There’s no doubt that 2022 was the year of energy, as the Russian invasion of Ukraine caused supply shocks that sent oil and gas prices soaring. But with inflation data more muted and most of the disruptions now long priced-in as we enter a New Year, it may be time to start getting much more selective about the energy sector.

That’s particularly true if you’re an income-oriented investor in it for the long haul. Cyclical sectors like energy can see big swings and high volatility, both for the share prices of companies in the sector as well as for their dividends.

So while it may be nice to see some of the windfall profits now, you don’t want to be duped into buying a high-flying energy stock that winds up cutting or eliminating its dividend a year or two down the road.

Let me illustrate the risks and opportunities created in the energy sector right now with one stock I’d avoid and a good alternative that I would snap up in pursuit of long-term income potential.

Don’t Trust Devon

First comes the worst, Devon Energy Corporation (DVN). This is exactly the kind of company you’d expect to soar in 2022, as it’s a $40 billion exploration and production company that makes its money by drilling and taking fossil fuels to market at the current price.

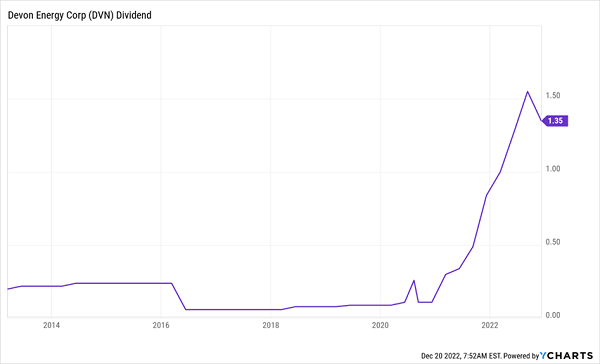

It has undoubtedly had a good run in 2022, but the future is anything but certain given the volatility in the energy sector generally and the specific nature of DVN dividends. Consider that in September 2021, its payouts bottomed at a low of 11 cents per quarter … but in September 2022, it was paying $1.55 per share!

That’s nice when the dividends are on the upswing, but is hardly something you can depend on. Payouts rolled back to $1.35 in December, and there’s no way of knowing for certain what the next four quarters will hold.

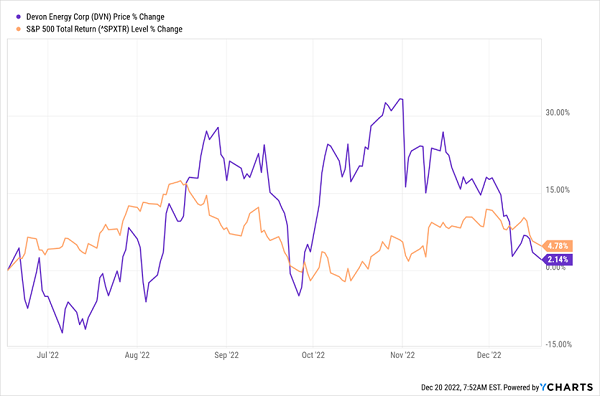

Sure, the stock is still up 35% or so in what has otherwise been a rough year for the rest of Wall Street. And if you annualize that payout you still get an impressive 8.8% yield.

But frankly, dividend investing isn’t about quick paydays. This yield accounts for a full year of payments, after all, so if you don’t know whether a stock like Devon will be back to paying 11 cents per share … well, it’s simply too hard to trust your investment is in the right place.

Throw in the fact that shares have slumped more than 20% from their October highs and crude oil prices are around $80 a barrel compared with $120 a barrel in June, and Devon looks even harder to trust.

Enbridge’s Dividend Has Staying Power

The flip side of Devon is Enbridge Inc. (ENB). This isn’t an explorer but an MLP, or Master Limited Partnership, that is focused more on the energy infrastructure side of things via tanks, pipelines and processing facilities.

Sure, it doesn’t have the name recognition as other megacap stocks in the sector. But it’s no slouch at roughly $80 billion in market value.

And sure, it has been left in the dust with a flat year-to-date return in 2022… However, the appeal of this stock is stability, not rapid share price appreciation, and unlike Devon it has rallied strongly off its October lows on hopes of a brighter year ahead in 2023.

But more importantly, the nature of the business is much more conducive to long-term dividend investment.

Enbridge is one of the largest “midstream” companies in North America, operating a network of pipeline and storage facilities for oil and gas that makes it an integral part of the global supply chain. What’s more, unlike explorers in the energy sector there isn’t direct exposure to the ups and downs of energy prices – so if oil does crater in 2023, ENB stock is relatively insulated since it is still moving the fossil fuel around despite the profit margins for refiners and other end-users.

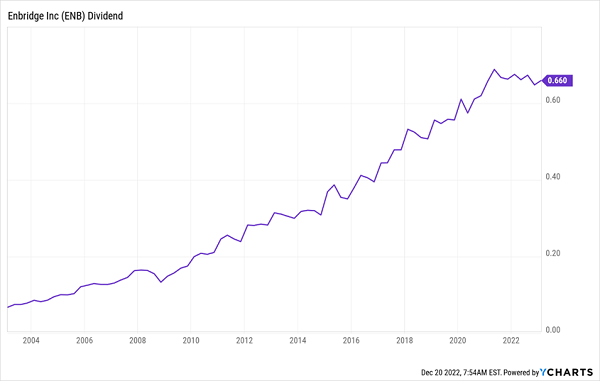

Furthermore, in recent years Enbridge has tightened its grip through acquisitions of firms like Spectra Energy and it has only widened its moat. That adds up to not just a juicy dividend yield of 6.7% right now, but 25 years of consecutive annual dividend growth – at least in Canadian dollars. While there’s a bit of ebb and flow thanks to currency exchange rates, the long-term look at dividend history here shows there is only one direction payouts are moving, and that’s steadily upwards.

If you’re interested in energy dividend stocks, this is exactly the kind of company you want to power your portfolio.

A Green Energy Play That’s Even Better Than Enbridge

Enbridge is exactly the kind of rising dividend stock we look for here at Contrarian Outlook. But you might be wondering whether ANY fossil fuel company is safe right now, given the volatility in energy markets as well as the long-term risks of climate change.

A pipeline stock like ENB is a good investment to help navigate this period, as it’s a lower-risk option. But it, too, may have its limits as sky-high energy prices are naturally sapping demand and speeding up the clean energy transition.

Thankfully, our team has uncovered a great alternative to Enbridge. It focuses on buying clean-energy projects like wind farms, solar farms and even natural gas assets with stable cash flows from long-term contracts.

It’s our favorite way to play the 21st century, clean energy revolution that will only gather momentum in the years ahead.

Even better, this is only one of 7 “Dividend Magnet” plays we’re pounding the table over right now. They all have accelerating dividends that are pulling their share prices higher and higher.

Recent Comments