Landlords and lenders have taken it on the chin since the world shut down. And until this place is actually open for business once again, many REIT (real estate investment trust) investors are unfortunately rolling the dice on the next rent payment coming in, the next commercial mortgage payment being made.

To be fair, however, select REITs are going to be OK, and many of them are selling at bargain prices right now. In the short run, REIT prices can move together (for example, drop when the 10-year Treasury yield rises). However, as weeks turn into months and years, we usually see a great variation in the performance of REIT stocks.

The REIT sector varies widely because, well, it really isn’t a sector at all. It’s a corporate vehicle that let’s firms get a pass on taxes provided they pay most of their profits to their shareholders as dividends.

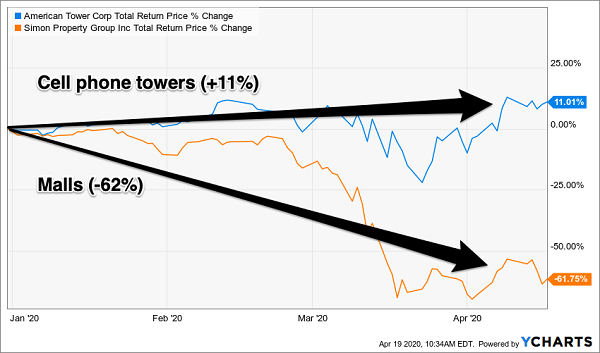

A cell tower landlord like Hidden Yields holding American Tower (AMT) and a shopping mall owner like Simon Property Group (SPG) may both be REITs, but their cash flows are completely different. And their year-to-date returns reflect the diverging outlooks for cell phone usage and mall traffic:

Same Sector, Wildly Different YTD Returns

(Think about Amazon (AMZN) and Macy’s (M). Both are technically retailers, but they have little in common. Ironically, AMZN is a major holding of many retail ETFs. Why investors would want to also own the firms that are being eaten alive by Bezos & Co., I do not understand.)

Buying a REIT ETF these days carries similar “loser risk.” This is a stock picker’s market, and we should be especially picky when combing through the wash out in REIT-land. Many stocks have been trashed for good reason, but bargains do exist. To find them, we should focus on the landlords who derive their income from “asset-lite” businesses, which often happen to be tech plays.

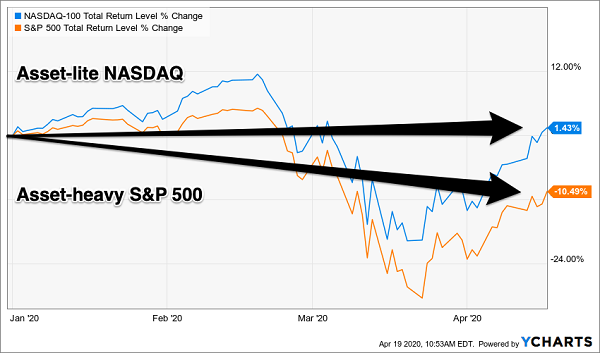

There’s a reason why the NASDAQ has whipped the S&P 500 in this rough start to the 20s. Many of us are sitting at homes with our cell phones nearby, Zoom (ZM) meetings running while we shop online at Amazon! The theme here is that our attention and our wallets are all focused on tech, and Mr. Market knows this:

2020’s Haves and Have Nots

We don’t talk tech often here, as most NASDAQ firms tend to pay little or no dividends. However, there is a backdoor way that we can profit from tech’s strength and collect dividends, and that’s by cherry-picking REITs (which do yield something) that rent to tech firms. We already discussed AMT—let’s get into a few more ideas for our shopping list.

Alexandria Real Estate Equities (ARE), paying 2.7%, is an undercover tech play. It owns offices and labs in what it calls “innovation clusters,” neighborhoods where companies and government agencies in a particular research area are concentrated.

Once tenants are in these clusters, they tend to stay. Heading into the pandemic, Alexandria boasted a sky-high 96.8% occupancy rate. Innovation-focused companies often let their employees work from home, so the current situation is nothing new. I would expect most are paying their rent just fine today, with no plans to shed the office.

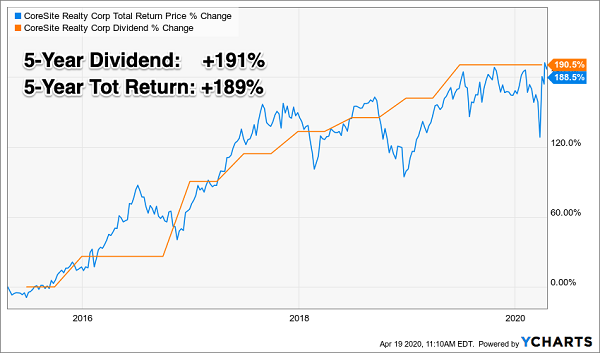

Datacenter REITs—like CoreSite Realty (COR), also of HY fame—are cashing in from this boom in online traffic. Every click you make from your computer, or tap from your phone, is “processed” by a server that is residing in a big datacenter somewhere. These facilities are owned by firms like 4.1% paying CoreSite.

CoreSite’s “Dividend Magnet” Pulls Its Price Higher

And finally, First Industrial Realty Trust (FR), yielding 2.8%, is the ideal landlord for the current “buy everything online” world. Most of its business is warehousing!

The firm is a brilliant backdoor play on e-commerce sales (which are growing by double-digits in the US). Management estimates every $1 billion of e-commerce sales requires 1.25 million square feet of space to service it.

As intriguing as these “asset-lite landlords” are, they were edged out by seven recession-proof dividend growers that I like even more right now. Now, these stocks don’t pay enough to qualify for my high-income portfolio, but they do provide us with the opportunity to double our dividends (and our capital) in the years ahead. Click here if you’d like some 100%+ profit potential in your portfolio and I’ll share the details.

Recent Comments