Let’s book these 104% profits today.

We’ll sell this winner and then consider a 9.3% dividend that could really soar in 2023. It couldn’t be any cheaper, either—this high-quality fund is trading at a 17% discount to fair value!

But wait, there’s more in the bargain bin. I’ll also share a 5.9% payer that is, likewise, trading for just 83 cents on the dollar—also 17% off!

More on these incredibly cheap dividends in a moment. First, the winner.

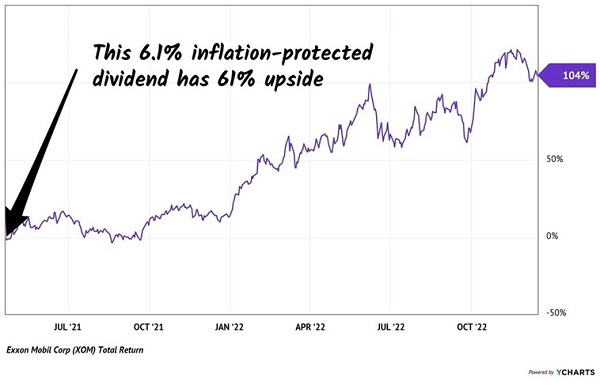

Remember when we “pounded the table” on Exxon Mobil (XOM) in April 2021? We were right. The then-6.1% payer was too cheap!

The only thing we missed was the upside target. We penciled in 61%. In reality, XOM delivered 104% total returns.

Believe it or not, energy stocks were broadly loathed when we flipped bullish on Exxon in April 2021. Mainstream investors thought XOM’s dividend was in danger of a spill. But we knew better than to accept this “common knowledge” at face value.

XOM’s 104% Run Since April 2021 “Plea to Buy”

Purchasing out-of-favor stocks rarely feels good in the moment. There’s pressure to run with the investing herd—it feels safer. But we know the real profits are made by running away from popular opinion.

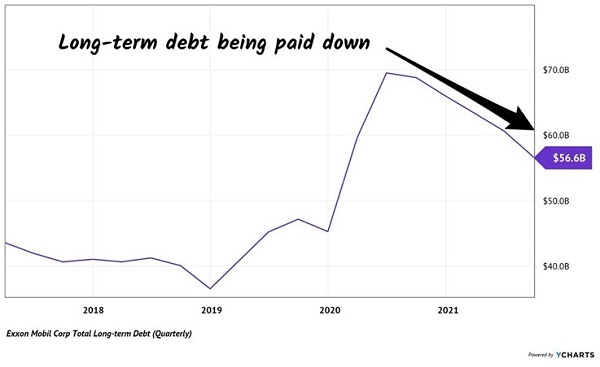

“Basic” dividend investors believed XOM’s payout was at risk. Activist investors were grabbing Board seats, and XOM’s debt ballooned since early 2019. At a glance, the company appeared to borrow cash to pay its dividends. Never a good look!

For a few quarters, it was. But our “second-level” research revealed that a multi-year bottom was likely in for XOM shares and its dividend was safe. We had two reasons to be confident:

- Oil prices were starting to rally. We reasoned they would continue to climb as the black goo traced its usual “Crash ‘n Rally” pattern. And that is exactly what happened. Higher energy prices since then have boosted XOM’s profits.

- Thanks to improved cash flow, XOM began paying down long-term debt. This was a strong sign the dividend was safe.

How We Knew XOM’s Dividend Was Secure

Firms like XOM will do anything to avoid cutting their dividend—including taking on debt to make their payments. And yes, management went to the debt well for a few quarters when oil prices collapsed. But a quick rebound in Texas tea prices would save the day and quickly reverse the need for XOM to borrow.

Declining debt was a strong sign that the worst was over. If the company had enough cash to run its business and beyond that to pay down debt, fund the dividend and buy back shares, it’s a coiled spring!

This would soon be reflected in XOM’s share price. The stock market rewards investors like us who place our wagers before an outcome is obvious to the rest of the world. This is why contrarian investing can be so profitable—because we buy before the fog completely clears. (If we run with the herd, we split the smaller profits with it!)

So why book the gain? I’m still wildly bullish on energy long term, right?

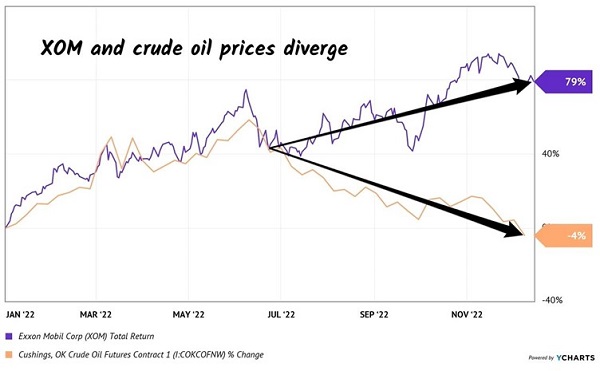

I am. But I’m picking on XOM because it is levitating higher in the face of lower crude oil prices. Check out the performance of XOM (+79%) versus Texas tea (-4%) prices year-to-date:

XOM Soars Even While Crude Sinks

XOM has been the “hot hand” of the pair. It may cool off, for two reasons:

- XOM’s yield is down to 3.5% (a “side effect” of a soaring stock price).

- Energy stocks are really popular now (they were hated in April 2021).

If you’re sitting on these 104% profits from our April 2021 call, this is a nice time to book them.

“But Brett!” I can hear you now, my thoughtful contrarian. “China is going to reopen. XOM is buying back $50 billion in stock. Don’t we still want energy exposure?!”

Yeah, we do. And as second-level thinkers, we’re going to demand a discount. Plus a bigger dividend! Which is why we’re considering the cheapest closed-end funds (CEFs) on the planet.

We love CEFs because they:

- Pay big dividends.

- Often fall into the bargain bin.

When markets drop, as they have for the entire year, CEFs drop with a thud. Investors who own them panic and sell at any price—even as low as 83 cents on the dollar!

Professional investors, meanwhile, can’t scoop up these bargains as fast as we can. Anyone with millions and millions of dollars to deploy will typically put cash to work in the big, liquid S&P 500.

We’re nimbler cuz we’re smaller. We can buy the cheapest funds on the planet for dimes on the dollar.

Take MainStay CBRE Global Infrastructure Megatrends Fund (MEGI), which yields 9.3%. Yes, 9.3%.

A fly-by-night fund? Hardly. MEGI owns some of our favorite energy dividends. Contrarian Income Report readers will recognize ONEOK (OKE) and The Williams Companies (WMB) and smile.

(These two energy blue chips are up 168% and 89% respectively in our CIR portfolio!)

Launching before a bear market means MEGI’s track record was in early trouble, which is why it didn’t show up on any self-respecting screener. And that stealth is also why it trades at a 17% discount to its net asset value (NAV).

Take PIMCO Energy & Tactical Credit Opps (NRGX), a perfect way to play the pullback in energy. NRGX owns a blended basket of income-producing stocks and bonds that benefit from high energy prices.

Please note that I said high, not higher. This is important because energy is likely to stay elevated in its continuing multi-year “crash ‘n rally pattern”:

- First, the price of oil crashes (see, March and April 2020).

- Next, energy producers scramble to cut costs. They slash production.

- The economy recovers because it always does. Energy demand picks up.

- Then, there is not enough supply! So, the price of oil begins to climb.

- Because it takes many years to explore and drill, supply lags demand for a long time. The price stays elevated.

We’ve got years here—perhaps the rest of the 2020s—for energy supply to remain tight. Even a light recession won’t derail this bull.

We have many ways to win with a CEF as heavily discounted as NRGX:

- Collect its secure 5.9% dividend, fueled by high energy prices.

- Enjoy rising NAV over time.

- Make money while/when the discount window narrows from 17%.

As the energy bull market rolls along, CEFs in this sector could eventually flip to premiums. Sounds crazy until we consider that many PIMCO funds trade for more than the value of their underlying assets. PIMCO CA Municipal Income (PCQ) commands a 51% “gratuity” as I write. (My high-earning neighbors are paying $1.51 for $1 of California munis—the cost of tax relief in a high tax state!)

We’re not interested in paying $1.51 for $1 in income. “Eighty-three cents” sounds better. Plus, we’re catching energy on a dip.

I get it—energy plays like XOM, MEGI and NRGX fly in the face of “tried and true” Wall Street advice. But the suits on Wall Street have ruined many perfectly good retirement portfolios this year with their lazy recommendation of a “safe” 60/40 mix of stocks and bonds.

This money advice was exposed as broken this year when stocks and bonds both crashed.

A better bet? Retire on dividends alone with a “No Withdrawal” Retirement Strategy.

Recent Comments