I hate to see investors get snared by so-called “rules of thumb” like the 4% rule (which we’ve debunked here on Contrarian Outlook many times before).

The trouble is, these rules only “work” until they don’t. And blindly following them through an unexpected market turn could lead you to investment losses, or to run out of money in retirement.

Heck, some don’t even have a germ of truth to them, like the “100 minus your age” rule, which says you should subtract your age from 100, and that’s how much of your portfolio you should dedicate to stocks. So if you’re 30 years old, 70% should go into stocks and 30% into bonds.

I’ll be honest: I don’t get this rule. First, it’s worded weirdly. Why not just call it the Bond Age Rule, where your age equals the percentage of your portfolio in bonds? Much easier! Second, I don’t understand the justification for this rule, namely, liquidity.

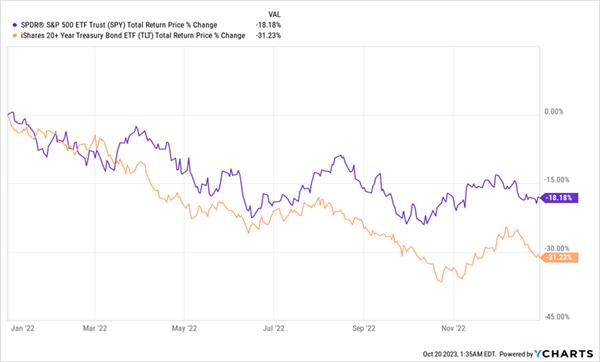

Take 2022, for example. I know I don’t have to tell you that it was a lousy year for stocks, with S&P 500 total returns down some 18%.

As we get older, we have less time to recoup our losses in stocks, so we put more and more of our money into lower-risk bonds so we aren’t forced to sell into a bear market. That’s the logic behind this rule. Trouble is, it doesn’t always work.

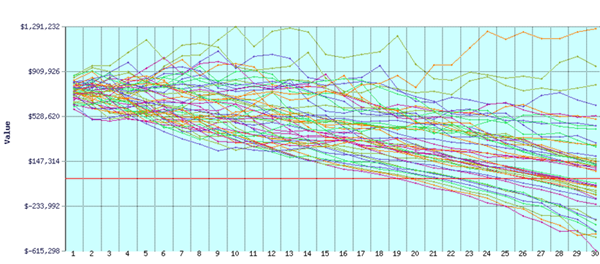

Another Poor Market to Sell In

As you can see in the orange line above, in 2022, a diversified portfolio of long-term US government bonds did even worse than stocks.

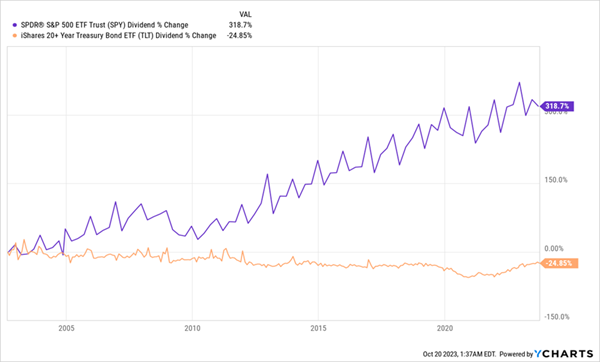

So holding Treasuries short-term through something like the iShares 20+ Year Treasury Bond ETF (TLT) doesn’t always give you as much liquidity as you’d like. Sure, you’ll get the 5% yield this fund pays out, but don’t rely on that payout to grow over time, unlike the big growth in stock dividends we’ve seen in the last 20 years:

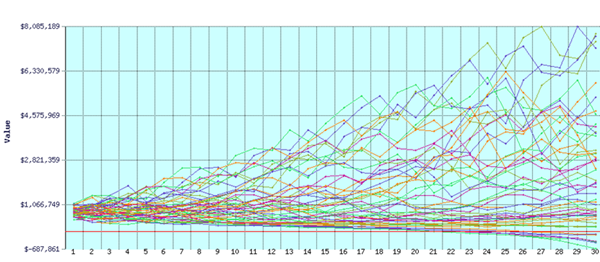

Buying US Treasuries Keeps Portfolio Income Down …

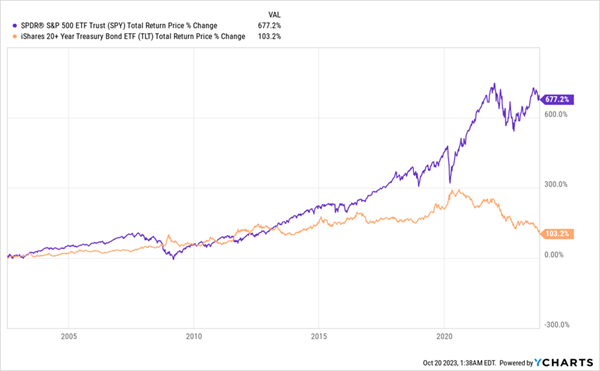

Oh, and you’d also have generated lower profits during this stretch, with returns falling in proportion to how much you put in US government bonds and not into stocks:

… And Smothers Portfolio Growth, Too

Some financial planners say this doesn’t matter because what you really want is liquidity without having to sell into a bear market. And 5% dividends sound good to most folks, who’ve seen Treasuries pay out 2% or less for over a decade. And to be fair, that higher yield does make the lower returns a little less painful to handle if you’re older.

Except you’re really just putting off the pain, because retirees who diversify into bonds have a higher chance of running out of money in retirement. And the chances of running out of money increase with the percentage of your portfolio you have in US Treasuries.

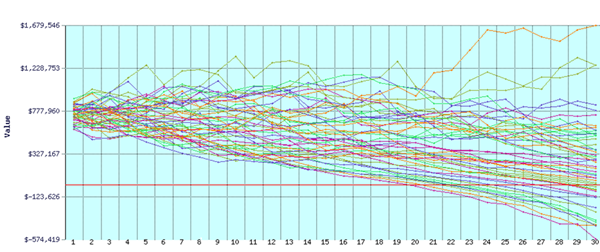

To see this in action, we can use the calculator at Firecalc.com to map out the probability of failure. Here’s what happens with a portfolio allocated to 60% long-term US Treasuries and 40% to the S&P 500:

Risk Meter Flashing Yellow

The success rate here is 71.4% for our assumptions (a retiree starting with $750,000, with a 3-year retirement). Go up to 70% Treasuries and 30% S&P 500 stocks and things get worse.

Red Hot Risk

Firecalc sees a 55.1% success rate with that asset allocation over 30 years, so at this point you’re basically flipping a coin. That’s an unacceptable gamble with your retirement, just because of an overly simplistic rule of thumb.

People don’t build houses on “rules of thumb” alone, and your financial house should have a better foundation, too. If we stuck with S&P 500 stocks, our success rate would be 87.8% in our scenario. And in many instances, our portfolio sees breakout growth.

Stocks Are the True Key to Wealth

So an S&P 500 focus is clearly the way to go here. But if we buy an index fund like the SPDR S&P 500 ETF Trust (SPY), we’re only getting a 1.5% yield, which means we’ll be forced to sell stocks every year to maintain payouts, getting into the trap of eventually being forced into selling into a bear market.

Which brings us to a much better option than ETFs: equity-focused closed-end funds (CEFs) that regularly distribute stock profits in the form of regular dividends.

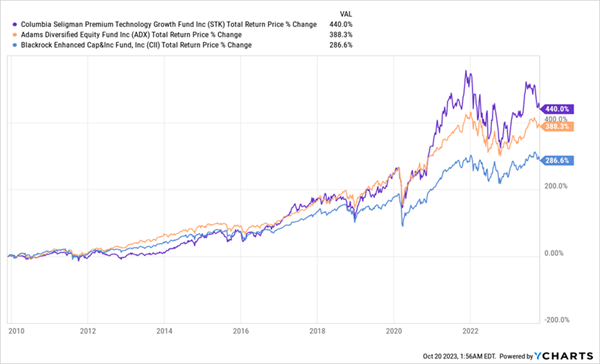

Funds like the BlackRock Enhanced Capital and Income Fund (CII), Adams Diversified Equity Fund (ADX) and the Columbia Seligman Premium Technology Growth Trust (STK) have provided exactly that for over a decade. I have written bullishly about all three over the years, and two—CII and ADX—have been profitable holds in the portfolio of my CEF Insider service. (In fact, we still hold ADX, which has returned 101% since we bought in July 2017, as of this writing.)

Going back as far as we can (to the inception of the youngest of the three, STK, in other words), we see that these funds have booked a 371% total return over the last 14 years:

Outsized Returns From 3 High-Yielding CEFs

That beats the 174% total return over that same period that a 60/40 bond/stock portfolio would get a 60-year-old retiree. And what about liquidity? This trio has you covered.

ADX has paid a 6.8% yield over this period, on average. CII has paid out 7.3%, and STK has paid out 7.8%. Thus, this portfolio gives us three things:

- A higher payout annually than Treasuries ($73,000 for every million dollars invested, versus $49,700 per million), meaning more liquidity than any portfolio with any government bond allocation can provide.

- A higher total return over time, resulting in a larger portfolio worth more money.

- Finally, we have less of a need to sell shares at any time (the payouts above are given out as cash on a regular quarterly and monthly basis—with ADX paying most of its dividend as one-time year-end payouts).

5 More “Hidden” Funds Trading Cheap (and Yielding 9.8%)

I call CEFs “hidden” funds because the big investment houses (which often manage CEFs and ETFs) put almost zero marketing muscle behind them.

There’s a reason for that: if investors discovered the income (and profit) power of CEFs, they’d likely never buy an ETF again! But if we want to retire well—and on dividends alone—9%+ paying CEFs really should be part of our strategy.

To learn more about these high-yield funds, click right here to read my Special Investor Bulletin. In it, I’ll reveal my CEF-investing strategy and give you the opportunity to download a free Special Report naming 5 of my top bargain-priced CEF picks (current yield: 9.8%!).

Recent Comments