I had just spent my whole paycheck at Whole Foods. My wife was not amused.

“Brett,” she paused and trailed off, a telltale sign that I was in the hot seat.

“You don’t have to buy everything organic. Some stuff…” she searched for words, shaking her head.

I flailed for a life raft: “But isn’t organic good?”

“Some fruits, sure,” she conceded. “And vegetables. But not all of them. Like avocados, and bananas—they have thick skins, so it really doesn’t matter if they are organic or not.”

“And cookies. Cookies are a highly processed food. Why are you bothering with organic?”

I tried to blame our three-year-old. “She wanted them!” I pointed, turning on my recent shopping partner.

My Waste of Money

Since then, I have gradually internalized my wife’s buying lesson. (Like an avocado, your income strategist boasts a thick shell.) Cookies and avocados always taste good. Apples, on the other hand, have a huge flavor variance. Those apples at the front desk in a hotel never taste like anything.

So, now I grab a ripe avocado. Any cookie. And I save the extra change for the organic, locally grown apple.

When it comes to income investing, we contrarians tend to walk past “conventionally-managed” exchange-traded funds (ETFs) in favor of closed-end funds (CEFs), which have more of a homegrown flair. CEFs, like organic produce, do tend to charge more—are they worth it? Usually, yes, but it depends.

The Global X Nasdaq-100 Covered Call ETF (QYLD) is an attractive yield with fees that are cheap for a reason. The ETF yields a sky-high 11.8%. Our covered call discussion last week prompted many thoughtful readers to write in and ask why I didn’t mention QYLD.

My omission was intentional. QYLD is a (relative) loser. Its strategy is sound, but the fund’s execution is lazy. I expect more for a 0.6% management fee.

The ETF owns 103 individual tech stocks. If the fund would sell (“write”) covered calls on each of these positions, it would reap nice premiums to support its 11.8% yield.

But it doesn’t. It writes calls on the NASDAQ index itself, which fetches a lower premium.

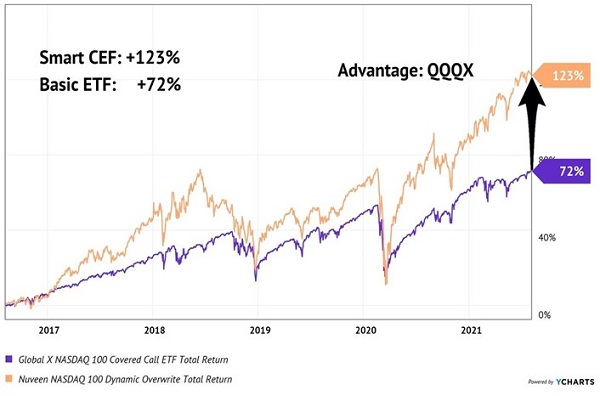

How costly is this laziness? Let’s consider QYLD’s competitor, Nuveen NASDAQ 100 Dynamic Overwrite Fund (QQQX). Here, portfolio manager Keith Hembre not only buys the individual stocks but he also writes individual call options on each position.

Plus, he smartly times the market. Keith usually sells options on 35% to 75% of the portfolio. He ups the percentage when Nuveen’s indicators look bearish (to protect on the downside) and holds more “uncovered” positions when tech looks bullish (to maximize upside).

Keith’s extra management fee (0.94%) is well deserved. Net of fees, he’s crushed his lazy ETF competitor:

For Tech Covered Calls, Choose QQQX Over QYLD

As I mentioned last week, Contrarian Income Report veterans will fondly remember our foray with QQQX. A few years back, we flipped the fund for 42% returns in just 15 months.

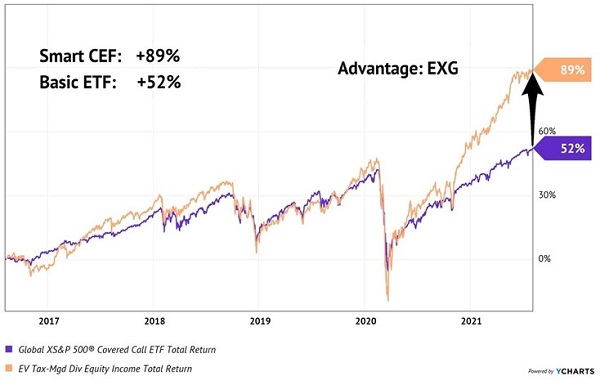

We haven’t bought QQQX since because it has typically traded at a premium to its NAV. We contrarians demand a discount, and we got one last October with our new CIR covered call play is the Eaton Vance Tax-Managed Global Diversified Equity Fund (EXG). It follows a strategy similar to QQQX. EXG buys high-quality tech stocks like Amazon (AMZN) and Alphabet (GOOG) and writes covered calls on the individual positions to generate income.

EXG is a one-click way to outsource this type of call writing, and tech stocks today carry larger option premiums than run-of-the-mill blue chips. We can thank the Robinhooders who are buying call options on these companies and paying through the nose for them!

Technology stocks began to take off in March 2020 when the Federal Reserve turned on the printing presses and papered the globe with greenbacks. EXG’s 7.9% payout is a direct play on Jay Powell and his propensity to print money.

While QQQX has traded at a premium to its net asset value (NAV) of late, EXG has (as recently as last week) been “slumming it” at a discount. But, EXG has been smartly writing covered calls on the same high-premium tech stocks that QQQX takes advantage of. So, it was a sneaky way for us to enjoy big yields plus price appreciation, which has added up to 49% total returns since we added EXG to our CIR portfolio in October 2020.

(Plus, we just received a sweet 12% dividend increase from EXG last week!)

EXG has, by the way, completely dusted its conventional dividend competitor Global X S&P 500 Covered Call ETF (XYLD). XYLD has the same problem as QYLD. It owns all 505 stocks in the S&P 500 index (yes, it’s actually 505). But it leaves money on the table by writing covered calls on the index itself, not the individual stocks!

These lost wages really add up. EXG managers Christopher Dyer and Michael Allison have earned their keep, beating the pants off XYLD in recent years:

Extra Effort, Extra Returns for EXG

And by the way, we have had the management fees “comped” because of EXG’s discount to its NAV. Now that’s the type of bargain that can help get this loose spender back in good grocery graces at home.

Lest we throw shade at all ETFs, we’ll wrap up our discussion today with an example in favor of the low-cost option. The iShares MSCI Emerging Markets ETF (EEM) is flirting with multi-year highs. A fresh “breakout” would clear the path for more gains.

Even a CEF fanboy like me can appreciate an ETF when it’s EEM. For emerging market exposure, this bellwether ETF is an effective way to diversify our holdings without getting too deep “in the weeds” trying to figure out how to buy this alphabet soup:

Top 7 of 1,353 EEM “Ticker Soup” Ingredients

We’re already up 17% since our October 2020 purchase in Dividend Swing Trader, but we shouldn’t let past profits prevent more gains. Emerging market stocks can catch fire in a hurry, and EEM is an effective and convenient way to play them when they heat up.

Selling covered calls is very profitable right now because the Federal Reserve is fueling a bubble in stock prices. As a result, every kid with a Robinhood account is buying calls (and paying too much for them) in the hopes of riches in the coming weeks.

We income investors are often attracted to selling (“writing”) covered calls. After all, if kids on Robinhood want to overpay for a call option on a given stock, why shouldn’t we be the ones to sell them that option and bank the premium?

These are the types of “Fed-Fueled” dividend plays we income investors want to buy today. Because, let’s face it, the printing presses are staying on.

Central banks are going to keep on printing. Governments are officially addicted to “free” cash.

Many investors are (rightfully) worried that this will kill their income. But as you’re about to see, it unlocks a remarkable opportunity.

I’m talking about safe and secure dividends of 5%, 6%…as much as 9%, with potential for double-digit price appreciation, to boot. All with very little risk.

Please let me share my favorite Fed-Fueled Dividends with you now.

Recent Comments