Income investors are typically a conservative and prudent bunch. Focused on a sustainable income stream, they often look for a sign to avoid a big price drop.

So when it comes to one of the highest-yielding investments of all—closed-end funds (CEFs)—how can you know when the time has come to sell?

I’ll tackle that question with a 1-2-3 approach to CEFs that will help you avoid the kinds of value traps that promise big dividends but really deliver big losses.

Sell Signs Not Always Easy to Spot

First off, it’s easier to know when to buy than when to sell. If the fund is well managed, has a strong track record, is deeply discounted and has a relatively safe dividend, it’s generally a screaming buy. Signs to sell aren’t always so obvious, but they’re still there. You just need to know what to look for.

With that in mind, here are three key points to consider when deciding whether to sell a CEF.

No. 1: The Discount Is Too Small

The first clue that it’s time to sell is the most obvious: when the fund is overbought, it’s time to dump it.

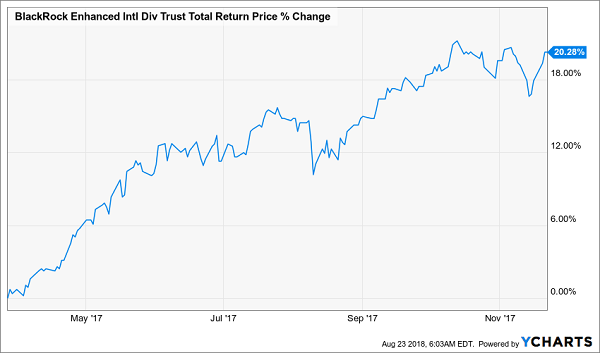

For instance, take the BlackRock Enhanced International Dividend Trust (BGY), which I recommended to CEF Insider readers in March 2017. I chose BGY at that time because its discount had suddenly widened, despite the fact that changes in its portfolio indicated it was well positioned to surge.

The fund did this over the following eight months:

A Fast 20% Return

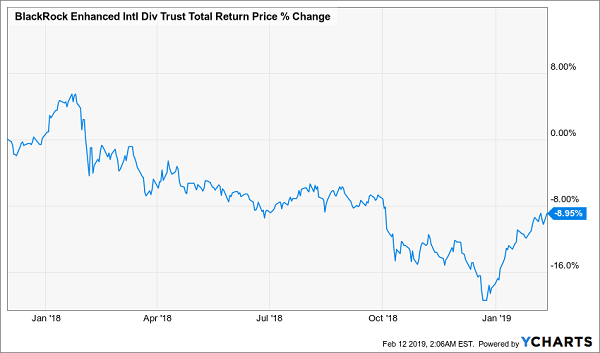

A big reason for this return: BGY’s unusually large discount of 12% in March steadily closed to a more normal 6.7% in November, when I urged subscribers to sell. After my sell call, the fund did this:

A Steady Drop

The lesson? Keep track of the discount, and when it gets too narrow (or becomes a premium) relative to its historic average, it’s time to get out of this crowded trade.

No. 2: Pressure on an Entire Sector

Sometimes some outside force will pressure the type of assets the fund invests in. When this happens, sell as fast as possible.

The great thing about CEFs is that, in large part because of their small size and retail-investor base, they react more slowly and over a longer period to bad news than more popular ETFs. This means that anyone who keeps up with the news and uses CEFs has more leeway to respond to the market and sell.

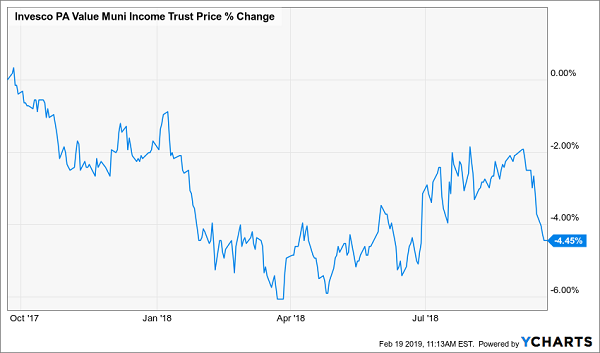

A clear example of this happened with a municipal-bond fund in late 2017: the Invesco PA Value Municipal Income Trust (VPV).

I recommended this fund to CEF Insider members in March 2017 for familiar reasons: a great and reliable dividend yield, strong management and an unusually big discount. And the fund delivered over the next few months, outperforming the municipal-bond index ETF that tracks VPV’s benchmark:

Cheap VPV Beats the “Dumb” Index Fund

Then a major news event happened in September that prompted me to release a sell alert: S&P Global Ratings downgraded Pennsylvania’s bonds, and the state did not immediately respond to the market’s concerns.

The combination of a downgrade and lawmakers’ refusal to address it was a crystal-clear sell signal. VPV did this in the year after we unloaded it:

VPV Plunges

This is a big move for a municipal-bond fund, and all it took to dodge this hit was to follow the news and react in a timely way.

No. 3: Get Defensive in a Bear Market

My third point is something that hasn’t yet happened since we launched CEF Insider, although I do believe it is a couple years away: a recession and bear market.

Every investor hopes to avoid plunges like 2008/09. No one can steer clear of losses all the time, of course, but it is possible to defend your portfolio while continuing to collect the 7%+ dividend streams our CEF Insider picks hand us.

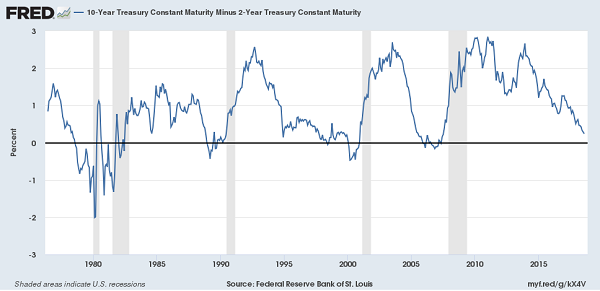

The key is to keep a watchful eye for four economic warning signs: rising unemployment, slower wage growth, weaker consumer spending, and, above all, the so-called “inverted yield curve.” That’s when the spread between 2-year and 10-year Treasury yields goes negative; in the past, it’s correctly indicated a recession within the following 12 months.

Below the Black Line Means Danger Ahead

The financial press has spilled a lot of ink about the inverted yield curve recently, because in the last year it’s tanked to its lowest point since just before the 2008/09 meltdown.

But we haven’t seen an inverted yield curve yet. When we do, it’s time to emphasize defensive CEF sectors, especially if the inversion is accompanied by rising unemployment and falling wages. The appearance of an inverted yield curve is also a good time to prune weaker CEFs from your holdings, such as those with flaws like the ones I showed you in points 1 and 2.

Fortunately, we’re not in this situation now: incomes are going up at an accelerating pace and unemployment remains below 4%. But I’ll keep a close eye on all the vital economic numbers and keep you updated (including giving you clear instructions on how to respond) in CEF Insider.

4 “Set-It-and-Forget-It” CEFs for Big Gains (and 7.5%+ Payouts)

With the market rebounding and CEF discounts evaporating, I’ve pushed out a freshly updated list of CEFs you need to buy now—while they’re still cheap!

And no, you won’t have to hover over these 4 funds, wondering when to sell, because all 4 are perfect picks to buy and hold for a decade (or more). And they boast ridiculously wide markdowns now, priming us for big upside in the next 12 months alone.

But even if the market takes a tumble, these crazy discounts have us covered, because they mean these 4 ironclad CEFs will dig in and hold their own in the storm.

The best part: these 4 buys pay an average dividend of 7.5%, with one even sending an incredible 8.4% cash payout your way!

So right now you’re probably wondering why these 4 CEFs are available so cheap.

The main reason: these CEFs are small, with market caps below $1 billion, and that keeps them off the herd’s radar, giving us more time to buy in as the bulls stampede.

But we don’t have forever, and I don’t want you to miss out. Click here now to get full details on these 4 bargain funds: names, tickers and everything I have on each one—all boiled down into clear, easy-to-read English.

Recent Comments