Need more proof this market is completely upside down? Look no further than this mess with Hertz Global Holdings (HTZ).

You likely know the story: the car-rental chain, run off the road by the coronavirus, filed for bankruptcy over the Memorial Day weekend. On the first trading day afterward, May 26, the stock fell to $0.56 … then soared 10X!

Investors Compete to See Who Can Lose the Most

It’s pulled back a bit since, but is still up 200% from where it stood right after its bankruptcy filing.

And get this: 159,000 of users of the popular Robinhood trading app owned Hertz as of June 19, according to Robintrack. That’s nearly four times the 44,000 who owned the shares three weeks earlier, on the day it went bankrupt.

This is pure gambling—these folks are buying and hoping they can pass Hertz stock off to others before it collapses.

The Bankruptcy Trade Is so 2020

Hertz isn’t alone: Whiting Petroleum (WLL) declared bankruptcy on April 1—and investors (at least Robinhood users) couldn’t buy fast enough: 56,000 of them owned the stock on June 19, up from 13,000 on the day of the bankruptcy filing.

Let’s be honest: behavior like this is enough to convince anyone that this market is bubbling over. It might even tempt you to sell your stocks and go to cash. But we’re not going that far. We need the dividends!

Besides, going to cash means we’ll be stuck on the sidelines, pondering the impossible question of when to get back in. That’s why permabears lose money in the market—they always wait too long.

A Careful Play for Tax-Free Dividends and Upside

Instead, we’re going to steer a prudent course. And income-seekers that we are, we’re going to focus on investments that pay high, stable dividends. That way, we get most of our return in cash, not here-today, gone-tomorrow paper gains.

The 10-year Treasury, by the way, is disqualified because it doesn’t pay, yielding a meager 0.7% as I write.

10-Year Treasury Rates: Down for the Count

Luckily, there are two places we can find safe payouts of 6.5% and up, plus strong price upside, too. And both carry the “endorsement” of Federal Reserve chair Jay Powell himself!

Let’s dive into both now, starting with an investment that’s more than worth your attention today. Then we’ll follow up with another you can put on your watch list—and be set to jump on after the next pullback (inevitably) rolls through.

Step 1: Follow the Fed to This (Tax-Free) Dividend

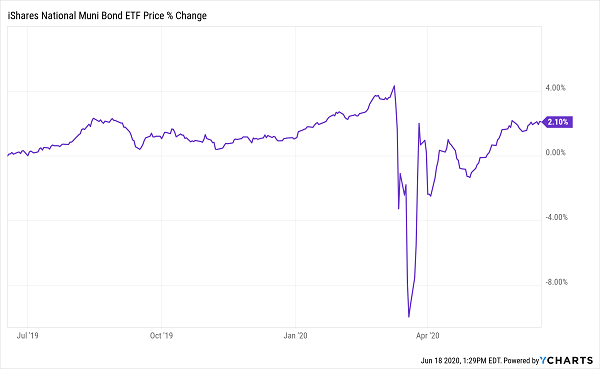

Our first “safe dividend” stopover is the opposite of Hertz: “boring” municipal bonds, which are issued by municipalities to fund infrastructure projects.

Back in March, the “muni” benchmark iShares National Muni Bond ETF (MUB) plunged 14% in just 10 days as investors worried the coronavirus would lead to a wave of muni defaults. That’s a massive dive for steady assets like munis:

Munis Crumble, Then Get an Assist From the Fed

As you can see above, munis then bounced back fast—even faster than stocks. That’s because the Fed rode to the rescue, pledging to buy up short-term munis.

That’s about the strongest insurance you can get against another pullback—and with munis still off their March highs, you’ve got a shot at some upside here, too. (And if high-profile defaults like Detroit and Puerto Rico worry you, fear not: those are outliers—just 0.042% of munis have defaulted in the last decade.)

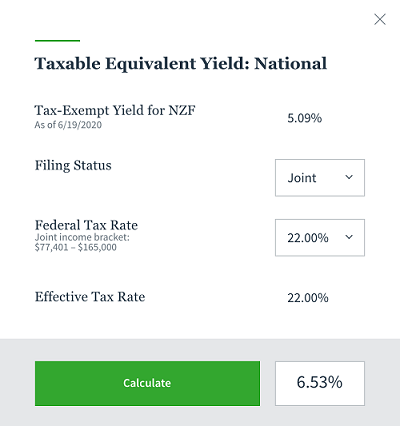

Our best play here is a closed-end fund (CEF) like the Nuveen Municipal Credit Income Fund (NZF), which trades on the market, just like a stock or ETF, and hands us a nice 5.1% dividend. That’s only the start, though, because thanks to muni-bonds’ tax-free status, your “real” yield would likely be a lot higher, depending on your tax bracket: I’m talking 6.5% or more.

Source: Nuveen.com

Plus, you get another shot at upside from NZF’s 7.4% discount to net asset value (NAV, or the value of the munis in the fund’s portfolio). That discount has been as low as 1.5% in the last year, and I expect it to head back in that direction, pulling the fund’s market price higher as it does.

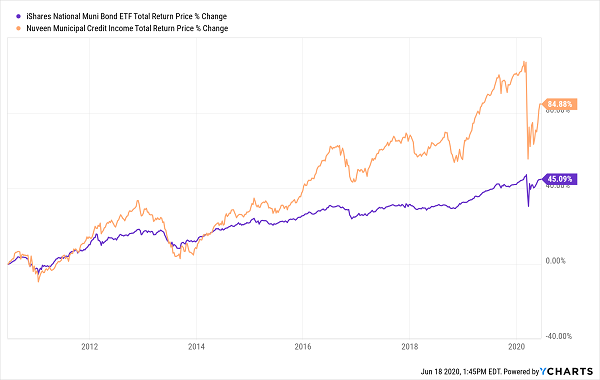

Now let’s talk performance: in the past decade, NZF has done what we’d expect from a “steady Eddie” muni-bond fund: its price has moved in a nice, narrow range, rising about 3% in that time, letting investors collect its tax-free payout in peace.

When you include its dividend, NZF’s total return soars to 85%—all in cash—besting MUB.

NZF Easily Beats Its Benchmark—in Cash

And remember, that 85% return doesn’t account for NZF’s tax advantages, so your real return would have been a lot higher here.

Now let’s move on to …

Step 2: Put This 9.9% Dividend on Your Watch List

Our next stop isn’t known as the safest place to hunt for big dividends, but here again, Jay Powell has given us a nice setup. I’m talking about high-yield corporate—or junk—bonds.

The Fed, of course, has been buying corporates since this crisis began, but it’s mostly been doing so through ETFs. Now the Fed says it’ll snap up bonds individually “to create a … portfolio that is based on a broad, diversified market index of US corporate bonds.”

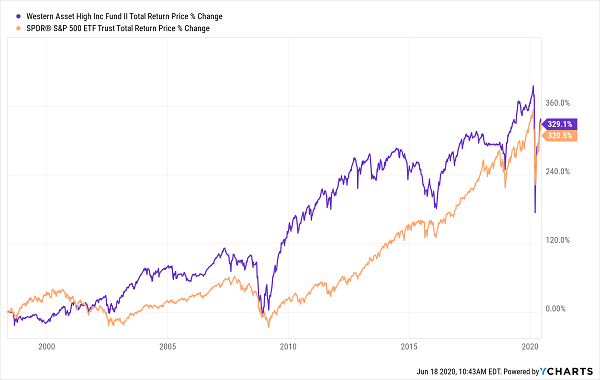

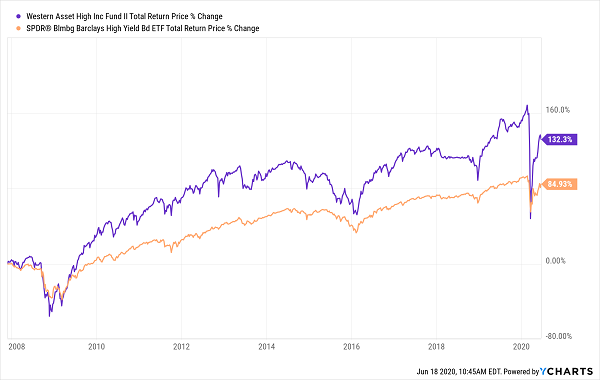

That includes junk bonds—and just like with munis, Powell’s move makes these high-yield plays safer. And, yes, our best move here is also a CEF. A good example is the Western Asset High Yield II Fund (HIX), which yields a gaudy 9.9% today.

Legg Mason (LM), which manages HIX, has been in the fixed-income game for 48 years, and that experience shows up in the fund’s performance. Since inception in 1998, HIX has beaten the S&P 500—a rarity for a bond fund. And thanks to its high dividend, that gain was entirely in cash:

HIX Rides Its Payout Past the S&P 500

Now let’s stack up HIX against the benchmark SPDR Bloomberg Barclays High-Yield Bond ETF (JNK). We’ll have to use a shorter timeframe here because HIX has actually been around for 10 years longer than JNK.

No matter.

HIX Laps the Junk-Bond ETF

With HIX trading at a 13% discount to NAV, this trade could work out nicely today, especially if you have a long time horizon.

But as you can see at the end of the chart above, despite its outperformance, HIX is prone to significant drops in a downturn—and its discount, as large as it is, can always get wider: it hit a record 28% at the height of the selloff in March.

So let’s put HIX on our watch list for now and complete this “second step” once sentiment cools down—and buyers of the Hertzes and Whitings of the world get their (inevitable) comeuppance.

These 4 Huge Payouts (up to 15%!) Are Retirement Game Changers

We’re not going to sit on our hands while we wait for this market to find some sense of balance. We’re going to buy—but we’re going to do it selectively, with 4 other contrarian investments I’ve just uncovered.

Buy them now, and you can turn this crisis into a massive opportunity—for both income and capital gains.

These 4 contrarian income plays pay amazing dividends up to 15% a year. That’s enough to double your nest egg in less than 5 years if you simply hang on to (or better yet reinvest) your payouts!

Or, if you’re already counting on your portfolio for income, these 4 income stars could give you an immediate “pay raise” of 300% or even 400%—all without having to withdraw a single dollar of your investment at any time.

Full details on these 4 dream retirement plays are waiting for you now. Click here to get everything I have on all 4 of them—names, tickers, full dividend histories, a complete breakdown of management—literally everything you need to know.

Recent Comments