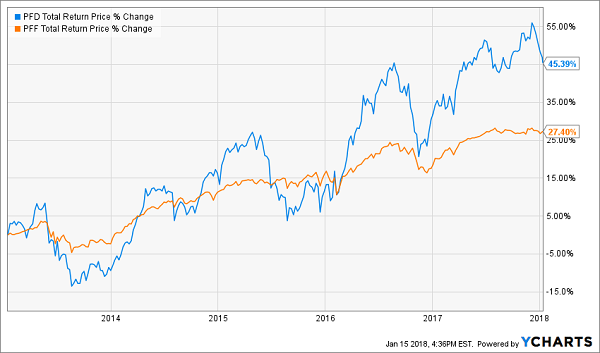

I shouldn’t criticize the iShares U.S. Preferred Stock ETF (PFF) too much. After all, it was a transformative product that helped bring preferred stocks – a stable source of income, but a more difficult asset to research and buy individually – into the mainstream because of its relatively low fees and easy accessibility.

That said, closed-end funds, with their ability to use leverage to amplify yield and returns, have proven to be a much better way to make a general bet on preferreds – even if they’re not even remotely as popular.

To wit, consider the Flaherty & Crumrine Preferred Income Fund (PFD), a closed-end fund that has just $163 million in assets under management at the moment. Why so unpopular? Well, the 1.34% expense ratio isn’t exactly appealing compared to 0.47% for the PFF, and there’s definitely a discrepancy in marketing spend between Flaherty and the PFF’s parent BlackRock (BLK).

However, investors who can handle a bit more volatility have been treated to far better gains that more than make up the expense ratio. That’s in large part thanks to management’s expertise in the preferreds space, as well as leverage of 30% currently that allows the fund to squeeze out more income.

iShares’ PFF Offers Basic Preferred Exposure, For Better or Worse

SPDR Barclays High Yield Bond ETF (JNK)

Dividend Yield: 5.6%

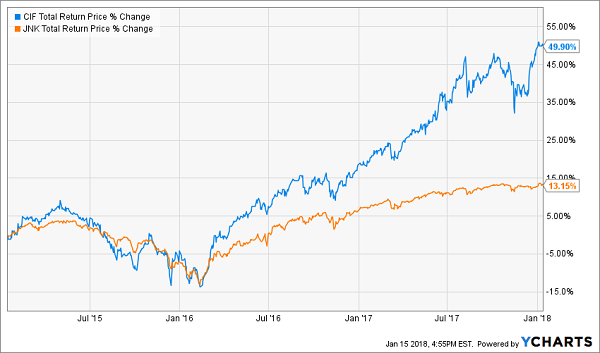

Count junk bonds in the same category as preferreds and covered calls: The most ubiquitous ETFs in the space offer cheap, adequate performance, but you can get far better from CEFs.

Consider the MFS Intermediate High Income Fund (CIF), which delivers an 8.9% yield – versus 5.6% for the popular SPDR Barclays High Yield Bond ETF (JNK) – on a portfolio whose credit risk is similar and boasts less than a year more in average effective maturity.

Once Again, Basic ETFs Aren’t Always Better

Also important to note is that closed-end fund shops can offer specialized exposure. In other words, you can get “plain Jane” junk exposure like you get with the CIF, or you can find funds with some international allocation, or even blends of junk debt and other assets.

Miller/Howard High Income Equity Fund (HIE)

Dividend Yield: 10.4%

Lesson learned, then: Closed-end funds are far superior to exchange-traded funds, right?

Not always.

Consider the Miller/Howard High Income Equity Fund (HIE) – a downright tempting CEF that delivers a double-digit yield by investing in a highly diversified portfolio of MLPs, REITs and mREITs, as well as solid high-yielding traditional equities such as AT&T (T), GlaxoSmithKline (GSK) and Royal Dutch Shell (RDS.B).

The fund aims to deliver high income and low volatility, but its portfolio selection – including its exposure to MLPs and REITs – has hurt the latter aim, as well as overall performance. But here, the ETF world shines. The PowerShares High Dividend Low Volatility Portfolio (SPHD) hardly blows the doors oft with its 3.1% yield, but its focus on more traditional equities has led to massive outperformance of 43% to negative 3% over the past three years. Also helping is a cheap 0.3% expense ratio, which at nearly 2 percentage points cheaper than HIE’s 2.24% fee, is a real difference-maker over time.

The real lesson to take away, then? CEFs can be superior to ETFs – but you can’t just pick names out of a hat.

Live Off Dividends Forever With This Secure 8% “Ultimate” Retirement Portfolio

High yields are the cornerstone of a comfortable retirement. A steady stream of substantial income will ensure you can pay the bills and stay afloat when you’ve stopped collecting a paycheck.

But if you want to get through retirement without ever touching your nest egg, you need more than just giant dividends – you need dividend growth to beat back inflation, and you need capital appreciation to keep building your nest egg! Losers like HIE can’t do that … but the “triple threat” stocks in my 8%-yielding “No Withdrawal” retirement portfolio sure can!

How often have you seen a pundit shill for OK-yielding blue chips like Coca-Cola or Kellogg? They’re not bad companies, but they leave you with just 3% to 4% in dividends, paltry payout hikes and little in the way of growth potential. You and I both know that math doesn’t add up. Those 3% to 4% returns on a nest egg of half a million dollars will only generate $20,000 in annual income from dividends at the high end!

You’ve worked your tail off for decades. So you deserve more out of your retirement.

My “No Withdrawal” portfolio ensures that you won’t have to settle during the most important years of your life. I’ve put together an all-star portfolio that allows you to collect an 8% yield, while growing your nest egg – an important aspect of retirement investing that most other strategies leave out.

I’ve spent most of the past few months digging into the high-dividend world, and I’ve had to weed out several yield traps that looked great on their surface, but potentially disastrous at a closer look. The result is an “ultimate” dividend portfolio that provides you with …

- No-doubt 6%, 7% even 8% yields – and in a couple of cases, double-digit dividends!

- The potential for 7% to 15% in annual capital gains

- Robust dividend growth that will keep up with (and beat) inflation

This all-star cluster of stocks features the very best of several high-income assets, from preferred stocks to REITs to closed-end funds and more, that combine for a yield of more than 8%.

This portfolio will let you live off dividend income alone without ever touching your nest egg. That means never having to worry about how you’ll pay your monthly bills, and never having to worry about wrecking your retirement account if disaster strikes.

Don’t scrape by on meager blue-chip returns and Social Security checks. You’ve worked too hard to settle when it matters most. Instead, invest intelligently and collect big, dependable dividend checks that will let you see the world and live in comfort for the rest of your post-career life.

Let me show you the path to the retirement you deserve. Click here and I’ll provide you with THREE special reports that show you how to build this “No Withdrawal” portfolio. You’ll get the names, tickers, buy prices and full analysis of their wealth-building potential – and it’s absolutely FREE!

Recent Comments