In a levitating market like today’s, we dividend investors absolutely must have a portfolio that does three things:

- Automatically “times” the market for us.

- Frees up cash for us to grab bargain dividend stocks on pullbacks and, of course …

- Pays us a growing income stream!

We’ll get to point No. 1 in a second. Let’s start with point No. 2.

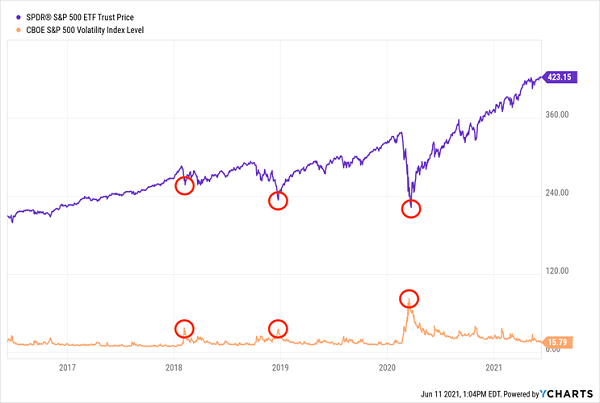

Most people panic when the market drops, but we dividend investors know that volatility is our friend. It’s easy to see this just by looking at what the S&P 500 benchmark SPDR S&P 500 ETF Trust (SPY) has done in the last five years. You’d have nicely boosted your performance if you’d added to your holdings on dips in the market and peaks in the VIX—the market’s “fear indicator,” which measures investors’ expectations for volatility.

Buy and Hold? Nah. The Timing of Your Buys (and Sells) Matters

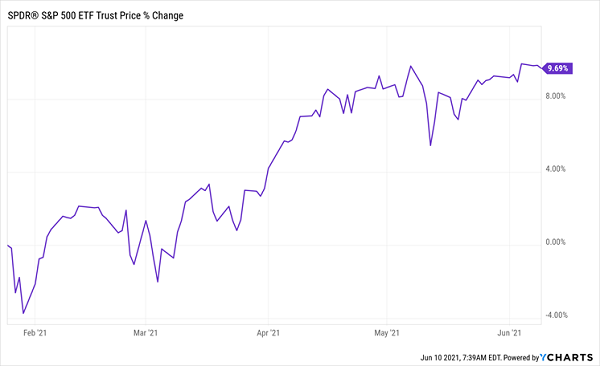

Even in a steadily rising market like the one we’ve seen in 2021, timing makes a difference. If you’d bought SPY at its highest level during the month of January (which came on the 25th), you’d be up 9.7% as I write this.

Buying at January’s Highest Level Brings a Decent Gain …

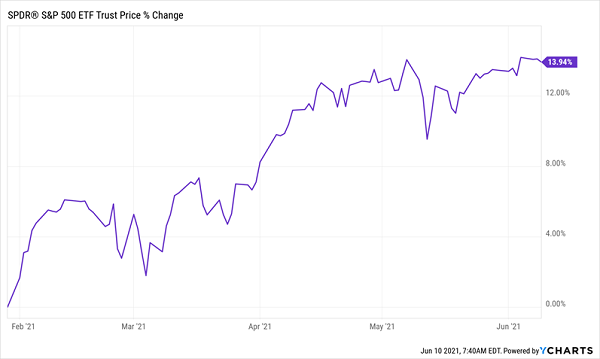

That’s not bad, but if you’d bought just four days later, you’d be up a lot more.

… But a Small Timing Change Makes a Big Difference

That’s not chump change: your 13.9% gain from buying the January dip is 43% bigger than the increase a buyer just four days earlier saw.

I know what you’re thinking: “Brett, trying to nail down a dip like that takes Jedi-like reflexes. How am I supposed to know when to jump in?”

This is where our “automatic” market-timing strategy comes in.

It’s a one you’ve probably heard of—a time-tested method called dollar-cost averaging (DCA). You likely DCA’d your portfolio to its current level, dropping a fixed amount of cash into your stock holdings at fixed intervals.

It’s my favorite way to “time” the market: your regular investment automatically buys more shares when they’re cheap and fewer when they’re pricey.

An “Active” DCA Strategy Is Your Best Play for the Economic Recovery

We’re going to take this robotic process a step further by holding back some cash so we can actively bargain hunt when mainstream investors get scared.

This beauty of this “active” DCA strategy is that it lets you hold on to your winners—and let them run—while enhancing your gains by injecting that extra cash on the dip and rebound.

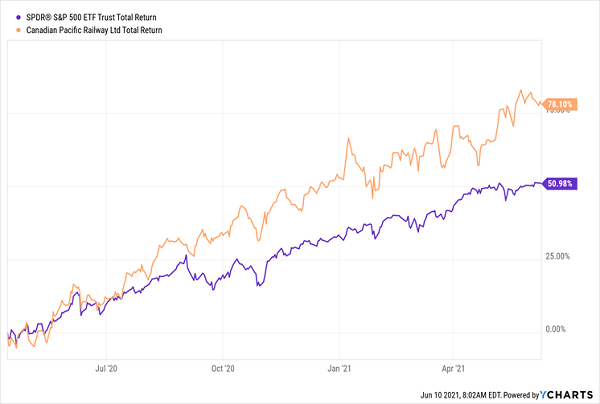

This is what I’m recommending readers of my Hidden Yields dividend-growth service do now: let our winners run, including Canadian Pacific Railway (CP), which we bought on April 14, 2020, just as the rebound was finding its groove. CP handed us a market-crushing 78% in gains and dividends in just 14 months.

CP Shows the Value of Letting Your Winners Run

Or, over the longer term, Texas Instruments (TXN), which we bought in June 2017. It’s nearly doubled the market’s return since, with a 160% total return (including its dividend, which has doubled during our four-year holding period):

Another Winner Runs … and Runs

You could effectively use a lump-sum buy, DCA or, even better, our split DCA/buy-the-dip play on either of these winners.

But if you want me to name the one most unloved (and therefore the cheapest!) sector out there, I’d have to say oil and gas. Here’s why the sector holds opportunities for us now, as well as a specific name to consider—no matter how you choose to buy in.

A Prime “Accelerated” DCA Target: Energy Stocks With Soaring Dividends

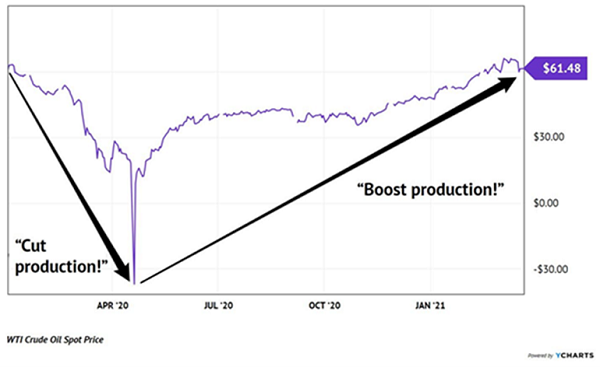

Everyone says energy prices are unpredictable, and in the short term, that’s true. But in the wake of a crisis, they have a very predictable “crash ’n’ rally” pattern we can exploit. The last one unfolded from 2008 to 2012 and is underway again.

Here’s how it typically plays out:

- First, demand for oil evaporates due to a recession. Oil prices crash.

- Next, energy producers slash costs and production.

- The economy recovers. Energy demand picks up.

- But there’s not enough supply! So oil prices climb.

- Energy producers bring supply back online, but it takes time. Supply lags demand for years, and the price of oil climbs and climbs.

We’re still early in this latest crash ’n’ rally pattern. We should assume oil prices will keep climbing for the next two or three years at least.

Oil’s Crash ’n’ Rally: 2020 to Present (and Counting)

My bet? Oil will clear $100 again before this rally is done. And if inflation continues to run hot, which, let’s be honest, is a near certainty at least for the remainder of 2021, as we compare current months to their pandemic-crushed year-earlier baselines, resource stocks are primed to rip higher. That’s because oil, gas, base metals, you name it—they all rise with consumer prices.

Then there’s the demand/supply dynamic. According to the International Energy Agency, world oil demand will come in at 92.7 million barrels in the third quarter and 94.7 million barrels in the fourth. Those figures outstrip forecast production of 91.1 million and 92.4 million.

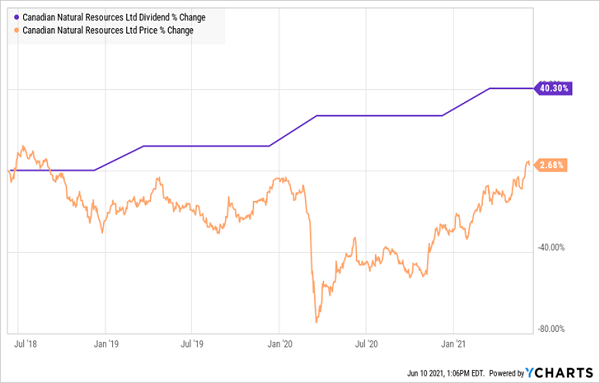

Canadian Natural Resources (CNQ) is a beneficiary of this setup: it’s the largest producer of heavy crude in Canada and a major natural gas producer, with properties in British Columbia and Alberta.

CNQ’s shares have bounced this year, along with oil. But they still have room to run, thanks in part to their bargain valuation: CNQ trades at just 10.6-times forward earnings as I write this.

You’re also getting a solid dividend. Shares yield 4.1% today and this payout has staying power, with management actually growing the dividend in the last 12 months, with hikes declared in March 2020 and March 2021. Few other energy firms can make such a claim.

Another sign that CNQ is primed to move higher is that its stock price has fallen behind its dividend growth (when measured in Canadian dollars and on the company’s home Toronto Stock Exchange).

CNQ’s “Dividend Gap” Shows Our Shot at Long-Term Gains

I’ve written before about how a firm’s share price will always track its dividend higher (this is why the yields on your favorite dividend growers always stay roughly the same, even when they hike their payouts). So when the price starts to lag behind the payout, we’ve got a nice shot at upside.

The fact that the company pays dividends in Canadian dollars also works in our favor, with the greenback likely to fall further versus its resource-powered Canadian cousin in the coming months. That would inflate our payout further.

7 “Bull or Bear” Stocks to Grab NOW (Either in One Go or Through DCA)

The 7 “Hidden Yield” stocks I’ve recently uncovered should be on every investor’s buy list now, no matter how you choose to invest in them.

I’ve hand-picked these 7 dynamic companies to return 15% every year, through all kinds of markets. The key to their strong prospects is their surging dividend payouts, which not only act like a magnet on their share prices but boost the yield on your original buy, too, as your payout zooms higher.

Just ask the folks who bought Texas Instruments on my recommendation back in June 2017. Thanks to the stock’s incredible payout growth, they’re yielding 5.1% on their original buy today, more than double the stock’s 2.2% current yield. And that’s in addition to the 136% price gains they’ve booked!

Full details on these 7 “Hidden Yield” stocks are waiting for you now. Click here to get everything you need to know, including names, tickers, complete dividend histories and my full breakdown of their operations and management teams.

Recent Comments