“There it is – Freddo’s Ice Cream. It should be right next door,” I half-heartedly explained to my wife.

And with feigned confidence, I added, “I’ll be right back.”

I crossed the street once, then again… and walked up toward this monolith:

I didn’t see a teller window, so I walked around into the ice cream shop. Maybe that was the entrance.

Nope, just a wall. So I circled back, and the door on the left “buzzed” at me. I tried to pull it open—to no avail.

It buzzed again. I tried pushing this time, and it opened. Inside there were two teller windows, both guarded by bulletproof glass.

Yes, this is what I was looking for. Oh boy.

I walked up to the available window on the right, nervously reached into my pocket, took out three very crisp one hundred dollar bills, and slid them across the countertop.

The teller barked something in Spanish at me. I had no idea what he said. I just nodded and kept my mouth shut.

He punched some numbers furiously into a 1987-vintage giant calculator. Then, he rotated it to face me:

3365

That was less than I thought it would be.

But, I didn’t have the guts to say anything. So, I just nodded, and muttered, “Si.”

He began to count out pesos in increments of 100. These were BIG bills here, too. Most local convenience stores refuse to make change for 100 pesos, in fact!

“Un ciento, dos cientos, tres cientos…”

He counted out the first thousand and began on the next. Then, quickly realizing that my stack of 100s was becoming unruly, he put a rubber band around the first pile.

I stuffed the wads of pesos into my pocket and walked outside into the Buenos Aires afternoon.

My experience in Argentina is five years old, but the currency lessons are coming around today. At the time I learned how to get money from my friend, who was fresh off his third trip to the “Paris of South America.”

The country’s ever-inflationary economy means cash is preferred. But you can’t get a fair rate at legitimate establishments. My buddy explained:

“So, what you need to do is take crisp U.S. $100 bills with you. Then I’ll tell you where to go when you get down there.

“Basically, you don’t want to exchange your dollars in a real bank, because the bank won’t give you the real rate. You need to go to the black market to get the best rate.

“I know it sounds like a real pain… but it’s the only way to do it. Everyone does it down there. Seriously, it will make your trip 40-50% cheaper if you exchange your dollars for pesos where I tell you to.”

“BUT!” he warned. “Don’t exchange your cash on the street. They’ll rip you off, guaranteed. And even if you get real money, someone will follow you and rob you. So… never exchange money out in the open.”

Did the Bond God Just Get Robbed in Argentina?

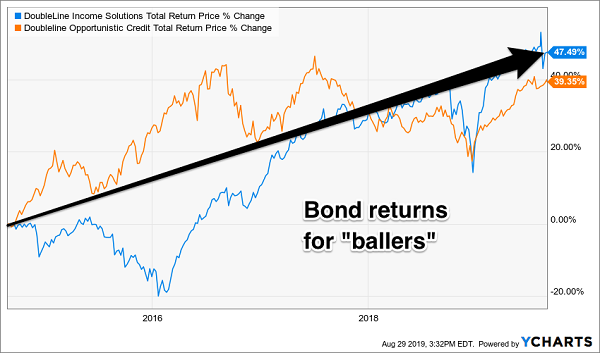

DoubleLine’s founder Jeffrey Gundlach (nicknamed the bond god for his fixed income brilliance) runs two very successful closed-end funds (CEFs). His team of 65 credit analysts cherry pick their favorite bonds in the US and around the globe. Over the past five years, the two funds have delivered total returns (including distributions) of 39% and 47%:

It’s Tough to Beat These Bond Funds

These are of course excellent results for bonds. Of the two vehicles, I prefer to drive the DoubleLine Income Solutions (DSL) fund because its team has a wider mandate to search the globe for high yield.

At the end of July, DSL’s top 25 holdings yielded an average 7.6%. How great is that in a world where Uncle Sam’s bonds pay just 1.5%?

Plus, Gundlach gets to borrow money for cheap (about 2%) to buy more high paying bonds. DSL levers its portfolio up an additional 30% or so to bring the net yield on its fund to 9.2%. And remember, that’s after Gundlach’s fees!

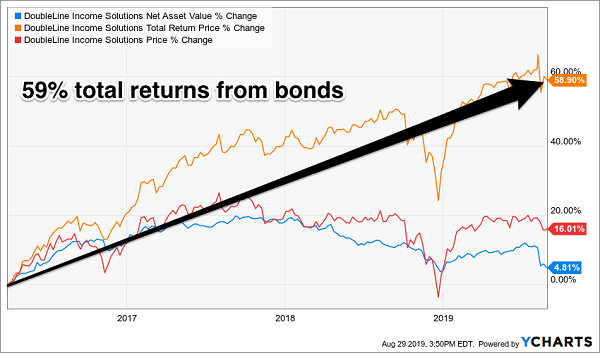

Since I formally recommended DSL to my Contrarian Income Report subscribers, it has delivered 59% total returns in less than three-and-a-half years. We beat the chart above because we “bought the dip” in early 2016. And we have another dip right now thanks to a good ol’ fashioned currency crisis in Argentina. Should we buy now?

When to Double Down on CEFs

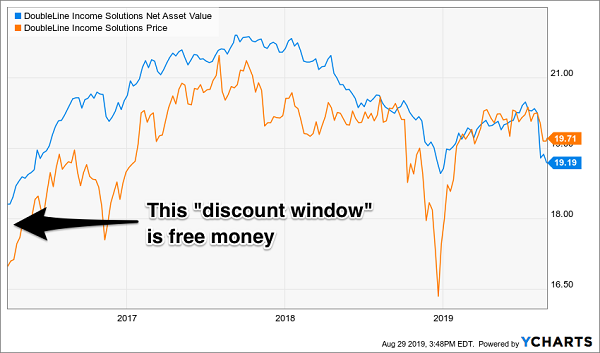

CEFs are unique vehicles because, unlike ETFs and mutual funds, their prices can drift from their net asset values (or NAVs, the actual values of their portfolio). NAVs are updated daily, and they are a truer measure of intrinsic value than price is.

As contrarians we want to buy funds when their prices are below their NAVs. In fact, the further below, the better. This is the “free money” we picked up courtesy of the bond god’s fund in April 2016:

When DSL Was Discounted, We Profited

At a glance the difference between the two lines on the far left above may not look like much. But the discount we bought, plus the distributions we collected along with the modest NAV gains we enjoyed added up to our 59% total returns:

Income + Discount Closing + NAV Gains = +59%

DSL’s price has dipped over the past month, but so has its NAV. In fact, the value of its bonds decreased even more than its shares and its price now trades above NAV. In other words, the fund is now fetching a modest 2.5% premium.

The DoubleLine team had doubled down too often on Argentina. A charming place to visit, but an economic basket case, it represented 10% of the fund. That’s not a position you want to have when the peso crashes.

It was a rare miss for this talented team, but a miss nonetheless. It doesn’t make sense to buy more shares at a premium. So should we sell and cash our profits? No. I think Gundlach & Co. deserve the benefit of the doubt while they sort out this mini-mess.

But until the situation in South America looks better, DSL is a hold. Looking for safe 9%+ yields to buy? I’m glad you asked.

Safe Dividend Machines That Pay 10% Today

Our newest “perfect income play” pays a safe 10%. That’s right. A secure 10%!

Put $50K into this stock and you’ll see $5,000 per year in dividends. Or $50K in annual dividends on a relatively modest $500,000! You get the idea.

What’s the ticker? Well, that’s what I’m here to show you today.

After years of keeping it my personal secret, I’m finally revealing my Perfect Income Portfolio. A simple, proven, and time-tested strategy you can use to double, triple, even quadruple your income–almost immediately!

Plus, I’m also going to give you THREE specific investments you can buy right now for MAXIMUM income combined with MAXIMUM stability!

This is a strategy I could easily charge thousands of dollars for.

But today, I’m handing you the keys to the kingdom right here on this page.

All you’ve got to do is take action and implement what you’ve discovered. If you want to take charge of your retirement income, you can easily build a portfolio which returns 10%+ per year—without EVER having to withdraw from your savings.

Now, compare this to the S&P 500’s 1.9% dividend and we’re talking about a $40,500 difference on a $500,000 portfolio—every single year! That’s the sort of life-changing money that can provide true security and freedom.

Best of all, as you’ll see today, it only takes a few minutes to set up this vastly more profitable portfolio.

When I talk about the Perfect Income Portfolio, I’m speaking about a collection of safe dividend stocks and funds that:

- Pay you 7%, 8% or more consistently and predictably—even if there’s a crisis, crash, or pullback.

- Give you a safe, secure, and steady income of $10s of thousands per year in cash—not just ‘paper gains.’

- Pay out exclusively from your investment income and NOT require you to withdraw cash from your savings or assets.

- Avoid overly-complex, high-risk investments that can wipe out decades of hard-earned money in a matter of weeks or months!

- Are simple to set up and simple to manage—so you’re not glued to your screen all day and you can actually enjoy life.

- Are backed up by a proven track-record of 10% total returns per year since inception.

As I mentioned, this was built from years of painstaking research, trial and error, and financial modelling. I designed it for my own personal portfolio and my desire to enjoy a large income…without exposing myself to too much risk or withdrawing from my savings.

And, in the obsessive pursuit of this goal, I quickly realized traditional income strategies just weren’t going to cut it.

So, instead of listening to the mainstream advice like…”invest in the Dividend Aristocrats” …”withdraw 4% per year”…”lower your expenses”…”cut back on luxuries”…I decided to carve my own path instead.

This journey led me to uncover three little-known investment ‘vehicles’ that can safely and securely double, triple or even quadruple your income—almost immediately.

So, right now, I’m pulling back the curtain and showing you how you can build the Perfect Income Portfolio today. Click here and I’ll show you how to get access to my full research, recommendations and stocks to buy today (including their tickers and buy prices).

Recent Comments