With over 500 closed-end funds (CEFs) on the market, how do you choose the best one?

It’s not an easy question to answer, because there are literally dozens of metrics any CEF investor should look at before buying.

Luckily, I’ve found a way to boil those down for you. In a moment, I’ll reveal the 5-point system I’ve carefully designed to pick winning CEFs for our CEF Insider service.

(If you joined me for my exclusive CEF Insider live webcast on October 25, you know about this proven system and you got 2 of my latest CEF investment ideas for 7.1% dividends and double-digit upside in 2018. If you missed this free event, click here to watch a rebroadcast.)

So why is it important to have a good system?

Because if you don’t, you could find yourself holding a very empty bag—like investors who bought the PIMCO High Income Fund (PHK) at the start of the year because they were seduced by its 13.5% dividend yield.

Sadly, that move resulted in a 7.8% loss, even with dividend payouts:

The Perils of a High Yield

What’s even sadder is that there are plenty of funds that invest in the same assets as PHK that have done far better. Take the MFS Intermediate High Income Fund (CIF), which also plays in the high-yield bond world and is up a whopping 20.3% so far for 2017.

A Far More Sustainable Pick

This is one of many instances where blindly buying a CEF would have cost real money. So how do you avoid the trap?

My 5-Point System

When choosing CEFs, I look at 5 crucial points that drive each buy call I make. And they can help guide you, too. They are:

- Management: How good is the team at the top, and has the fund changed horses lately (frequent management changes are an obvious red flag)?

- Discount: What’s the fund’s discount to its net asset value (NAV, or the value of its underlying assets), and what has that markdown been historically? We want a current discount well below the long-term average to drive our upside.

- Portfolio: What does the fund hold now, are there any big changes to the portfolio, what’s the rationale behind those changes, and how are those assets going to perform in the future?

- Dividend: How sustainable is the payout, what are the chances of a dividend cut, and how low can the payouts go? (Key here is to look at yield on price, yield on NAV, changes in NAV and total net investment income, or NII)

- Current Climate: How does the fund’s investment strategy fit within your broader portfolio and view of changes in the broader economy?

In other words, I combine a variety of bottom-up questions about the fund’s portfolio, strategy and management with top-down questions about the asset class and economy as a whole.

The System in Action

To show how this works, let’s look at a recent example: the PIMCO Dynamic Credit and Mortgage Income Fund (PCI).

Back in early 2016, my colleague and Contrarian Outlook Chief Investment Strategist, Brett Owens, and I worked together to figure out what the future held for PCI. You can read his original buy recommendation right here.

The first step was to look at the fund’s management.

In early 2016, the fund was changing its strategy away from high-yield corporate bonds to mortgage-backed securities. The complexity of these investments scared some, but we saw this as a positive for PCI. We also saw it as a sign that the fund was in the process of a transformation that would be good for its returns—and shrink its discount to NAV.

We were right.

In July 2016, PIMCO announced that it would change the fund’s name (it used to be called the PIMCO Dynamic Credit Income Fund) to reflect its new mandate. Fund manager Daniel J. Ivascyn, who has quickly become a legend in finance, was largely behind the change as he took a more active role at the fund.

He had good reason to. At the time, PCI was the most discounted of PIMCO funds.

And while mortgage-backed securities sound scary to a lot of people because of their role in the Great Recession, PIMCO saw things differently (and so did we). Mortgage defaults were going down and the housing market was a lot stronger, which made the heavily discounted mortgage-backed securities a steal.

So PCI’s change in strategy, driven by top-notch management, and its portfolio quality indicated that its deep discount was a buy signal. It also showed that the fund’s 11.9% dividend yield was sustainable.

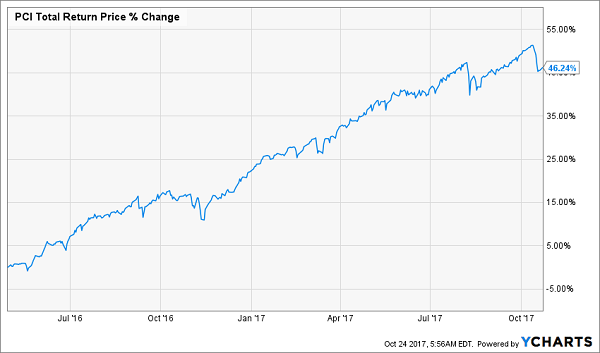

What’s happened since? A 46% total return:

A Quick Ride Up

3 CEFs I’m Watching Now

Nowadays, I’m looking at a couple dozen CEFs that I think are getting to that perfect place where the fundamentals and the broader economic climate are combining to create a perfect storm for massive upside and sustainable high yields.

The first is the BlackRock Resources & Commodity Fund (BCX), a commodity specialist that has done well in a tough environment for commodities. It’s an example of a well-managed portfolio with a great management team—but while the bottom-up is good for BCX, we’re not quite there from a macro standpoint yet. But we’re getting closer.

In the utilities world, there’s the Gabelli Global Utility Fund (GLU), which is diversified and has the added bonus of going beyond the US to take advantage of currency fluctuations. I haven’t added it to the CEF Insider portfolio yet, for a couple of reasons: its 4.1% dividend is too small and I’ve already added two foreign-focused funds that will do just as well while paying better dividends.

And they have—these two funds are up 18%, on average, since my recommendation, while GLU is up 17.2%. But instead of paying a 4.1% dividend, my picks are paying 6.9% each. (Click here to get access to my complete CEF Insider portfolio, including these two foreign fund picks.)

Finally, another interesting fund on my watch list is the AllianzGI NFJ Dividend Interest & Premium Strategy Fund (NFJ), which has been a strong performer in the past, despite a history of drastic dividend cuts (distributions are down 55% from a decade ago).

Despite those cuts, the fund has a great portfolio and excellent management. The only problem? Its income strategy (selling index options, such as calls on the S&P 500, for income) wasn’t enough to cover payouts in our low-volatility environment.

Recently, management changed its strategy (selling stock options instead of index options). That brings NFJ closer to being a buy, but its dividend coverage needs to strengthen first.

URGENT: 3 NEW Picks for 7.1% Dividends and BIG Gains in 2018!

In my just-finished FREE live webcast, I went well beyond my watch list and delivered great 2 CEFs my 5-point system just revealed!

These stealth funds pay rock-solid 7.1% dividends now … and boast ridiculous discounts to NAV. In fact, my system indicates those weird markdowns will slam shut early in the new year, catapulting us to quick 22%+ total returns!

If you missed these 2 picks, you NEED to CLICK HERE to watch a rebroadcast of this free LIVE event now.

And that’s just the start.

Because TOMORROW, Friday, October 27, at 9 a.m., I’ll release another fresh CEF pick, and I want to send you that one too! (But you must act now.)

Like the 2 picks I released at the live event, this one pays a 7% dividend, but its payout is poised to explode thanks to the massive cash flows its portfolio is throwing off. Plus it’s got even more upside thanks to its laughable discount … which can’t defy gravity forever.

When you CLICK HERE you’ll get the 2 funds I revealed in my webcast (if you haven’t already) now, plus the chance to sign up for this latest pick, for CEF Insider members only, which will come your way in the latest issue tomorrow at 9 a.m.!

That’s 3 unbeatable funds with no risk and no obligation whatsoever. Don’t miss out! Go right here to get your 2 bonus funds now and put your name on the list for my third double-digit gainer, to be released tomorrow morning!

Recent Comments