“Jenny, I can imagine. My wife makes fun of me when I ice my knees after basketball games,” I confided to my friend and favorite bartender.

Her husband, no “young chicken” anymore either she joked, was sore from his own martial arts contest. She bought him a CBD “bath bomb” to help with the aches of being active and middle-aged.

Always the sucker for natural remedies and bartender wisdom, I teed up an Amazon selection for pain and inflammation. Just 26 hours later, I was massaging hemp, turmeric and MSM into my patella tendon (about an hour before tipoff):

BO’s Anti-Inflammatory Pick

“You’re a terrible scientist,” my wife reprimanded me after I bragged about my patella’s comeback in my postgame recap. “You’re supposed to change one variable at a time. You changed everything.”

She was right, of course. I had new basketball shoes and wore a knee brace for the first time in years. I’d changed three variables, had no idea which was the miracle cure. I was left with no choice but to keep my three member “knee team” together! (Who knows how it’s working, as long as it is working, right?)

Hemp has been a popular free agent addition for many aging athletes since its increasing legalization. As you know the crop has other popular uses, too. Mine is more mundane, yet probably fitting for a dividend analyst!

The plant was used in China nearly 5,000 years ago and is enjoying a good old-fashioned American boom thanks to state governments. I live just a few blocks from our neighborhood dispensary yet I wouldn’t have thought to get a doctor’s note for the salve. Put it in on Amazon Prime, though, and it’s in my cart in minutes.

Now what about weed dividends? We’ve had plenty of readers write in asking and, with “pot holiday” April 20 just days away, I thought it’d be fitting for us to review the current crop of dividends.

The Horizons Marijuana Life Sciences Index ETF (HMMJ) just paid its seventh quarterly dividend last Wednesday. Its $0.3811 per share payout is good for a generous 5.1% trailing yield. Plus investors have been as high as a kite since inception, enjoying 160% total returns versus 22% for the S&P 500:

An ETF Contact High

But where exactly do these dividends come from? Most of the stocks the fund holds are not profitable. And the lone dividend payer Scotts Miracle-Gro (SMG) in the fund is only 7.2% of assets.

HMMJ actually makes its money by lending its shares to short sellers. Remember, when you sell a stock “short,” you are actually borrowing shares so that you can sell them at their current market price. Later, you must buy back these shares to “cover” your short position.

Normally it doesn’t cost that much money to short a stock. But the mostly-unprofitable shares that HMMJ holds are in high demand by short sellers today, and the ETF itself holds much of the supply. So, the fund’s “side hustle” of renting out its holdings is booming.

But there is no actual cash flow backing up its distribution. Nor is there any guarantee that its “short lending” business will remain as robust in future quarters. To paraphrase Prince, this distribution is just a party and parties weren’t meant to last.

How about Scotts, which does manufacture actual products? It’s more of a “pick and shovel” play on weed. The company doesn’t peddle the crop directly but sells growing equipment. Scotts stock pays 2.7% today and, while the firm raises its dividend regularly to the tune of about 5% per year.

As much hype as there is around weed, the power of the “dividend magnet”—the gravity exerted by a payout on its stock price—is even stronger. While Scotts has hiked its dividend by 17% over the last three years, its stock price has risen by the exact same amount:

The All-Powerful Dividend Magnet

The firm’s subsidiary for cannabis growers has, troublingly, not been growing organically. It’s been more hype than hemp to date for this baked maker of lawn and garden products.

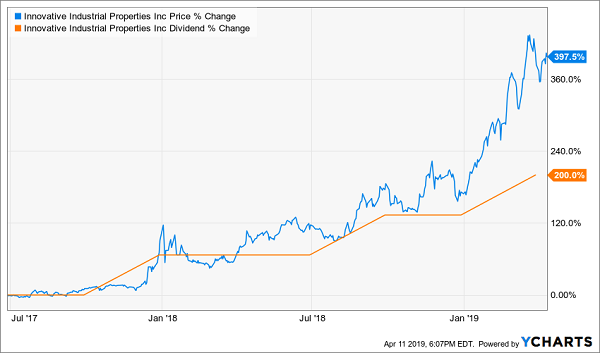

A better backdoor play on the sector is landlord Innovative Industrial Properties (IIPR). Remember, while many states have legalized pot, it remains illegal under federal law. Financing is challenging for weed peddlers, so many sell their properties to IIPR to get cash in the door for their operations. The firms then rent their former buildings back from IIPR.

Why IIPR? It’s the only real estate investment trust (REIT) that works with weed growers. As a publicly traded company, it gets to borrow money at much lower rates than it collects from its cannabis clients. As a REIT, IIPR is obligated to dish most of its profits back to its shareholders as dividends. The result is a good old-fashioned payout boom, a 200% increase in less than two years:

The Landlord’s High

The only “problem” with the chart above is that, if you don’t yet own IIRP, it is now quite expensive to do so. Its price line has run away from its payout line, which is a sign that shares are dangerously overvalued. The stock now pays just 2.1% and trades for an extremely rich 31-times its annual cash flow.

Sure, you may be able to buy IIRP “high” and sell it higher. But that’s a different dividend drug altogether.

Forget dividends you say? Let’s not forget the example that money-losing, no-dividend firm India Globalization Capital (IGC) set for us. IGC found the magic investor formula when they put two investing buzzwords side-by-side:

- Cannabis, and

- Blockchain.

The savvy marketers at IGC then introduced an energy drink infused with hemp, and wow, what a rush!

IGC Jumped 10-Fold on Buzzwords

We rational income investors fortunately avoided this clown show. I wrote to you as the blockchain-weed craze was peaking:

We level-headed contrarians should stay away from this circus. In fact, you need to be honest with yourself about the latest weed craze. If you’re tempted at all to buy this junk, it’s better if you change the channel.

Many marketers know that you and your peers are fixating on these parabolic charts. It’s going to end in tears, but they don’t care. They know they can get your attention now with a weed-fueled promise of 100% to 1,000%+ gains and get out while the getting is good.

The epilogue on IGC? Tears would be putting it mildly:

IPC’s Fast Rise and Fall

One of the smartest investors I know is a sweet grandma. She’d never fall for this speculative stuff! Grandma has a modest $387,000 nest egg that is on pace to last forever. No joke.

Recently I was chatting with a reader of mine who manages money for a select group of clients. He’s using my 8% Monthly Payer Portfolio to make a client’s modest savings – a nice grandmother with $387,000 – last longer than she ever dreamed:

“She brought me $387,000,” he said. “And wants to take out $3,000 per month for ten years.”

“Well she’s already withdrawn money for eight months (at $3,000 per month) and her balance has actually grown to $397,000. If the portfolio continues yielding 7% per year plus 2% per year in capital gains, and she withdraws $3,000 per month, it will pay my fees and still last her 27 years!”

Now many retirement experts pitch real estate as the best way to bank monthly income. But this grandma isn’t hustling to collect rent checks, or fix broken light bulbs. She’s simply collecting her “dividend pension” every month, which is 100% funded by her stocks and funds.

Actually her monthly salary is more than 100% financed – which is why her portfolio has grown by $10,000 as she’s withdrawn $3,000 per month.

I’m ready to give you everything you need to know about this life-changing portfolio now. Let’s talk about Grandma’s secret – her 8% monthly dividend superstars (which even have 10% price upside to boot!)

Grandma focuses on the 12 monthly payers in my “8% Monthly Payer Portfolio.” If you’ve got a bit more than she does–say $500,000 invested–it’ll hand you a rock-solid $40,000-a-year income stream. That’s an 8% dividend yield … and it’s easily enough for most folks to retire on.

The best part is you won’t have to go back to “lumpy” quarterly payouts to do it! Of the 19 income studs in this unique portfolio, 12 pay dividends monthly, so you can look forward to the steady stream of $3,333 in income, month in and month out—give or take a couple hundred bucks – on every $500K in capital you’re able to invest.

I’d love to share my 8 favorite monthly payers with you today, along with the name, ticker, and buy price for this floating rate bargain. Click here to get a full copy of my research on Monthly Dividend Superstars: 8% Annual Yields with 10% Price Upside, Too!

Recent Comments