One mistake I’ve seen investors make time and time again is leaning too heavily on the latest “investment product” their bank is pitching them.

The problem arises because at the heart of the banking system lies a key conflict of interest: banks make money off fees and interest charged on investments, loans, credit cards and other products, so they’re motivated to get you to use those tools more.

But that usually lies at cross-purposes with our goal as income—and more specifically closed-end fund (CEF)—investors: to retire early on a high income stream (and ideally on our dividends alone), with no need for banks’ expensive loans and debts.

It’s no wonder the 500 or so CEFs out there, whose average yield clocks in north of 8% now (with dividends often paid monthly) never get bankers’ attention—and are never among the products they recommend to their clients!

Buyer beware doesn’t just extend to big banks’ retail products, by the way: even their investing advice needs a big disclaimer on it. Many bank execs and economists were bearish last year, including Morgan Stanley CIO Mike Wilson. Last year, he said the slowdown in economic growth, which would get worse, wasn’t fully priced in; thus he called for stocks to fall 10% in 2023.

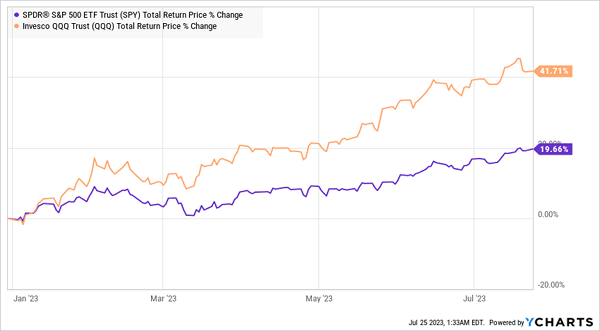

S&P 500 and NASDAQ Soar in ’23

Anyone who sold late last year has locked in their 2022 losses and missed out on a near-20% rebound in the S&P 500 this year (not to mention a near-42% return on the NASDAQ). And as studies have shown, once investors have sold out of the market, they often wait too long to buy back in—and miss out on more gains.

Be Your Own Bank With This 10% Yielder

Banks, at their core, have a simple operation: take in cash, have some available for customers when necessary, and lend the rest so they collect income that, in turn, provides their profits.

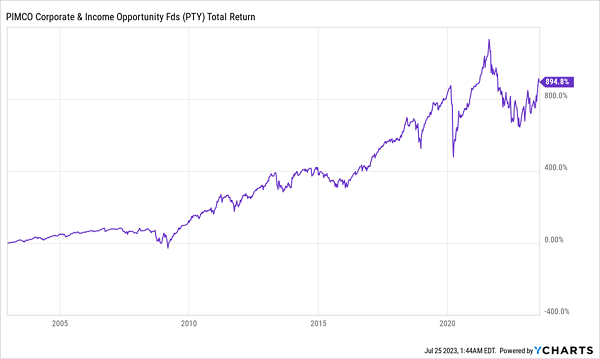

CEFs operate very much on the same principle. If you buy the PIMCO Corporate & Income Opportunity Fund (PTY) you’re very much buying into something like a bank.

PTY takes $2 billion of cash, makes 10% of it available to PTY shareholders, thanks to its 10% dividend yield that is paid out monthly, and uses the rest to lend money to companies of all stripes; even if you’ve never heard of PTY, you know the companies it lends to: Ford Motor Company, Verizon Media, and Carnival Corporation are just three of the 400+ debtors PTY has lent money to.

The “Bank of PTY” Wins

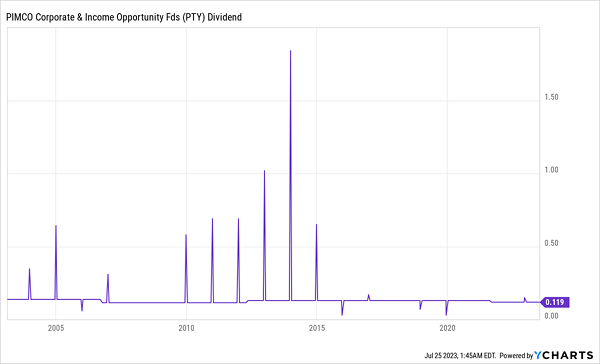

PTY has made a ton of wealth doing this; its 10% income stream is not only fully covered by current fund returns, it’s overcovered, which would most likely result in the big special dividends this fund gave out in the 2010s, causing PTY’s annualized yield to rise as high as 20%.

PTY Pays Out Big Special Dividends in Flush Years

Note too that the fund’s dividend payout has remained stable throughout, as well—although a lot of people say double-digit yields are unsustainable, PIMCO’s fund disproves that pretty easily. And since PTY is a CEF, you can buy or sell anytime stock exchanges are open.

In other words, with PTY you’re getting to be the bank and collect a double-digit yield with pretty much zero effort. Which makes the dividend checks, when they start coming in, feel almost magical.

5 More “Hidden” CEFs You’ll Never Hear About From Your Bank

As we just discussed, it’s easy to see why CEFs are ignored by banks and advisors: once folks discover the rich 8%+ yields (often paid monthly) on offer with CEFs, they’ll never buy an ETF or a bank-sponsored financial “product” again!

Luckily, we CEF investors know better. We’ve taken advantage of the 2022 pullback to bulk up our portfolios, locking in 10%+ CEF income streams and setting ourselves up for double-digit price gains, too.

You’re not too late to grab these deals: because CEF investors tend to move a bit more slowly than stock buyers, our buy window is still open. To help you take advantage, I’ve pulled together our 5 top “bank-beating” CEFs yielding 10.2% on average to buy now in a new Special Report I want to give you now.

Recent Comments