These days, everybody’s looking for the one magic indicator that says when an investment is overbought—or better yet, reveals if it’s a terrific bargain.

Of course, no signal is right 100% of the time, but there is one that gives us the next best thing and unlocks high, “crisis-resistant” dividends, too.

The Perfect Crisis-Investment Indicator (for 7%+ Dividends)

The “bargain alert” I’m talking about is a figure called the discount to net asset value (NAV). And you’ll only find it in a high-yielding investment called a closed-end fund (CEF).

Before we venture too far into financial-jargon land, let’s unpack this, because what I’m about to show you is the simplest, most effective way I know of to grab steady 7%+ dividends and predictable upside in any market.

Let’s start with those outsized payouts: right now, there are about 500 CEFs out there, with an average yield of around 7%. That’s five times more than the typical S&P 500 stock pays.

And if you love monthly dividends (who doesn’t—matching your dividend payouts with your bills only makes sense), CEFs are for you: 381 of them pay monthly, according to a quick sort on CEF screener CEFConnect.

Now let’s move on to that indicator I mentioned: the discount to NAV. It’s critical for two reasons:

- It’s a proven predictor of CEF price gains, and

- It makes your CEF dividends safer, as we’ll see below.

The best way to show the discount to NAV in action is with an example, and we’ll do that with a CEF from the sector everyone seems to be chasing now: technology.

That would be the Nuveen NASDAQ Dynamic Overwrite Fund (QQQX). This fund is a bit like an ETF in that it aims to track an index—in this case the NASDAQ 100. As such, its portfolio is riven with tech giants: top-five holdings include Apple (AAPL), Microsoft (MSFT), Amazon.com (AMZN), Alphabet (GOOGL) and Facebook (FB).

But there’s a twist: to generate extra income (the fund currently yields 6.5%), QQQX sells call options on 35% to 75% of its portfolio.

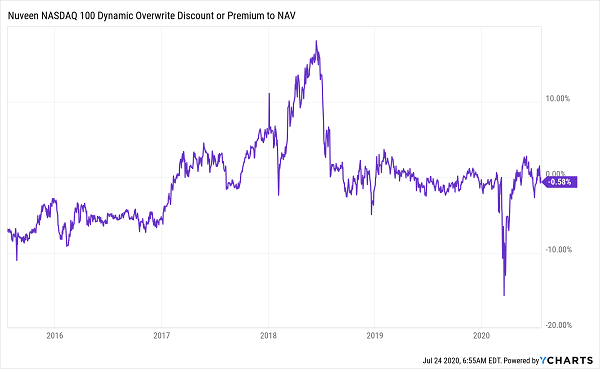

Like all CEFs, QQQX isn’t allowed to issue new shares to new investors—another key difference from ETFs—and it makes for some wild swings between a CEF’s market price and its NAV: in the last five years, QQQX has swung from a 16% discount to an 18% premium!

QQQX Flips From Discount to Premium—and Back—Regularly

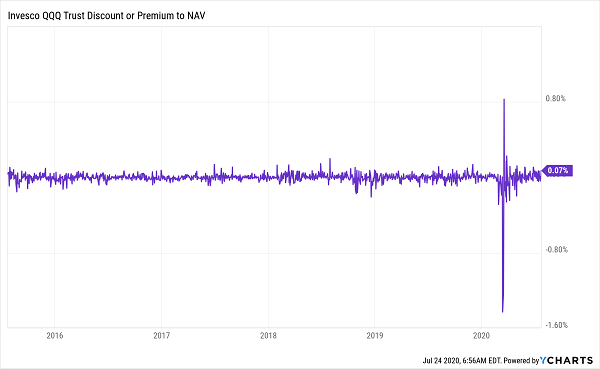

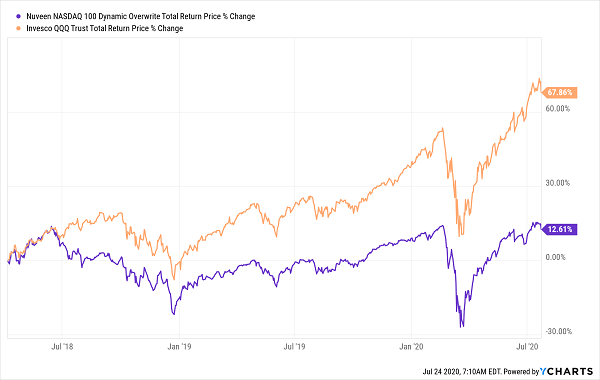

That gives us a crystal clear buy-sell signal—and it’s a big difference from QQQX’s ETF “cousin,” the Invesco QQQ ETF (QQQ), whose unit price is always more or less the same as its NAV.

QQQ Is Never a Bargain—Even in a Crisis

As you can see, QQQ did see a quick discount and premium in the spring crash and rebound, but those were fleeting and small (a premium of around 0.8% and a discount of around 1.5%).

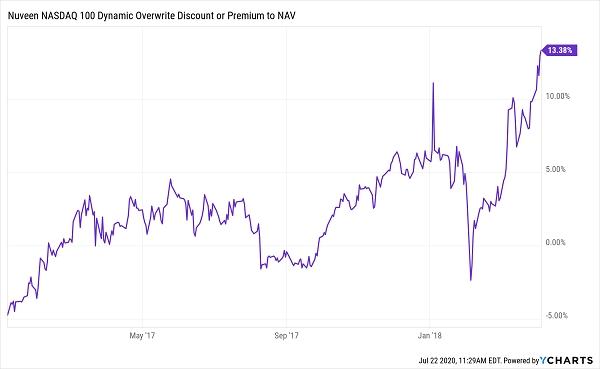

How We Rode A Vanishing Discount to a Fast 42% Return

Another reason why I’m mentioning QQQX now is because members of my Contrarian Income Report service will likely recognize the fund, which delivered a 42% total return in just 15 months after I recommended it in January 2017.

When I issued my buy call on QQQX, it traded at a 4.8% discount to NAV. Here’s what happened to that discount between then and when we sold on April 5, 2018:

QQQX’s Discount Flips to a Big Premium …

That’s a massive swing: in just 15 months, QQQX went from trading at a 4.8% discount (or about 95 cents on the dollar) to a 13.4% premium (or about $1.13 for every dollar invested in the tech stocks QQQX holds).

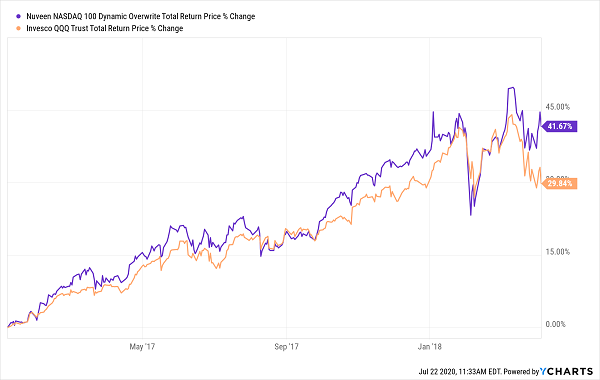

The arrival of that ridiculous premium was our cue to exit, so we did just that, taking our 42% return with us. That’s much more than the “never-on-sale” ETF delivered:

… And Slingshots Us to a Benchmark-Beating Return

The story doesn’t end there. I knew that QQQX’s premium would at best throw a cap on further upside, and at worst leave the fund vulnerable to a quick pullback as shareholders cashed in.

And sure enough, the fund has gone on to woefully underperform QQQ since our sale—anyone who took the opposite side of the bet and bought in April 2018 has been run over by the benchmark ETF:

The Danger of Overpaying

Big Discount, Risky Dividend

Even that’s not the end of the story, because there’s another risk in buying a premium-priced CEF that few people think about: it makes the dividend less safe.

Here’s what I mean: with CEFs, management only cares about the yield on NAV, or the yield you get when you divide the annual dividend payout into the per-share NAV. This yield equals the return management needs to cover the dividend.

But we’re not buying a fund’s NAV. We’re buying at the (discounted) market price. That means our yield will be higher, since we’re dividing the same annual payout into a smaller sum.

Again, QQQX is a great example: as mentioned, when we bought the fund in January 2017, it traded at a 4.8% discount and yielded 7.3%, based on its market price (and its last 12 months of payouts). However, thanks to its discount, its yield on NAV was a touch lower, at 7%.

Fast-forward to our April 2018 sell date, and the script had flipped: with QQQX at a 13.4% premium, its yield on NAV stood at 6.9%, while the yield on market price was just 6.1%.

That’s the worst of both worlds! It was also another clear sell signal that proved timely: in March 2019, QQQX lowered its quarterly dividend by 7%, to $0.39 a share, where it stands now.

Urgent: Buy These 5 “Ironclad” Dividends (up to 13%!) Before the Next Wave

A big discount not only sets you up for big upside in CEFs, but also gives you strong downside protection, too. That’s absolutely critical for us income investors because we want a rock-steady share price holding us up while we collect our big—and ideally monthly—payouts.

That’s exactly what I’ve designed my “Recession-Resistant” portfolio to deliver: the 5 stocks and funds inside it yield 9.4%, on average, and they’re all unusually cheap, even with the strong run-up in stocks we’ve seen since March.

One of these picks even pays an outsized 13% dividend while trading at a (frankly bizarre) double-digit discount!

I’ve had my research team working overtime to get this portfolio of stout high yielders out to you fast, so you can tap it for high, safe income as we head toward the fall—and a higher risk of another wave of lockdowns.

Now is the time to buy these 5 “recession-resistant” stocks and funds: Click here to get their names, tickers, complete dividend histories and my full analysis of each one.

Recent Comments