Today, more than 18 months after the press started ringing the recession alarm, they’re still at it! And we contrarian income seekers are still happy to take the other side of that argument.

After all, this overdone fear mongering has handed us an opportunity to “lock in” bigger dividend yields than we’ve been able to grab in years. Our buy window is still open—at least for now.

Even the banks are spreading fear these days. Like Société Générale, which recently warned that even a “hint” of a recession could cause a 1987-style crash in stocks. DC-focused sources are taking up the story, too, with Politico plaintively writing: “If the bond markets aren’t scaring you yet, they should be.”

But we contrarian income investors aren’t scared. Instead, we’re coolly going where the facts take us. And the data continues to tell us we should be buying, not selling. Our preferred play? Stock-focused closed-end funds (CEFs), as many of these income plays are paying Treasury-doubling 10% yields now.

Let’s look at what that data is saying today, then we’ll talk strategy.

Consumer Spending Holds Up, Setting Up Stock (and CEF) Gains

At their core, economies are about people, and when people are spending, economies are good.

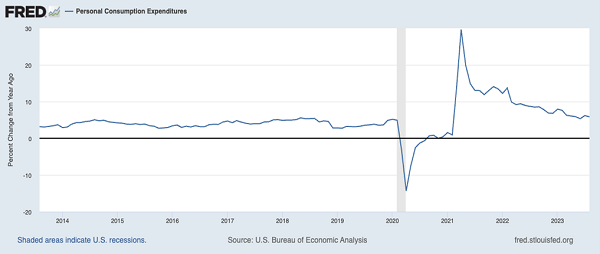

Spending Exceeds the Norm

The above chart shows personal consumption expenditures, which the Commerce Department calls “the primary measure of consumer spending on goods and services in the US economy.” It’s a broad measure of how much Americans are spending on a variety of goods and services. It’s up 5.8% from a year ago, although inflation is higher than the long-term average, at 3.7%.

This means Americans aren’t just spending more because of inflation; they’re spending more because they have more money to spend and they’re confident in the economy. This, again, is reflected in our low unemployment rate (3.8%, an almost unthinkable number for the last decade) and constantly growing incomes.

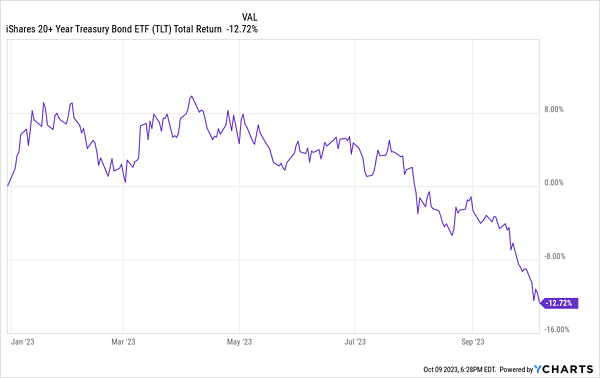

When job openings start to fall, unemployment claims surge or we start to see a significant rise in corporate-debt defaults, we can move to a more cautious stance—but there’s no sign of any of those yet. Until then, going to cash or seeking refuge in US Treasuries won’t work—ask anyone who’s invested in the iShares 20 Plus Year Treasury Bond ETF (TLT), the benchmark for long-term Treasuries, lately.

Bonds Decline in ’23

Americans Are Getting Used to “Higher for Longer” Interest Rates

Recently, Treasury Secretary Janet Yellen said banks, businesses and households are fine with higher interest rates. “I haven’t seen any evidence of dysfunction in connection with the increase in interest rates,” she said.

If you’re a small business owner or are in the market for a house, you will scoff at this. How can she say we’re “fine” with 8% mortgages when you could have locked in a rate in the 2% range for three full decades just two years ago?

But, as insensitive as her words are, she’s not really wrong at a macro scale.

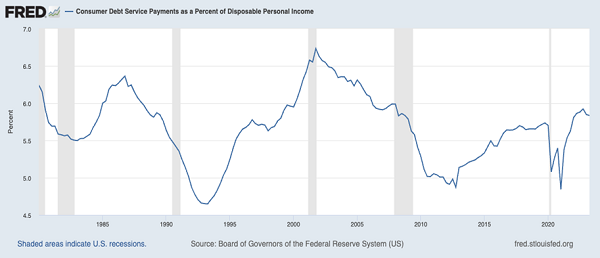

Total bankruptcies have fallen 4.9% in 2023, according to the Administrative Offices of the US Courts, and the total amount Americans have to set aside to pay down debt hasn’t gone to absurd levels, historically speaking, although it is a bit higher than the low-rate 2010s, when credit was cheap.

Low Growth in Debt-Servicing Costs

None of this data suggests there will be blood in the streets. Instead, it hints at the soft landing the Fed has been working toward and, at least so far in 2023, we’ve been experiencing.

What Do We Do Now?

With the economy humming along and the main stock exchanges taking a bit of a breather, the greatest value right now lies in US stocks.

And we’re going to skip the S&P 500 index funds the BlackRocks and Vanguards of the world are peddling and go straight where the big dividends are: equity CEFs, whose payouts have jumped, thanks to the pullback we’ve seen in the last couple of months.

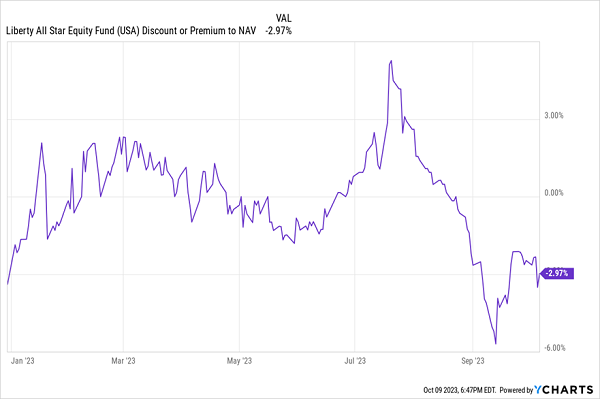

Consider, for example, the Liberty All Star Equity Fund (USA), whose top holdings include S&P 500 mainstays like Apple (AAPL), Amazon (AMZN), Visa (V) and Microsoft (MSFT). This one yields 10.4% now, and it checks the past-performance box, too, delivering a 184% return in the last decade, with almost all of that in dividend cash.

Those are two reasons why USA is attractive, but here’s why it has even more potential:

A Sale Appears

With USA’s normal small premium turning into a discount, there’s a buy window open here, but since things are moving fast, that opportunity is closing, as you can see on the right side of the above chart. But our chance to get this 10.4%-yielding large cap stock fund at a discount is still available, because the fear mongering discussed above has kept plenty of folks on the sidelines for too long.

But that’s starting to change, and when folks really start to swing back in, it will change quickly, making now the time to make a move.

Don’t Miss Your Chance to Lock in “Forever” 10%+ Payouts Now. Here’s How.

In just a few months, we’ll likely look back at this pullback and realize it was a once-in-a-generation chance to “lock in” huge dividend yields at massive bargains.

Imagine booking yourself a 10% payout essentially forever! That’s what’s on the table here. And when Treasury yields (inevitably) decline, stocks (and CEFs) will soar, driving their dividend yields down. By then it will be too late!

That’s why I’m inviting you to try my CEF Insider service for 60 days. As I write this, our portfolio yields a stout 9.8%, with many funds paying much more. This powerful income portfolio gives you instant diversification, too, with CEFs holding corporate bonds, US stocks, international stocks, real estate investment trusts and more.

Simply click here and I’ll share my full CEF-investing strategy with you and give you the opportunity to download a free Special Report naming my top 4 CEFs to buy now. Plus you’ll get your chance to kick off your no-risk 60-day trial to CEF Insider, too.

Recent Comments