It’s a great time to be an income investor. We have yields averaging 11.1% staring us in the face.

All we need to do is step past the broader fear, and we can dial in these dynamic dividends. Which oh by the way, pay us monthly.

To do so we’ll look past traditional ETFs in favor of select closed-end funds (CEFs). These vehicles simply pay more than popular funds. Plus, they tend to be more closely managed—a good thing in manic markets like these.

Getting paid every 30 days smooths out our dividend income. This is what a vanilla portfolio of quarterly payers looks like. It’s a mess!

Now, look at a monthly dividend portfolio that pays almost exactly the same amount annually, just in even, monthly distributions:

That’s more like it. But securing 11.1% in monthly dividends isn’t as easy as reading this column and punching in a few tickers. We contrarians must be careful. Some of these funds are cheap for a reason.

The dangerous dividends are funded by a heavy use of debt—aka leverage. This can work out well when rates are low, but it’s trouble when rates rise.

So, let’s you and I review a four-pack of funds—averaging 11.1% yields—with our low leverage requirement in mind.

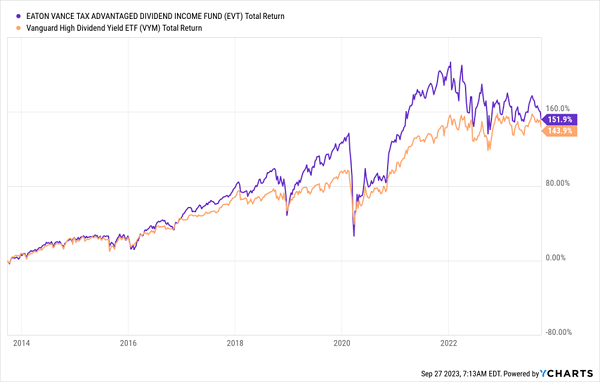

Eaton Vance Tax-Advantaged Dividend Income Fund (EVT, 8.5% distribution rate), which invests in value-oriented dividend stocks with a penchant for dividend growth.

It’s funny. When you hear “tax-advantaged,” you probably think “municipal bonds,” but that’s not the case with EVT. Instead, this CEF simply buys common and preferred stocks that distribute qualified dividends (i.e., dividends that enjoy the more favorable long-term capital gains tax rates), the likes of which include JPMorgan Chase (JPM), Constellation Brands (STZ) and ConocoPhillips (COP).

The good news is, EVT fits the bill—its roughly 21% in leverage is certainly on the low side for a closed-end fund. Unfortunately, that leverage doesn’t buy you much in the way of performance.

EVT Is Pretty Much on Part With Plain-Vanilla Indexing

If there’s any upshot, it’s that EVT is trading at a 7%-plus discount to NAV—roughly thrice its historical discount.

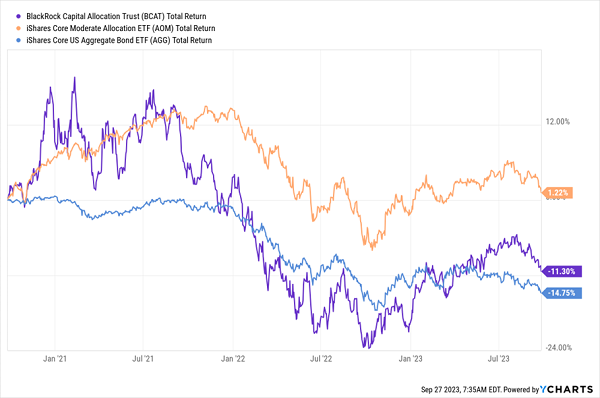

BlackRock Capital Allocation Term Trust (BCAT, 10.8% distribution rate) offers a wild yield of nearly 11% despite being a pretty plain-Jane allocation fund (read: stocks and bonds) and utilizing just 5% leverage. That leverage allows it to have an asset blend of more than 100%—equity exposure is at 56%, while bond exposure is at 46%.

BCAT’s an interesting bird. Your typical CEF is a “perpetual” fund, which means it will just keep on keepin’ on. But BCAT is a “term” trust, which means it has a limited shelf life. The fund came to life on Sept. 25, 2020, and will wind down 12 years from then—so, in 2032. With target-term CEFs, management is aiming to deliver a target NAV back to investors by the time the fund terminates. Interestingly, these funds also tend to hold bonds that are similar in maturity to their expiration date—and so does BCAT, with the lion’s share of its fixed-income portfolio invested in bonds that mature in 5 to 10 years.

Sadly, management has dropped the ball thus far. Allocation funds are designed to provide asset diversification where, say, strength in stocks can cover for weakness in bonds, or vice versa. But in this case, BCAT’s greater-than-50% allocation to stocks hasn’t done anything to counter fragility in its fixed-income portfolio. For comparison’s sake, here’s how BCAT has performed compared to the iShares Core Moderate Allocation ETF (AOM) and the Agg bond index.

A “Balanced” Portfolio, Sure, But Not a Productive One

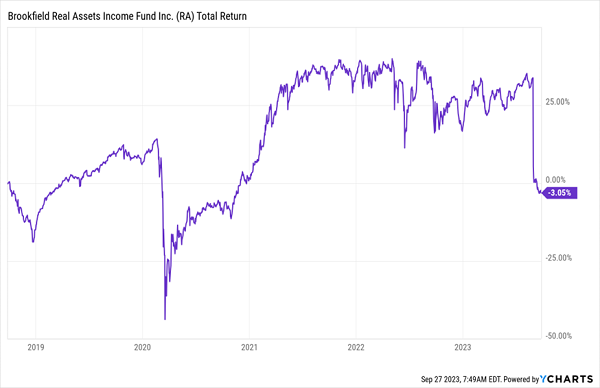

Brookfield Real Assets Income Fund (RA, 11.7% distribution rate) offers a massive yield of nearly 12%, uses a light 17% in leverage and is trading at a dirt-cheap 16% discount to its net asset value—crazy talk for a CEF that, on average, has traded at a slight premium to NAV.

If it seems almost too good to be true, that’s because it is.

Despite its “real assets” moniker, the fund is almost completely invested in credit—and just 30% of the fund is invested in infrastructure-related credit. The lion’s share of assets are invested in real estate bonds and mortgage-backed securities.

Here’s what I had to say about the fund when I sold it from my Contrarian Income Report service in November 2018:

The fund’s generous distribution (10%+) and equally generous discount (6% to 9%) gave us a margin of safety while we awarded their promising management team time to dial in their strategy. But to be blunt, they haven’t.

Their average coupon today pays just 4.8% while they’re on the hook for a 10.4% distribution on NAV. Borrowing cheap money helps fill some of the gap but not enough of it. And the portfolio remains too heavily focused on fixed-rate and longer-duration bonds for my liking.

Let’s take our modest 1% total returns and move on.

In the roughly five years since then, the monthly dividend remained constant while its NAV plunged. And finally, in September, reality came to the fore—Brookfield’s CEF cut its distribution by 41%, and shares cratered.

The Sun No Longer Shines on RA

I do think our best opportunity now is in fixed income, however—just not in second-rate funds like RA. While today’s hysteria would lead you to believe rates will never top out, they will, and we should put together a wish list for when that happens.

FS Credit Opportunities (FSCO, 13.3% distribution rate) has been around for nearly a decade, but it listed less than a year ago, in November 2022, and has made a splash since then.

What a Year for Loans!

FS Credit Opportunities invests in “non-traditional” public- and private-market credit. Right now, for instance, roughly 60% of the fund is invested in senior secured loans, 17% is in senior secured bonds, and another 7% is in subordinated debt. (Equity and asset-based finance make up the rest.) And it uses relatively light 17% leverage.

The only difficulty with investing in FSCO is its lack of public track record. It trades at a whopping 26% discount to NAV, but given that it has only been trading for a year, it’s hard to say if that will thin out (and squeeze prices higher) or if FSCO will be a perpetually cheap fund.

Earn 8% in Retirement + Get Paid EVERY MONTH

FSCO is an interesting fund that delivers fat monthly dividends. And as crazy as it seems to pass on a 26% discount, there’s plenty of uncertainty in FSCO’s near-term.

But if you’re a long-term investor looking for high yields right now, you can’t do much better than the beautifully boring, high-yielding blue chips I hold in my “8% Monthly Payer Portfolio.”

Don’t let the name deceive you. The “8% Monthly Payer Portfolio” isn’t just about earning high levels of yield—it’s about earning high levels of yields by leveraging steady-Eddie holdings that won’t have you reaching for the Pepto every time the S&P gets the jitters.

You also won’t need to stress about the size of your nest egg. Unlike many retirement plans that require you to bleed out your savings as you age, the income this portfolio can generate is so rich, it can sustain a retirement on dividends alone.

Here’s the math: A mere $500,000 nest egg—less than half of what most financial gurus insist you need to retire—put to work in this powerful portfolio could generate a $40,000 annual income stream.

That’s more than $3,300 every month in regular income checks!

Even better? The current bear market has provided us with a rare gift, pulling many of these monthly dividend stocks back into our “buy zone,” where we can grab them at bargain prices. Click here to learn everything you need about these generous monthly dividend payers right now!

Recent Comments